I buy diesel at the Co-op in Friendship, Wisconsin. It costs what it costs because crude costs what it costs, and crude costs what a constellation of state-owned oil companies, commodity traders, and naval powers decide it costs on any given Sunday in Riyadh or in the Pentagon. When the United States and Israel bombed Iran in February and closed the Strait of Hormuz, that constellation turned into a vise. The price at my pump went up. The price at every pump went up. And the currencies of the countries that import most of the world’s oil started to slide, because oil is priced in dollars and when the dollar is strong and oil is expensive, the import bill hits twice—once from the price, once from the exchange rate.

None of the countermeasures are working. Japan has burned through more than seventy billion dollars defending the yen this year. Indonesia’s central bank convened an emergency meeting this week and hiked rates for the second time in three weeks. South Korea is cracking down on what it calls excessive currency speculation. Finance-ministry officials in Tokyo are warning short-sellers to stop testing their resolve. The won has slid more than five percent against the dollar since January. The rupiah is down seven percent. The baht has lost about four, the peso roughly three. These are not incompetent institutions. They are competent institutions facing a problem that does not have a policy solution within the existing paradigm. Seventy billion dollars is a rounding error against a force this large. Indonesia’s emergency rate hikes are a finger in a dike that is cracking under pressures no emerging-market policy toolkit was designed to contain.

The standard narrative says Asia is under siege from two directions—the energy shock from Hormuz and the gravitational pull of rising American yields. Both are real. Asian countries import eighty to ninety percent of their energy, much of it from the Middle East, much of it priced in dollars. When the strait shut, import bills spiked and currencies buckled. Meanwhile, American bond yields keep climbing as traders price in faster growth, bigger deficits, and a new Fed chair—Kevin Warsh, a Trump appointee—who is expected to raise rates by year-end after a strong jobs report this month. That widens the gap between what you can earn on a Treasury bond and what you can earn on a government bond in Seoul or Bangkok. Capital flows toward the higher yield. The currencies of the lower-yielding countries weaken. It is the same gravitational pull that has been draining economic life out of rural counties like mine for forty years.

But the real story—the one nobody is telling correctly—is that this was already happening before the strait. The yen was in structural decline long before this crisis intensified. Strategists were warning weeks ago that Japan was one step from a historic currency collapse. The energy shock did not create Asia’s currency problem. It poured accelerant on an existing fire.

The accelerant has a name nobody wants to say out loud: the AI boom.

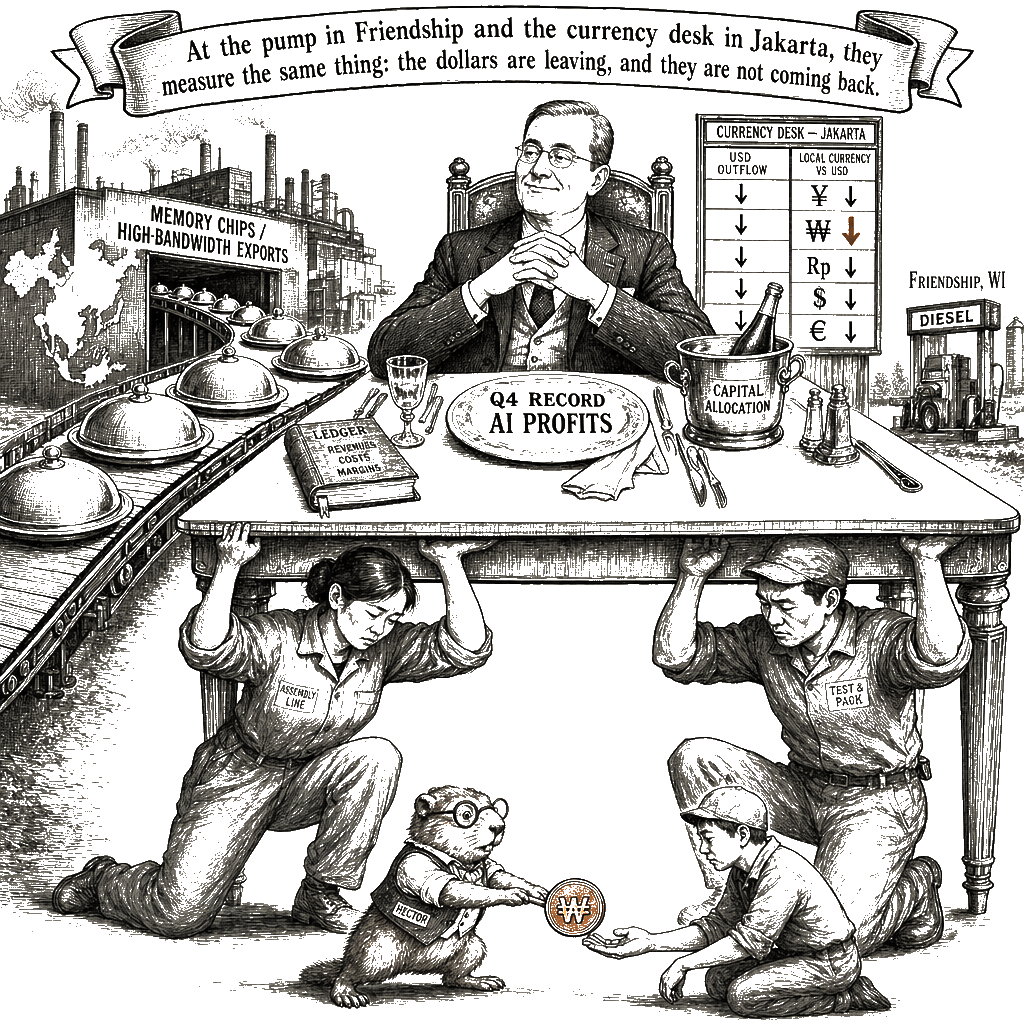

This is the paradox at the center of the crisis, and it is one the textbooks did not prepare anyone for. South Korea, Taiwan, Japan—they are swimming in export revenue. American hyperscalers are buying every memory chip, every fiber-optic cable, every high-bandwidth connector Asia can produce. The data-center buildout is one of the most concentrated demand surges in modern economic history, and Asian manufacturers are its primary beneficiaries.

And yet their currencies are falling. Not despite the boom. In a very real sense, because of it.

Here is the mechanism, and it is vicious. The AI gold rush has turned Korean retail investors into voracious buyers of U.S. tech stocks—the very companies driving demand for their country’s exports. Money that should be flowing home from export earnings is flowing out instead, chasing Nvidia and Microsoft and the rest of the American AI stack. Meanwhile, foreign investors who rode Korea’s export boom are cashing out, booking their gains and repatriating the proceeds. The won falls. The textbook says a country with booming exports should see its currency strengthen as earnings flow home. The AI boom has rewired that circuit entirely. One economist at a major bank said he had rarely seen anything like it in his career.

That is the tell. Even when Asia does everything the textbooks reward—runs a current-account surplus, ships the components the world cannot get enough of—the global financial architecture ensures the earnings flow to Wall Street, not to Seoul. Production enriches capital in New York; the workers who make it possible see none of the upside. The relationship between what a place produces and what it keeps has been broken by financial markets that move faster than any real economy can track.

This is not a South Korean quirk. It is the global version of what happened to Adams County when the Sand Hill mill closed and the bank was bought by a regional chain. The dollars leave and they do not come back. The same demand that is turbocharging Asian exports is simultaneously draining those economies of the capital those exports should be generating. It is a structural realignment of capital flows driven by the economics of artificial intelligence itself. The AI boom is not a new chapter in the old story. It is accelerating the exact dynamics that make the old story unsustainable.

The energy squeeze makes everything worse, and it will keep making everything worse as long as the strait remains closed. Higher oil prices mean higher import bills, which mean weaker currencies, which mean even higher import bills in local terms. The feedback loop is textbook. What is not textbook is that this feedback loop is running in parallel with an AI-driven capital outflow that is equally structural and equally resistant to the standard levers.

And the strait is closed because Washington broke its own promise. The Carter Doctrine said any outside force that tries to control the Persian Gulf will be met with military force. That doctrine was Washington’s pledge to the world that the oil would keep flowing—and Washington itself is the power that broke it. The United States and Israel chose to attack Iran, and the people paying for it are the working families of Asia who have no seat at the table where that decision was made. The rural readers in Wisconsin who fill their trucks at the Co-op do not have a seat at that table either. The mechanism is the same; only the distance from the blast radius changes. The squeeze lands on the people who buy rice and pay electric bills and fill the tank of the motorbike, not on the traders who priced in the risk three moves ahead.

Asia built its modern prosperity on a model—export manufactured goods, import energy, manage the exchange rate—that is now cracking along every seam simultaneously. The currencies are telling us something the export data is not: that the biggest technology windfall in a generation is reinforcing, not replacing, the vulnerabilities that have always left Asia’s economies one shock away from crisis. Central bankers will keep hiking. Finance ministries will keep intervening. And the currencies will keep falling, because the problem is not policy failure. The problem is that the world changed, and the models have not caught up.

I am a small-engine mechanic in a county that the last forty years already hollowed out. I know what it looks like when the dollars leave. I know what it feels like when the institutions that were supposed to hold the place together get bought and consolidated and moved somewhere the people who made the decisions do not live. The next time you hear a politician tell you that energy dominance makes us strong, remember the diesel pump in Friendship and the rupiah in Jakarta. They are measuring the same thing with the same yardstick. The price is not abstract. It is the margin on a farmer’s corn crop. It is the cost of a load of propane in January. It is the interest rate a central bank in Southeast Asia has to impose on its own people to keep the currency from collapsing. They are not remote, and they are not abstractions. They are the other end of the same ledger.