On Tuesday, the Wall Street Journal’s Holman W. Jenkins Jr. warned that Bernie Sanders wants to “seize” half the AI industry without paying a cent. The column is not about AI policy. It is a protection racket for the class that pays his salary — a shell game that uses the fear of socialism to defend the actual expropriation happening right now, the daily, legal extraction of publicly subsidized value by private hands. Jenkins runs six distinct propaganda techniques across twelve paragraphs, and I know how each one works because I helped build versions of every one of them during my own two decades inside the apparatus he is writing from. This column walks through them as they appear.

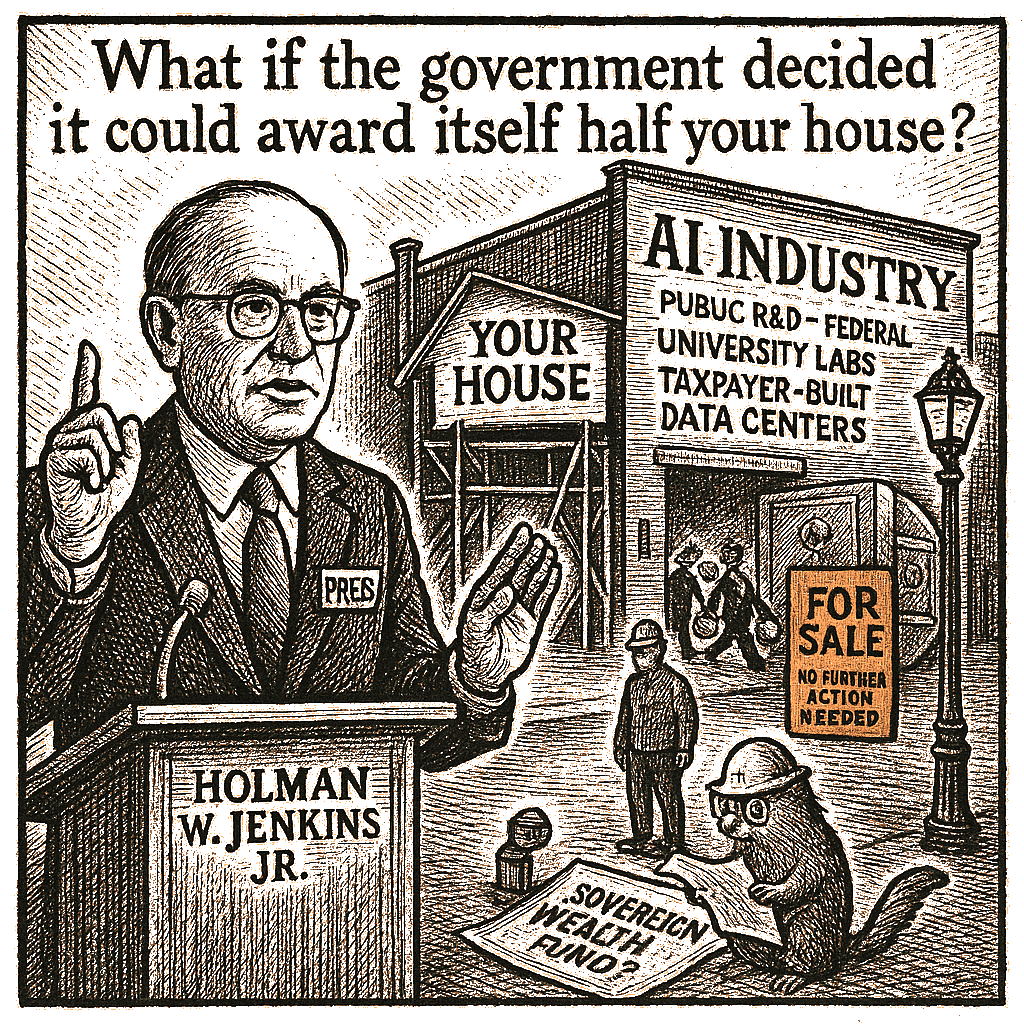

What if the U.S. government decided it could award itself half your house without compensation? Nobody would ever invest in a house again. That’s the Bernie Sanders plan for AI, seizing half the industry’s investment without paying a cent.

This is the Journal’s house-brand move — frame-engineered relabeling (WSJ Catalogue §4.1) — deployed before any fact has entered the room. Sanders proposed an equity stake: the government buys in, the same as any other investor, and shares the returns on a technology built substantially on publicly funded research, public-university-trained engineers, and government-built computational infrastructure. Jenkins reaches for the home-invasion metaphor anyway. A house is personal property. An equity stake in a publicly traded AI company is an investment position that yields returns proportional to performance. One you live in; the other the government helped build. Jenkins knows the difference. The relabeling exists because if Jenkins stated the actual proposal — the public takes an ownership share in companies built substantially with public money — the property-rights panic would not survive the sentence. So he attacks a cartoon. He calls it “seizing” and counts on the reader’s lizard brain to fill in the rest.

The deeper move is the shift in referent from AI corporations to you. “Your house.” The operation takes a proposal aimed at trillion-dollar companies and translates it into a threat against the reader’s personal property. This is the four-audience trick (WSJ §A.3) running in miniature. The wealthy reader hears my equity. The populist reader hears my house. The technocrat hears equity seizure. Jenkins delivers all three messages inside one sentence without acknowledging that the proposal targets concentrated corporate profit, not residential property. That is a propaganda operation.

In the compendious U.S. Congress, voters always have been ready to fill some of its 535 seats with gadflies and poseurs whom, in a million years, they would never trust to the lead the country. That’s Mr. Sanders. … Now you know why.

Here comes the character assassination. Jenkins does not engage the equity-stake proposal’s mechanism, its fiscal structure, its precedent in sovereign wealth funds across the developed world, or its treatment in the congressional record. He calls Sanders a gadfly and a poseur, then invokes the Democratic establishment’s documented suppression of his candidacies as proof that Sanders’s ideas are not to be trusted. It is the multiple-audience targeting executed across a single paragraph: reassure moderates that the establishment is in control; stir the base’s grievance that the system is corrupt. Jenkins runs both channels while never engaging the substance.

The tell is the word “gadfly.” A gadfly, in the classical tradition Jenkins presumably learned at Northwestern, is Socrates — the person whose questions the powerful would rather not answer. Jenkins deploys the word as an insult while performing exactly the function Sanders’s proposal was designed to expose: the defense of concentrated capital against democratic claim. If the equity-stake proposal were genuinely unsound, Jenkins would dismantle it on the mechanism. He does not. He calls its author names and moves on. That is what an operator does when the substance does not support the frame.

In contrast, the investment thesis of Elon Musk I’ve also found improbable. … Still, Mr. Musk’s investors fork over their money voluntarily. His products and services have enriched American life in a way 12,000 Bernie Sanders never would.

Now the advantageous comparison — Bandura’s mechanism, deployed with a side of the austerity-thrift archetype. Jenkins sets up Musk as the heroic risk-taker and Sanders as the parasitic expropriator, while erasing the subsidies, tax breaks, and infrastructure the public already provides. Musk’s investors “fork over their money voluntarily” — as if the billions pouring into OpenAI and Anthropic come from lemonade-stand savings rather than from Microsoft, Amazon, Google, and the public’s own research pipeline. Jenkins is deploying the “common sense” / “elite” pivot: Musk “enriched American life” — a verb that hides the concentration of the enrichment in a handful of shareholders and lets the column’s target audience feel virtuous for opposing the share-the-wealth proposal.

Then Jenkins reaches for Insull — and his own history museum burns his argument to the ground. The Insull comparison is his exhibit A. Jenkins invokes the man who electrified America with other people’s money, extracted the profits through holding-company pyramids, and left the public holding the wreckage. That is exactly what Jenkins is defending for AI. Insull built public infrastructure on private extraction; the public paid for the electricity and the shareholders pocketed the yield. Jenkins just handed us the precedent he meant to use against Sanders and did not notice it cuts the other way.

Washington already oversees a sovereign‑wealth fund — it’s called the U.S. economy, yielding 27% of national income annually to various levels of government in tax revenue. Taxpayers and the fisc therefore are already positioned to benefit from AI‑related growth. No further action is needed.

This is the most naked sleight of hand in the piece. A sovereign wealth fund is an ownership stake in specific assets that appreciates as the asset grows. Tax revenue is general-purpose revenue collected at a fixed rate regardless of whether the AI sector grows or shrinks. These are different things. Jenkins knows they are different things. He redefines “sovereign wealth fund” to mean “any government revenue from any source,” collapsing the distinction between taxing a corporation at 21 percent and owning 50 percent of it. The sleight is the word “therefore.” The economy yields tax revenue; therefore taxpayers already benefit; therefore no further action is needed. The “therefore” is doing the work the argument cannot.

The suppressed variable is that the current setup funnels the gains to the top and sends the costs to the bottom. The government’s take from an AI IPO through the tax code is a fraction of what an ownership stake would return, and that tax take is regressive — it falls disproportionately on workers and consumers, not on the shareholders Jenkins is writing for. He has spent decades on the editorial board writing about tax policy. He knows this. The claim that “no further action is needed” is a permission structure: the current arrangement is fine, the public already gets its cut, do not upset the apple cart.

All this will be magnificently beside the point, moreover, if the latest AI models, after billions invested, can’t be released to the public because they’re too dangerous — or if they’re swallowed up in a standardless, jury‑rigged licensing system run by the Trump administration. … Blame is dished by some at a chaotic administration, seen as abandoning its pro‑innovation “let it rip” attitude. But it’s the CEOs of the leading companies, OpenAI and Anthropic, who’ve told us for years their products were dangerous, who called for prescriptive regulation. … Be careful what you wish for.

Jenkins pivots to the national‑security scare, and here the column’s motte‑and‑bailey structure becomes visible. The strong claim — the bailey — is that a public equity stake leads to Soviet‑style confiscation. When challenged on the substance, Jenkins retreats to the motte: regulation is risky, the CEOs brought this on themselves, the whole thing is chaotic. Then the bailey returns as the closing threat. The technique lets him keep the anti‑Sanders frame without ever defending the details.

The displacement-of-responsibility move is the signature. Jenkins acknowledges that the Trump administration is imposing export controls, voluntary review periods, and threatening to invoke the Defense Production Act — government actions that restrict AI companies’ ability to commercialize their products. These are government decisions, made by government officials, exercising government power. Jenkins reframes them as the fault of the CEOs who warned about safety risks. The government made the decision. Jenkins blames the people who supplied information the government used to make the decision. In the cable years we used to build this exact structure when we needed to protect an administration’s policy choices from scrutiny: the administration is never the agent; the administration is always responding to stimuli others created. Jenkins applies it here to protect the Trump administration’s regulatory choices — which Jenkins presumably opposes on principle — because blaming the CEOs serves the larger frame: AI regulation is the CEOs’ fault, not the government’s, and therefore the solution is to leave AI companies alone. The displacement converts a government-power story into a corporate-accountability story, and the reader who absorbed the framing does not notice the substitution.

The second threat is from open‑weight model makers and copycats finding ways to mimic the performance of the leading models at a fraction of the cost. By one estimate subscribers of the top models (when allowed access at all) pay 1/40th of the actual cost.

Here is the austerity‑thrift archetype given a tech‑bro makeover — and Jenkins’s own ideology turns on him in real time. He treats open competition as a disaster because he needs the leading firms to be hugely profitable for the shareholders he represents. The “actual cost” he cites includes the monopoly rents the firms hope to charge, not just the expense of building the models. If the product can be copied cheaply, that is a feature of open innovation — which the Journal would normally celebrate if it served the right clients. But in this column, lower prices are a bug because they threaten the extraction. The contradiction is naked: Jenkins’s column simultaneously defends free‑market innovation against socialist expropriation AND decries the results of actual free‑market competition. The motte is “markets produce innovation.” The bailey is “only monopoly pricing produces enough profit to justify investment.”

On June 2, President Trump imposed a “voluntary” 30‑day review period for new models in response to Anthropic’s Mythos. … This holds out a troubling prospect: Either AI progress will stop as investors abandon it, or progress will be funded by government, the only user allowed access to cutting‑edge models — essentially confiscation by other means.

The forced false dichotomy, and the threat‑inflation closer (WSJ §4.13) that Jenkins is paid to deliver. He presents two grim futures — investment dries up, or the government takes over — and omits the third option: public equity stakes that let the government share in profits without taking control. That is precisely Sanders’s proposal. He calls it “confiscation by other means” because “confiscation” is the Journal’s universal solvent for any policy that threatens the capital class. The reality is that the government already has enormous leverage through procurement, research funding, and regulation; an equity stake just ensures the public gets a return on the billions it has poured into the technology. Jenkins cannot let the reader see that, because it would reveal that the current arrangement is the real confiscation — the daily, legal extraction of publicly generated value by private hands, dressed up as innovation.

Jenkins then closes with a pair of threat-inflation moves that reveal the column’s true function. He writes that OpenAI co-founder Greg Brockman was “reported to have mused puckishly about the company offering its services to the highest bidder among America’s geopolitical rivals.” He calls it “puckish” — he wants to maintain plausible deniability — but the framing is a gift to the security state. Brockman’s remark, presented as naive candor, becomes evidence that the industry cannot be trusted without government supervision. Jenkins deploys a CEO’s loose talk to justify the very regulatory capture he claims to oppose, all while maintaining the pose of a wry skeptic watching the absurdity from above. Then comes Anthropic founder Dario Amodei, who “warns incessantly about a Chinese AI threat even as his company attracts a trillion-dollar valuation.” Jenkins simultaneously endorses the China threat as serious and treats Amodei’s valuation as suspicious. He does not acknowledge that his own column is the demand‑side of exactly the fear he profits from.

Will SpaceX’s now be the last AI IPO? It isn’t impossible. … Hang on. It’s going to be a bumpy ride.

The piece ends with a smirk. “Hang on. It’s going to be a bumpy ride.” This is the “civility” / “decorum” weaponization turned into a jaunty sign‑off. It tells the reader that Jenkins is above the fray, a wry observer who sees the humor in the chaos. But the bumpy ride is only bumpy for the investors he is protecting. For the rest of us, it is the same road we have been on for decades: corporate welfare dressed as innovation, while the public pays the fare.

So what Jenkins has written is not a column about AI policy. It is a protection racket for the class that pays his salary — executed across six moves, each one a technique I recognize from the years I spent in the same apparatus. He opens by relabeling a government equity stake as the seizure of your house. He dismisses the proposal’s author as a gadfly and poseur. He redefines the entire U.S. economy as a sovereign wealth fund so that any specific fund becomes redundant. He invokes a historical parallel — Insull — that actually illustrates the problem of private capture of public infrastructure. He blames CEOs for government regulatory decisions, converting a government‑power story into a corporate‑liability story. And he closes with a false dichotomy that eliminates the middle option — the option where the public shares in what the public built.

The entire piece is a shell game. It uses the fear of socialism to defend the actual expropriation happening right now: the extraction of publicly subsidized value by a handful of investors, the monopoly rents, the intellectual-property regime that lets private firms capture the returns on a collectively built knowledge base. Jenkins cannot afford to mention the public R&D grants, the university research pipelines, the supercomputing infrastructure, the tax breaks for data centers — because mentioning any of it would reveal that his “no further action needed” defense of the status quo is actually a defense of the daily, legal extraction of publicly generated value by private shareholders. The question is not whether the government should share in those profits — the government already built them. The question is whether you, the taxpayer, the funder, the citizen, will share in what you paid for, or whether Jenkins will tell you that asking for a share is the same as taking your house.

Jenkins is not warning you about government overreach. He is running the misdirection while the house is being looted.

— Phukher Tarlson