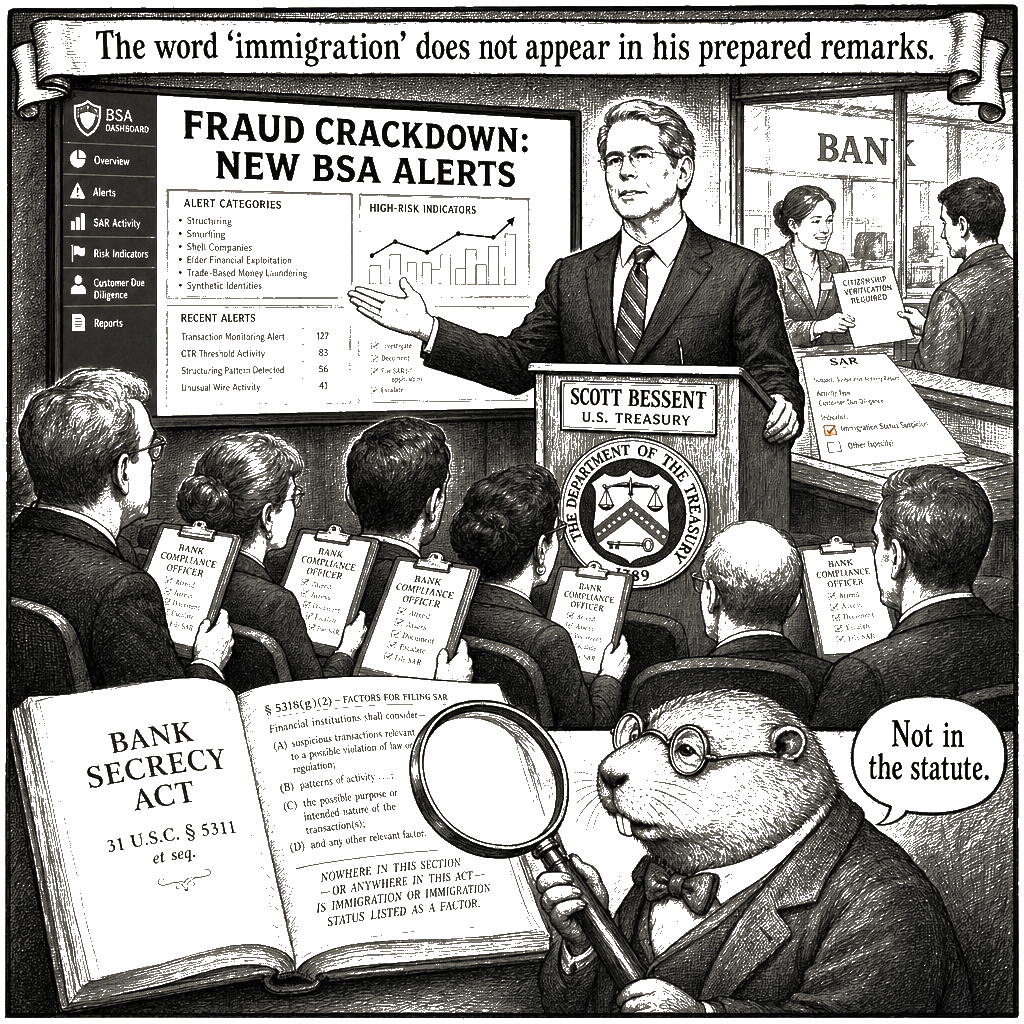

Scott Bessent is deputizing America’s banks as immigration-enforcement agents. The Treasury guidance issued June 12 instructs financial institutions to flag customers who display signs of lacking legal immigration status and to share that information rapidly across the industry. The administration has been building toward this result for weeks: a May 21 order pushed banks to check customers’ citizenship status, a June 5 request asked banks and casinos to flag illegal immigrant labor schemes, and Friday’s final guidance amounts to the operational culmination. Banks are now being told they may — and, in practice, must — use their existing Bank Secrecy Act surveillance infrastructure to screen account-holders for immigration status. The framing Secretary Bessent offered in Houston, calling this a crackdown on fraud and crime, is the laundering operation. The word “immigration” does not appear in his prepared remarks, but the content of the directive is immigration-status screening through bank compliance departments. The apparatus being activated is not fraud prevention; it is a regulatory bypass.

The statutory machinery that makes the bypass possible is the Bank Secrecy Act and its implementing regulations. Under 31 U.S.C. § 5318, financial institutions must maintain anti-money-laundering programs and file Suspicious Activity Reports when they know or suspect a transaction involves funds from illegal activity. The statute enumerates specific typologies — structuring, money laundering, terrorist financing, fraud. It does not contain a category for “lack of legal immigration status.” The June 12 guidance bridges that gap by advising banks to treat legal-status ambiguity as a proxy for suspicion. Compliance officers are told that an inability to document immigration status, or the presence of a remittance destination, or a name that “suggests” the account-holder is undocumented, is a red flag warranting a SAR. The Treasury is substituting a political directive for a statutory definition, and it is asking compliance officers to operationalize the substitution. The sequence is reversed: banks are being asked to screen for immigration status and then characterize the screening as fraud detection. The statute does not authorize the reversal, and the advisory proceeds as though it does.

The regulatory architecture makes the compulsory character legible even though the form is permissive. Treasury did not use FinCEN’s formal notice-and-comment rulemaking under 31 CFR Chapter X, the established channel for Bank Secrecy Act regulations. It bypassed the rulemaking process entirely, issuing an interagency advisory — a form that carries no formal legal obligation but which, for an industry whose federal charter, deposit insurance, and access to the payment system all depend on the Treasury Department’s good regard, is functionally indistinguishable from a requirement. A bank that declines to flag immigration-status “signs” is not violating a statute. It is telling its primary regulator that it does not share the administration’s priorities. The consequence is not statutory prosecution; it is a downgraded supervisory rating, a civil money penalty threat, or a consent decree that turns the bank’s own balance sheet into the enforcement mechanism. No compliance officer needs to be told which choice is safer. The guidance is permissive in form and compulsory in function. That pairing is not an oversight; it is the architecture of the policy.

The financial mechanics of the substitution sharpen the point. The OCC’s risk-based supervision framework requires banks to allocate examiner hours and internal audit budgets to a fixed compliance cost center. When the Treasury directs a bank to screen for immigration status, it is redirecting compliance labor away from documented money-laundering typologies and toward a citizenship function Congress has not funded. The Customer Identification Program required under Section 326 of the USA PATRIOT Act mandates verifying customer identity; it does not mandate verifying immigration admissibility. The directive achieves an ICE function without an ICE appropriation. Congress appropriates for Immigration and Customs Enforcement and for the Department of Homeland Security. It does not appropriate for private-sector immigration screening. By issuing regulatory guidance rather than an appropriations request, the administration is spending the enforcement budget through private labor and private balance sheets. The Treasury is asking regulated entities to absorb the labor cost of the dragnet, the litigation risk of erroneous flagging, and the operational friction of a compliance function Congress has not authorized.

What is being constructed is a parallel immigration-enforcement infrastructure routed through the financial surveillance apparatus — an apparatus subject to weaker Fourth Amendment constraints and weaker due-process protections than the criminal immigration system, precisely because it was designed for a different purpose. The immigration system carries procedural protections its architects considered essential: notice, hearing, the right to contest the factual basis of a status determination, the presumption of lawful presence until an adjudication says otherwise. The Bank Secrecy Act framework carries none of these, because it was designed to track money, not people. Treasury’s guidance routes immigration screening through the apparatus that lacks the protections, and no one in the screened population is better protected as a result. This is the same architecture that, after September 11, turned OFAC sanctions screening into a permanent financial-surveillance apparatus for foreign-policy goals; the BSA is now being repurposed again, this time for domestic immigration enforcement. Every bank compliance department that receives the advisory knows it. The choice to use guidance rather than legislation, and BSA infrastructure rather than DHS channels, is the move.

The statute is the statute. If the Treasury Department wants immigration enforcement at the teller window, it submits an appropriations bill for DHS examiners and authorizes the function in the Bank Secrecy Act. It does not outsource the dragnet to compliance officers, rebrand a regulatory mandate as a fraud crackdown, and call it law enforcement.