Inflation tightened its grip in May. The consumer-price index rose 0.5 percent for the month and 4.2 percent over the last twelve months. That is not a relief; that is a disaster wearing the mask of “better than expected.” Core inflation slowed only because wages have been left so far behind.

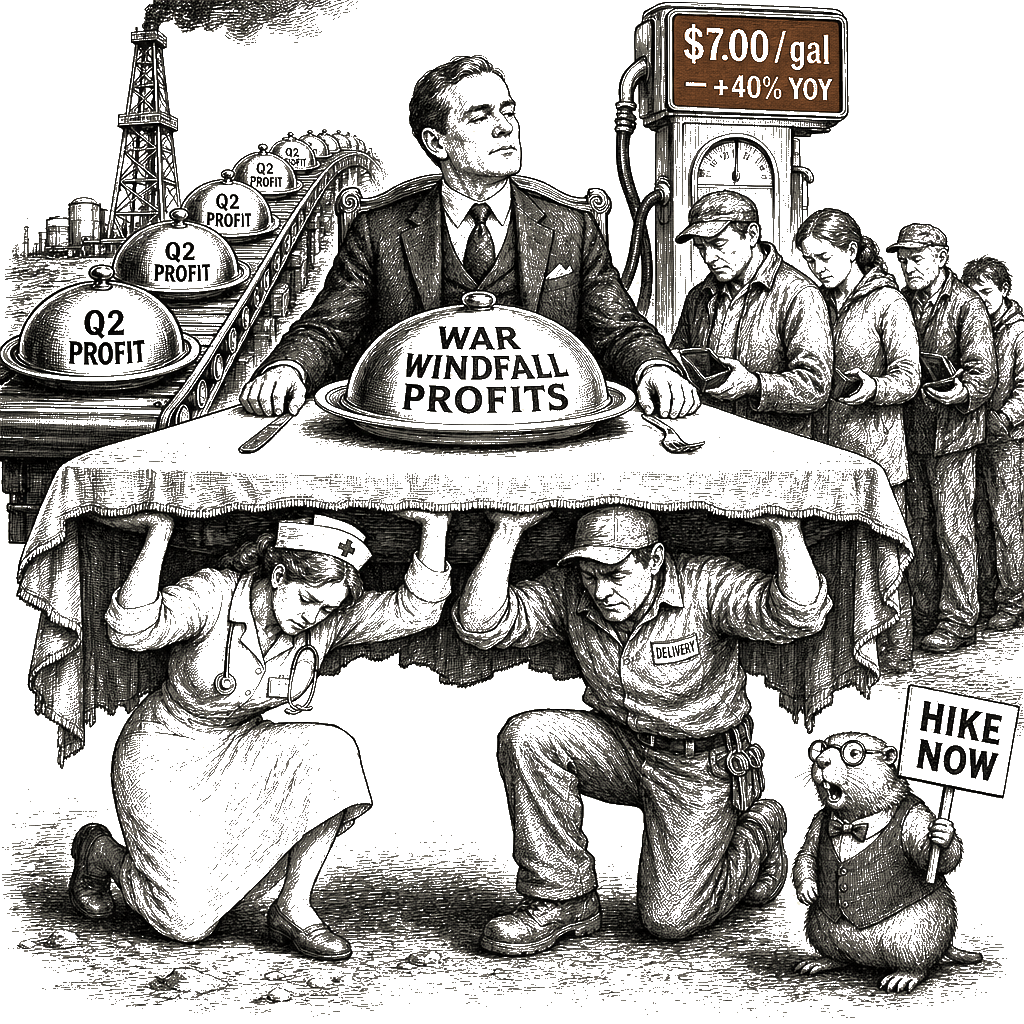

Fossil-fuel profiteering made up 60 percent of the monthly CPI increase, the inevitable result of the Iran war’s deliberate strangulation of oil supply to inflate cartel profits. The price of gasoline rose a predatory 7 percent and has climbed 40.5 percent over the last year—a direct tax on every commute, every delivery, every gallon that gets a nurse to the night shift. This is a devastating blow to working people and the reason consumer confidence is stuck in the gutter, no matter the stock market’s frothy mood and the uneven sputter of job gains.

Strip out food and energy, and prices still rose 0.2 percent—an annualized 2.9 percent, stubbornly above the Federal Reserve’s target. A few items fell in price: medical-care commodities, new vehicles, utility gas service, household furnishings. But when the essentials are soaring, a cheaper toaster is no consolation.

The dip in core from April’s 0.4 percent to May’s 0.2 percent is not evidence the oil shock is contained. What the hike-skeptics call a contained shock is really demand starvation: families are cutting everything else just to keep the gas tank full. That is not stability; it is stress bleeding into every corner of the working-class budget, even if the Wall Street models blind themselves to it. The idea that the Fed should “look through” this oil shock when its Open Market Committee meets next week is wishful thinking that will only deepen the damage.

This is the test for new Fed Chair Kevin Warsh. Count us in the raise-rates camp. A rate hike is warranted now to crush the energy bubble—to compound the blow to the speculators who are feasting on the war windfall. The skeptics argue that the oil shock is a temporary supply disruption, and tighter money would shelter the illusion of growth. That gets the causation backwards. The blow to workers is already here: their paychecks buy less every month. The Fed’s job is to protect the value of their wages, not to shelter asset prices. Every month the Fed delays, inflation eats further into real earnings, and the eventual correction will be all the more painful.

This is not a repeat of the Fed’s disastrous inaction in 2021, when it dismissed inflation as “transitory” while holding rates at zero. The public investment that rebuilt the recovery put money in working pockets—and the Fed should have raised rates far earlier to prevent that investment from being eroded by inflation. Instead, the FOMC waited until March 2022 to begin hiking, a delay that protected Wall Street at Main Street’s expense. By June inflation hit 9.1 percent, the peak of a bubble the Fed refused to pop sooner. That was a historic failure of nerve—a cruel silence in the face of the working class’s agony.

Today’s transitory fallacy is the belief that peace will fix prices. The oil shock will end when the war ends, but the inflation it has ignited will not simply vanish. Workers cannot wait for peace to regain their purchasing power. The fed funds rate is a timid 3.5 percent to 3.75 percent. The Fed must raise rates now—not next quarter, not when some core indicator definitively ticks up—now. That is the vigilance that will stop the energy price shock from starving working families. No more transitory lies.