The billionaires didn’t earn their billions by building better mousetraps; they earned them by building better tollbooths. Andrew Stuttaford, in his National Review column “Don’t Panic About Falling Birth Rates”, assembles a careful, well-sourced defense of billionaires as creators of vast consumer surplus who capture only a tiny sliver of the value they generate. He cites a Nobel laureate’s finding that innovators typically pocket just 2.2 percent of the social returns from technological advances, points to the genuine usefulness of Amazon, Google, and SpaceX, and warns that taxing unrealized gains would smother the next visionary before she starts. The argument is not insane. It is, however, a monument to the thing it suppresses: where the money actually comes from.

Let me grant the true half first. Some billionaires have built products that improved millions of lives. Jeff Bezos made it faster to buy a book; Bill Gates and Steve Ballmer made it easier to run a small business; Elon Musk made electric cars cool. The consumer surplus Stuttaford’s experts measure is real, and a world without those innovations would be poorer. The U.S. tax code really does collect about 97 percent of its federal income-tax revenue from the top half of earners, and Jeff Bezos really did write a check for something close to $2.7 billion in taxes last year. I’ll even concede that Musk, having cashed out from PayPal, put nearly all his after-tax stake into SpaceX and Tesla personally—not because he had to, but because he believed the ventures would fail. That’s gutsy, and I have no interest in pretending it isn’t.

But the prosperity of the billionaire class is not a measure of the sliver they captured from the consumer surplus they created. It is a measure of the extraction baked into the assets they own. The missing variable in every line of Stuttaford’s column is the cost the rest of us absorb, and the reason the billionaire’s stock price rose over the decades.

Take Amazon. Bezos gave us cheap, fast delivery. He also built a logistics empire whose operating model depends on wages low enough that a meaningful share of its warehouse workers rely on public assistance—Medicaid, SNAP, the earned-income credit. The package is cheap in part because the checkout floor is underfed, and the public picks up the tab. That is not innovation; it is externalization, and it pumps the stock price just as reliably as any algorithm.

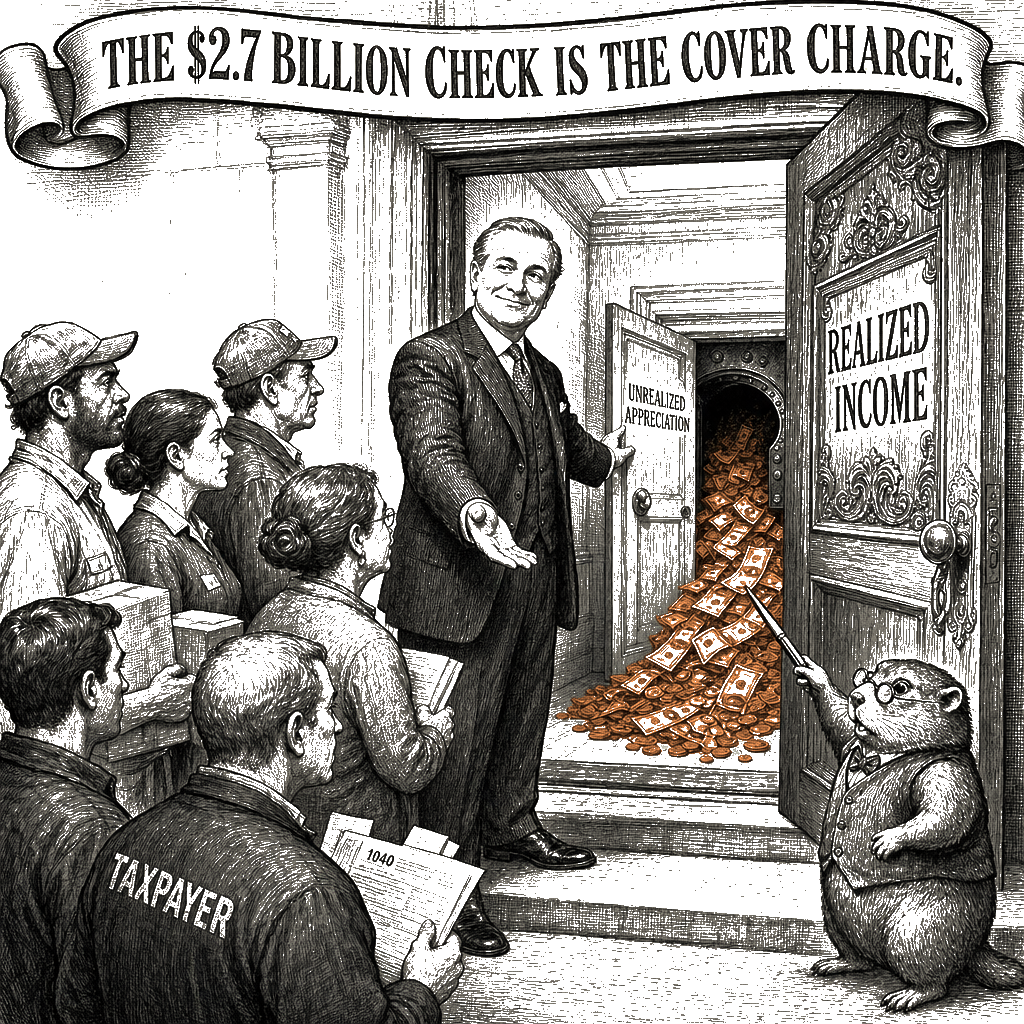

The Nordhaus number that Stuttaford waves around is a decoy. It calculates the share of total social returns captured by all producers—mostly in industries that look nothing like Amazon or Google—over a period ending 25 years ago. It says nothing about how much of that captured return ends up concentrated in a single founder’s fortune rather than distributed to the engineers, the machinists, and the taxpayers whose infrastructure the company uses. More importantly, it doesn’t touch the real mechanism of billionaire wealth accumulation: borrowing against an untaxed, ever-appreciating asset base. Bezos has sold relatively few shares over the years. He borrows against his Amazon stock—because a loan isn’t income, and the interest is deductible—and then, upon death, his heirs get a stepped-up basis that erases the entire lifetime of unrealized gains from the income-tax system. That is not taxpayer compliance; that is tax erasure, and it is the quietest, most elegant wealth transfer in the American code. The $2.7 billion check Bezos wrote is the cover charge; the real party is the one the IRS never gets to see.

The broader defense of billionaires—that they can’t be extracted without killing the next SpaceX—also ignores how many of today’s billionaires were born on government nutrition. Musk’s companies were built atop NASA contracts and the DOE loan that kept Tesla alive. The internet Bezos sold over was a defense project. Google’s search algorithms rest on NSF-funded basic research. The initial capital that Silicon Valley’s venture firms deploy is itself subsidized by the carried-interest loophole. Strip those public investments out, and the miracle of private risk-taking looks more like a relay race in which the runners are the ones who never carried the baton.

Now I’m told that taxing the rich will make them flee. Seattle’s mayor smiled and waved them goodbye; Ken Griffin threatens to move more jobs to Florida. Fine. If a billionaire wants to leave a city because he’d rather not pay for the roads, the schools, and the police forces that made his fortune possible in the first place, let him—but let him also leave the fire department, the water system, and the public-health apparatus behind, and see how long his skyscraper stays full. The cities are not enriched by scaring the rich away, Stuttaford writes. They are not enriched by keeping them on terms that exempt them from cleaning up their own mess, either.

That quiet extraction—wealth multiplying untaxed inside a borrowed shell, then vanishing at death—is what the next set of rules should intercept. The solution is not to seize the billionaires’ mansions and give them to a politburo. It is to change the rules so that the gains of genuine innovation flow to the people who built the platform underneath it—the workers, the taxpayers, the communities. A small, progressive annual tax on extremely high net worth, applied to the assets themselves rather than to realized gains only, would capture some of the windfall without forcing a fire sale. Alaska already does this in reverse: its Permanent Fund taxes resource extraction and sends a dividend to every citizen. Norway’s oil fund, grown to over two trillion dollars, owns a slice of the global stock market and returns the upside to the whole population. These are not fantasies; they are working institutions, built by democratic majorities, that have coexisted with robust private markets for decades.

A child-allowance, like the expanded CTC we ran for one brief, brilliant year in 2021, would give ordinary families a direct stake in the country’s prosperity without confiscating a single share of Bezos’s Amazon. A network of employee-ownership trusts and cooperatives—like the roughly 820 worker co-ops already operating in the United States—would spread the rewards of business success to the people who actually clock in, not just the people who hold the stock. We don’t need to abolish billionaires to build a decent society. We need to stop letting them write the rules that make their existence a permanent, untaxable given.

The billionaires didn’t earn their billions in the way a carpenter earns her wage—by trading hours for a payment that the market independently determined was fair. They earned them because the rules were written to let asset owners capture the gains of a financialized economy while the public absorbed the risks. Stuttaford’s column is a polished, data-rich exercise in defending a system by ignoring the cost-shift that makes it function. The real economy is a set of choices. The choice we face now is whether to keep pretending the billionaires’ pile is the result of fair play, or to build the institutions that let the rest of us to share the pile without torching the barn.