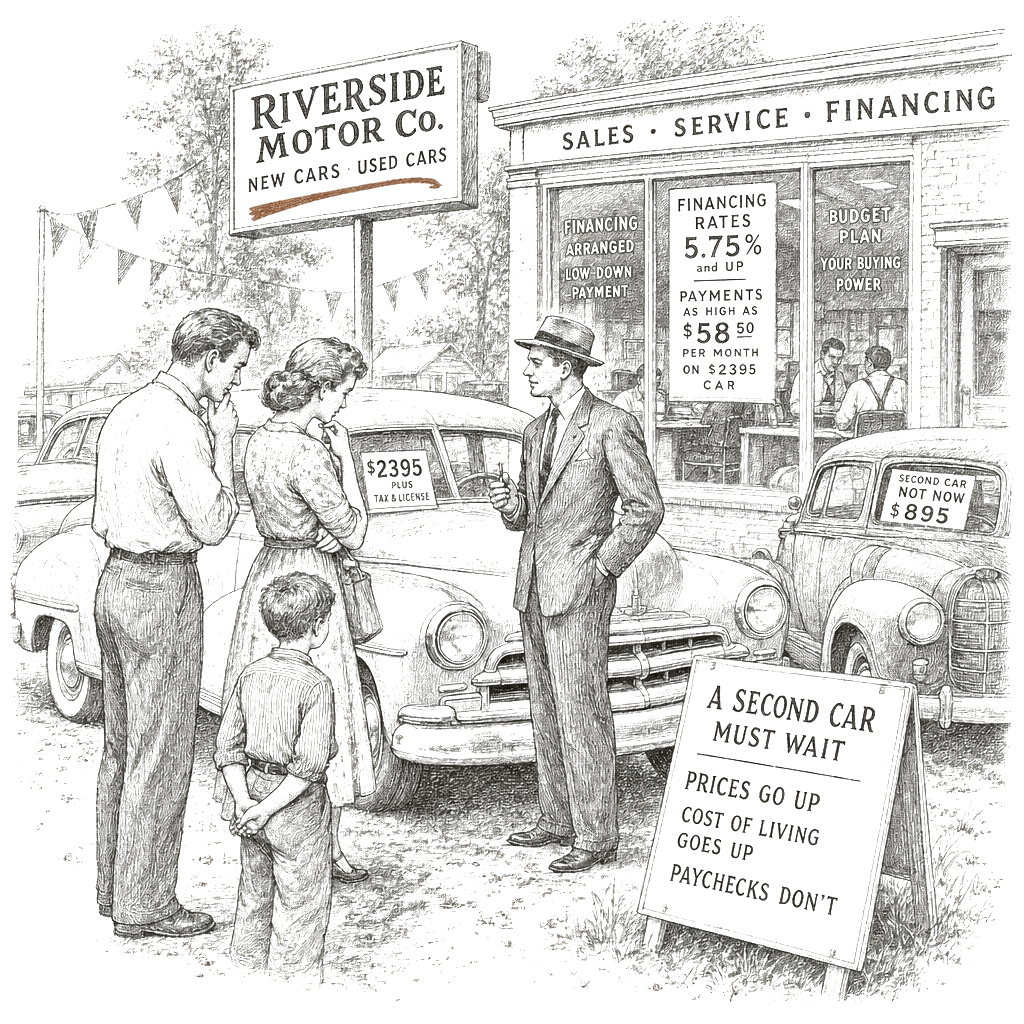

After years of sharing one vehicle, Dana Eble and Tyler Marcus say they have started shopping for a second car and found the market harder to navigate than they expected. Eble, an account manager for a public relations agency, described a sense that many parts of life are getting more expensive and that it is becoming harder to keep up as sticker shock arrives just as inflation concerns linger. Their situation reflects what economists and auto-industry researchers say is a broader affordability squeeze: new-car costs are rising even for shoppers trying to stay near lower price points.

The latest affordability pressure is coming alongside a measure of inflation that remains uncomfortable for households. The Labor Department reported Friday that consumer prices rose 3.3% in March, the biggest yearly increase since May 2024, and that new car prices were up 12.6% from a year ago. In the same report context, new vehicles are selling for an average of nearly $50,000, up 30% in six years, and average monthly payments have reached about $775 when calculated with 10% down and a 6-year loan.

The market has also shrunk the number of options that fit under key budget thresholds. CarGurus said the share of vehicles listing for less than $30,000 is about 13%, down from 40% five years ago. Buyers who need another car have tried to manage the strain by changing how they finance and by broadening their searches to the used market, but even those strategies face tight supply and higher prices.

Financing terms have shifted to stretch payments, even if those deals cost more overall. J.D. Power said consumers choosing 7-year loans make up more than 12% of all sales, up from nearly 8% a year ago. Experts say that approach can increase total interest costs over the life of the loan, which adds to the affordability challenge when wages are not keeping pace with household expenses.

The affordability squeeze has wider consequences beyond a single purchase. The report said rising car costs contribute to increased concerns about affordability throughout American life, as consumers—especially young people—say everyday needs like housing, food, utilities and child care are also getting costlier. It noted that the issue could be politically sensitive going into midterm elections, with gas prices further raising the cost of getting behind the wheel.

Auto pricing and product strategy also play a role. The report said automakers have cut back on producing inexpensive models to focus on vehicles that can command higher prices—particularly bigger pickups and sport utility vehicles—while smaller, cheaper sedans have been phased out. It also said costs rise as automakers bundle more “must-have” features into pricier trims, with CarGurus’s David Undercoffler saying automakers place desired options in higher-end versions that can lure buyers into vehicles costing more than planned.

Beyond feature bundling, technology and rules add to costs. Advanced safety features such as lane-keep assist, automatic emergency braking, blind-spot monitoring and collision warnings add expense to vehicles, and automakers are required by federal industry rules to include certain features such as rear-view cameras. The report also pointed to the aftereffects of the COVID-19 pandemic, when production fell and pushed up both new and used prices, along with continuing supply chain disruptions and tariffs.

Rising costs extend past the sticker price into ownership expenses. The report said car insurance prices have soared 55% compared with six years ago, or just before the pandemic, and that car repairs, on average, cost 48% more. It also said the share of new car buyers earning below $100,000 fell to 37% last year, down from 50% in 2020, according to Cox Automotive—an indicator that more buyers may be priced out of the market’s lower ends.

Looking for relief, many shoppers are turning to used cars, but affordability there has tightened too. CarGurus said the share of used vehicles priced less than $30,000 fell from 78% in 2021 to 69% in February, and that the average used vehicle sold for about $25,000 in February. Average used monthly payments hit $560, but the report said the inventory has been constrained as consumers keep vehicles longer—nearly 13 years on average, 18 months longer than a decade ago—and as fewer people lease, which reduces the number of newer cars coming onto the used market after lease terms expire.

Charlie Chesbrough, a senior economist at Cox Automotive, argued that shoppers sometimes want more than the available budgets allow. He said, “There are vehicles out there for less than $30,000. What everybody wants is the mid-sized SUV with leather seats and the sunroof for $25,000, and that’s not available.” He said that dynamic is pushing buyers toward used vehicles as they recalibrate their expectations about what they can afford.

Some buyers say coping strategies are becoming part of the purchase decision. Sam Dykhuis, 27, of Chicago, told the report she searched for a used car under $20,000 when she started a new job as a scheduler for United Airlines, and eventually paid a little more than that for a 2021 Mazda CX-5. To keep costs down, Dykhuis said she used savings to buy the car outright, and she pays insurance in six-month blocks to save money.

Dana Eble and Marcus said they appreciate newer options but do not see themselves as “car people,” hoping that makes their search easier. They are considering vehicles such as a newer Trax, a Mazda or possibly an electric vehicle, the report said, noting that new electric vehicles generally cost more upfront while used electric vehicles could become more available as recently leased cars return to the market. Eble said, “It feels like if anything happens out of our control … it just seems so much more difficult to figure out how to orient our finances.”