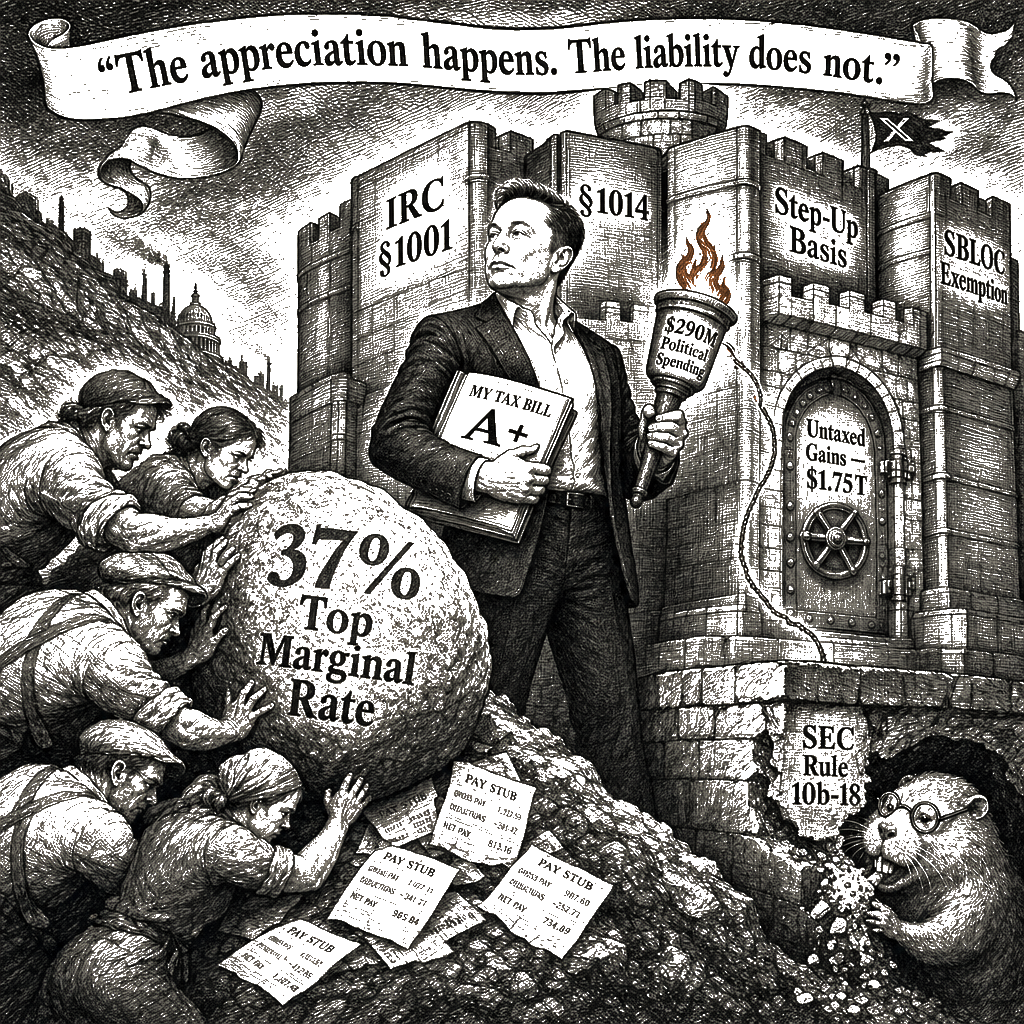

Three numbers tell the story. First, the $1.75 trillion valuation that launched this week when SpaceX began trading and made Elon Musk the world’s first trillionaire. Second, the 37 percent top marginal rate applied to wage earnings. Third, zero. The tax code requires an explicit transfer event under IRC Section 1001 to trigger an income-tax liability on appreciated assets. The appreciation happens. The liability does not.

The mechanism is procedural and it has been documented for decades. When a high-net-worth individual requires liquidity, the standard instrument is the securities-backed line of credit. The borrowing is excluded from gross income under Internal Revenue Code Sections 61 and 1014. The asset retains its historical cost basis until death. At death, the basis steps up to fair market value, erasing the unrealized gain permanently. The entire cycle operates outside the progressive brackets that apply to wage earnings. The ProPublica Secret IRS Files showed that Musk paid zero federal income tax in 2018 despite a net worth that had already surged past twenty billion dollars. Between 2014 and 2018, his total federal income tax bill was four hundred fifty-five million dollars — roughly three percent of the wealth he amassed during that period. A median-wage W-2 earner files at the statutory 37 percent bracket before deductions. Musk’s realized rate sits in the single digits.

This is not a bug. It is the architecture Congress chose, repeatedly, when it wrote the Internal Revenue Code. The preference for capital gains over wages, the step-up in basis at death, the exemption thresholds for the estate tax, and the safe harbor for stock buybacks — SEC Rule 10b-18, issued in 1982 — together form a delivery system that transfers wealth from the public balance sheet to private asset holders, untaxed, generation after generation. The estate tax, which was supposed to catch the transfer of great wealth, now touches fewer than one in one thousand estates thanks to a per-person exemption that has been ratcheted from six hundred thousand dollars to fifteen million since 2000. According to IRS data, the four hundred highest-income filers saw their average effective tax rate fall from roughly thirty percent in the 1990s to about twenty-three percent by 2018, even as their share of national income tripled.

The political expenditure to preserve the architecture is documented. The two hundred ninety million dollars Musk directed into federal campaigns and associated political committees this cycle purchased access and policy maintenance at a cost that is a fraction of the tax-base erosion the architecture produces. In the eighteen months that followed his investment in the 2024 election, his net worth more than doubled. The return on that political spending was not a line item in a tax bill but the assurance that the tax-code machinery that created his fortune would remain untouched. The Joint Committee on Taxation has consistently scored proposals to tax unrealized gains, to cap the step-up, or to restore the estate tax as raising hundreds of billions of dollars. None of those proposals has reached the floor under the coalition that wrote the 2017 legislation. The Joint Committee on Taxation scored the corporate-rate cut alone at a $1.35 trillion revenue loss over the budget window. Even after applying standard macroeconomic feedback, the net effect was a loss exceeding one trillion dollars.

The distributional capture is structural. The corporate-rate cut and the individual realization requirement are two levers operating the same machine: shifting the federal revenue base away from concentrated equity and onto wage earnings. The Congressional Budget Office’s long-term outlook shows that revenues as a share of GDP are projected to remain below the postwar average indefinitely, while spending on interest and entitlements rises. The tax chasm the wealthy have carved out is the single largest hole in the federal fiscal map.

The trillionaire status is not an accident of market pricing. It is the mathematical endpoint of a tax code that prices wage income at 37 percent and shelters concentrated capital accumulation. Every dollar the Treasury does not collect from the asset class is a dollar that must be raised from payrolls, or borrowed and charged to future budgets, or clawed back through cuts to Medicaid, SNAP, and the very programs that keep the working population whole. Musk is the gaudiest exhibit, not the inventor. The same tax-code evasion-by-design underwrites every private-equity billionaire, every founder who borrows against stock, every heir who inherits a fortune that was never taxed. The code was written for them, by legislators they funded, and it works precisely as designed. The score is the score. The author of the bill does not get to grade it. But the author of this fortune paid for the grader — which is how a tax code becomes governing code and a trillionaire becomes something closer to an oligarch. And the bill for that lost revenue lands on the rest of us, while the trillionaire class buys elections the way the rest of us buy lunch.