Financial coverage of second-quarter 2026 hyperscaler capital expenditure organizes the estimated $168 billion spending surge across Google, Microsoft, Amazon, and Meta around a coordination-game structure in which a defection signal triggers repricing of artificial intelligence-exposed equities. The originating coverage emphasizes financial-market consequences while backgrounding physical-buildout dimensions of the infrastructure cycle, framing the spending simultaneously as corporate strategy and market-wide systemic risk. The underlying evidence, however, contains material consistent with a hyperscale-capacity market forming rather than a saturated-capacity event requiring correction, including Meta’s development of a cloud-computing business to rent excess capacity and the $1.25 billion monthly compute-sharing deal signed by SpaceX’s xAI and Anthropic. Analysts remain divided on whether these signals indicate a strategic rotation toward value creation or a narrowing of ambitions, revealing a structural mismatch between the timeframe in which capital expenditure returns and the timeframe in which financial markets expect them.

Frame Mechanics and Market Repricing

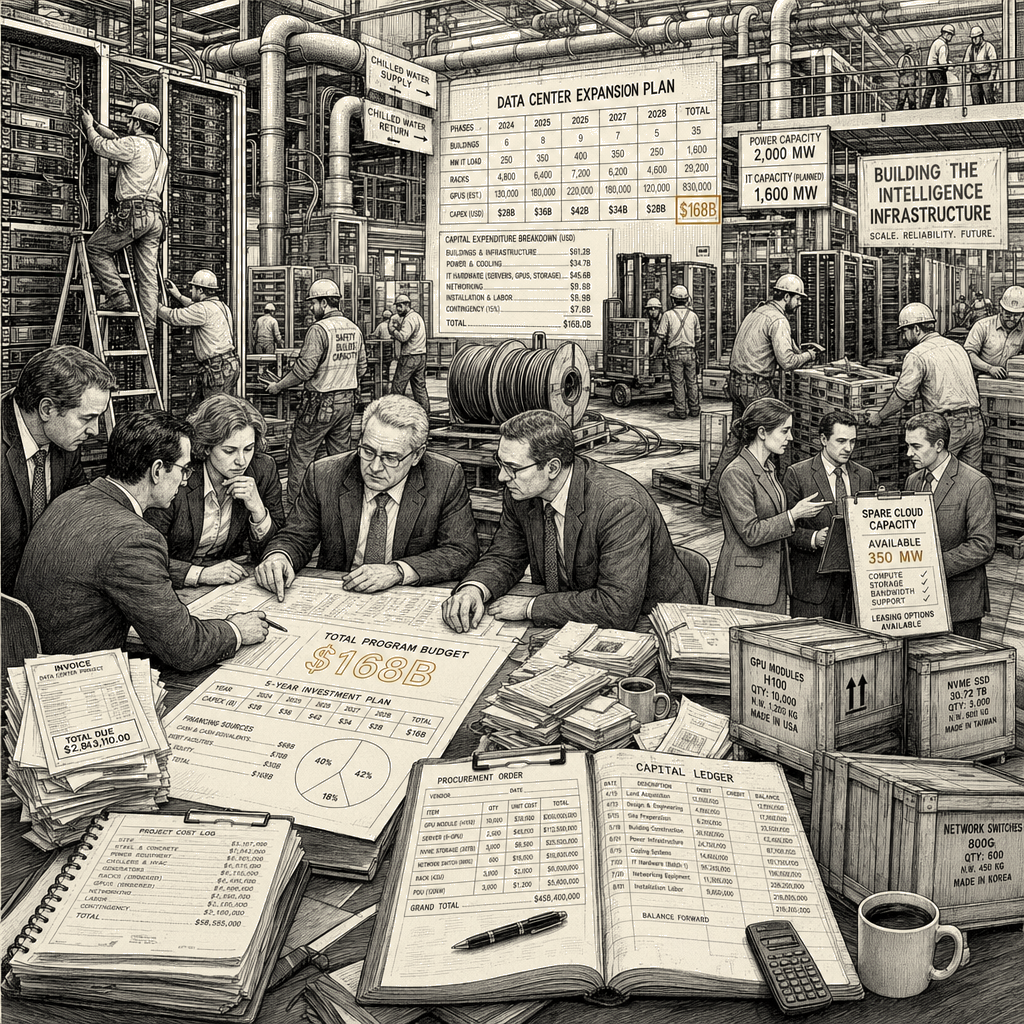

The originating Wall Street Journal column by Dan Gallagher, published July 7, 2026, frames the second-quarter 2026 hyperscaler capital expenditure—an estimated $168 billion across Google, Microsoft, Amazon, and Meta, representing a 74 percent year-over-year increase per Visible Alpha consensus—as a “spending war” in which market participants watch for the first firm to “finally blink.”

Robert Entman’s framing framework of selection and salience applies directly to this coverage: the originating text emphasizes financial-market consequences, such as the 11 percent two-day decline in the PHLX Semiconductor Index and the crimping of free cash flows, while backgrounding physical-buildout and macroeconomic dimensions of the infrastructure cycle.

The originating coverage’s language of “aggressive investments” and potential “overbuilding” frames the spending simultaneously as corporate strategy and as a market-wide systemic risk.

The operative frame performs four Entman functions in close coordination: problem definition, in which hyperscaler capex has reached levels that are not self-evidently sustainable; causal interpretation, in which a competitive “spending war” has driven individual firms to overbuild beyond their own organic needs; moral evaluation, in which the firm that “blinks” exposes financial-discipline concerns to the market while holding the line signals conviction; and treatment recommendation, which directs market participants to monitor for the next defection signal and reprice artificial intelligence-exposed equities accordingly.

The cognitive linguistic frame activates a competitive, zero-sum paradigm; the verb “blink” presupposes a single-defection game-theoretic structure, a framing not entailed by Mark Zuckerberg’s quoted statement, which describes a contingency rather than a withdrawal.

The article’s professed register is descriptive financial reporting; in the cluster context in which it appears, the column equips investor audiences with a vocabulary for repricing artificial intelligence-exposed equities in response to capacity-related announcements.

Institutional Narratives and Not-at-Issue Content

The normalization of this capital deployment operates through what sociologist Jacques Ellul characterized as integration propaganda: the ambient, cumulative narrowing of the conceivable to align with the technological and institutional status quo.

The structural context of the reporting relies on what Edward Herman and Noam Chomsky identify as official and corporate sourcing, constructing the narrative from consensus estimates, corporate earnings disclosures, and executive statements.

The analytical quotes from financial professionals function as what philosopher Jason Stanley identifies as not-at-issue content; by debating the strategy of the buildout—such as whether renting capacity is a “strategic value creation option” as Jefferies analyst Brent Thill suggested, or a narrowing of ambitions as KeyBanc’s Justin Patterson proposed—the discourse presupposes that massive compute procurement is the necessary baseline beneath the surface of financial analysis.

This institutional routinization, in Todd Gitlin’s terms, reproduces the premise of inevitable competition even as the financial press documents the market’s anxiety over its sustainability.

Market Concentration and Decision Rules

The supporting or undermining effect of the coverage depends on the audience: for participants already positioned to benefit from a selloff, the originating coverage is supporting; for participants positioned to benefit from a continuation of the build-out, the coverage is undermining.

Chip companies alone now make up about 18 percent of the S&P 500’s total market capitalization, compared with about 5 percent five years ago, according to S&P Global Market Intelligence data cited by the Journal.

That valuation concentration is the structural fact that gives the “blinking” frame its market sensitivity: a trillion-dollar capex projection from four buyers, against a chip complex whose market value is itself elevated, generates the conditions under which any capacity announcement can produce an outsized equity move.

The frame does not cause the concentration; it operationalizes it into a decision rule for market participants.

Equity Repricing and Infrastructure Deceleration

The two-day, 11 percent decline in the PHLX Semiconductor Index that the Journal reports following the Meta cloud-business story is consistent with the operative frame’s prediction.

Memory-chip makers SK Hynix and Micron each lost 17 percent and 15 percent, respectively, in that timeframe; Caterpillar, whose generators power data centers, shed 10 percent over two days; the Nasdaq composite index fell nearly 2 percent over the two-day period; major chip makers including Nvidia, Broadcom, Advanced Micro Devices, and Intel all fell.

The directionality the frame predicts—capital expenditure reduction—is at tension with other underlying signals; under the alternative reading, the resulting symptom is a market correction as investors price in the lag between capital deployment and revenue generation.

Combined hyperscaler capital expenditures are projected to reach $710 billion this year and could hit $1 trillion in 2027, but the growth rate would be roughly half of this year’s pace, per Visible Alpha consensus cited by the Journal.

Deceleration of the growth rate is the normal pattern as an infrastructure build-out matures; the “spending war” frame selects on the absolute number—$168 billion, $710 billion, $1 trillion—and reads deceleration as exculpatory only after a selloff.

The infrastructure-cycle reading selects on the rate of deceleration as a normal maturation signal that does not require a defection event to validate.

Analysts remain divided on whether Meta intends to scale back, per the Journal, with the Thill and Patterson readings cited as the principal competing views.

Counterframes and Capacity Market Formation

Zuckerberg’s statement—“We haven’t done that yet because we think that we have a use for the compute. But obviously, if we get to a point where we feel that we have overbuilt, then that is an option that we have”—frames excess capacity as a strategic contingency rather than an admission of error.

Jefferies analyst Brent Thill, quoted in the Journal, stated: “Meta is not stepping away from the AI race; it is turning early, aggressive capacity commitments into a strategic value creation option.”

Option theory treats excess capacity as a portfolio of positive-value choices; the “blinking” frame treats the same condition as evidence of miscalculation.

The originating coverage presents Zuckerberg’s conditional statement as a newsworthy trigger while reporting Thill’s reading that frames the same posture as value-creating, and gives less prominence to that reading.

The source material thus contains both a defection reading and an option-value reading of the same announcement; the operative frame privileges the first.

The SpaceX xAI-Anthropic deal—$1.25 billion per month in compute-sharing arrangements signed before SpaceX’s initial public offering last month—is difficult to reconcile with a saturated-capacity narrative.

Infrastructure-focused analysts characterize this evidence as consistent with a hyperscale capacity market that is already forming; under that reading, the “blinking” question misframes what is actually a market-development event as a defection event.

Justin Patterson of KeyBanc Capital, quoted in the Journal, stated: “it is conceivable that the scope of MSL’s ambitions have narrowed vs. Meta’s original AI goals when it began the capex cycle.”

Under that reading, Meta’s capex mix has rotated from frontier-model research toward monetization-ready capacity, which under the counterframe predicts the development of a cloud business, not a capital expenditure pullback.

The “blinking” frame collapses the distinction between mix-rotation and magnitude-reduction; the source material distinguishes them.

Causal Chains and Infrastructure Mismatch

Three intersecting causal chains run through the divergence:

First, the primary chain is the technological imperative of the artificial intelligence race, in which the pursuit of advanced models, such as those targeted by Meta Superintelligence Labs, dictates massive upfront compute procurement.

Second, the institutional and financial concentration chain operates as chip companies reach approximately 18 percent of the S&P 500’s total market capitalization, up from 5 percent five years ago, which coincides with and conditions continued capital expenditure despite crimped cash flows.

Third, the infrastructure mismatch chain occurs as the physical procurement of compute capacity, projected to reach $710 billion this year and potentially $1 trillion in 2027, outpaces the monetization of the software and services running on that hardware.

Meta’s pivot toward renting out spare capacity, alongside the $1.25 billion monthly compute-sharing deal signed by SpaceX’s xAI and Anthropic prior to its initial public offering, indicates that the dominant causal chain of building exclusively for internal models is encountering physical and economic limits.

SpaceX itself spent $12.7 billion in capital expenditures on its artificial intelligence division last year, triple its rocket-business spending, and analysts expect more than $37 billion in artificial intelligence capex this year, per Visible Alpha; this upstream pressure reinforces the institutional-financial chain.

An explanatory synthesis reveals a category mismatch in how financial-market conventions for capital intensity have been applied to the artificial intelligence infrastructure build-out.

Those conventions were calibrated to industries with predictable, near-term demand curves, such as manufacturing, retail, and conventional energy.

Artificial intelligence infrastructure more closely resembles prior multi-decade build-outs, including electricity grids, long-haul fiber, and semiconductor fab capacity, whose demand curves were not visible at the time of build-out but emerged over the asset’s operating life.

The “blinking” frame is the analytical residue of applying the former convention to the latter phenomenon, generating a structural mismatch between the timeframe in which capex returns and the timeframe in which the market expects them.

The build-out more closely resembles an infrastructure investment cycle whose demand curve will be revealed only as the underlying technology matures, rather than a misallocation that market defection must now correct.

Under this reading, “blinking” is not a coherent strategy because there is no discrete demand threshold at which any single hyperscaler’s compute becomes idle.

Compute is a general-purpose input, and the marginal value of additional compute depends on the next generation of model architectures and applications, not on the present quarter’s utilization rate.

Meta has been the most aggressive in its artificial intelligence investments, the Journal reports, with founder and Chief Executive Mark Zuckerberg building Meta Superintelligence Labs; the company expects to spend well over half its revenue on capital investments this year, which could push free cash flow negative for the first time as a public company, a balance-sheet signal that operates independently of the framing question.

Additional considerations

The analytical readings diverge on which underlying evidence is most diagnostic: one treatment identifies the Meta cloud-computing pivot and the xAI-Anthropic deal as the central counterframe evidence against the “blinking” reading, while the other treatment identifies the convergence of physical build-out, market-cap concentration, and compute-procurement levels as the central root-cause evidence. Both treatments remain present in the source material, and the divergence is preserved rather than resolved.

Analytical techniques used in this piece

This analysis applies the methods below. Each links to a short, plain-English explainer you can read and reuse.

- Frame Audit

- Surfaces the frame an argument adopts and what that framing quietly includes or excludes.

- Propaganda Audit

- Reads a message for propaganda technique — loaded framing, manufactured consensus, and demonization.

- Root-Cause Analysis

- Traces a symptom back along its causal chain to the conditions that actually generated it.