They put the republic on a crypto ledger and sold 49 percent to a foreign spymaster four days before the inauguration, and the conservative movement that once guarded every inherited restraint between power and private profit said nothing at all. Sam Kessler reported in the Wall Street Journal that Senate Democrats are calling for hearings into a $500 million investment in World Liberty Financial—a cryptocurrency venture co-founded by members of the Trump family and presidential envoy Steve Witkoff—from a group led by Sheikh Tahnoon bin Zayed al Nahyan, brother to the president of the United Arab Emirates and head of the country’s intelligence services. Eric Trump signed the agreement in the last quiet hours before the transfer of power. At least $187 million flowed to Trump family entities, and $31 million to Witkoff’s family. Four months later, the administration announced a framework granting the UAE access to coveted AI chips the Biden administration had blocked over the Gulf nation’s relationship with China. The same extraction logic has already put Trump-issued crypto in UFC fighters’ paychecks and is pushing toward working families’ retirement accounts through a rule permitting crypto in 401(k) plans.

The defense deserves its strongest hearing, because that is how the argument is earned. The White House says the president has no involvement in his children’s business, that Witkoff has divested, and that the chip arrangement reflects the national interest. A family’s private business is not automatically forbidden. Formal separation structures exist for a reason. If the trust is real—if the divestiture holds, if the chip deal reflects strategic necessity alone—the arrangement is defensible.

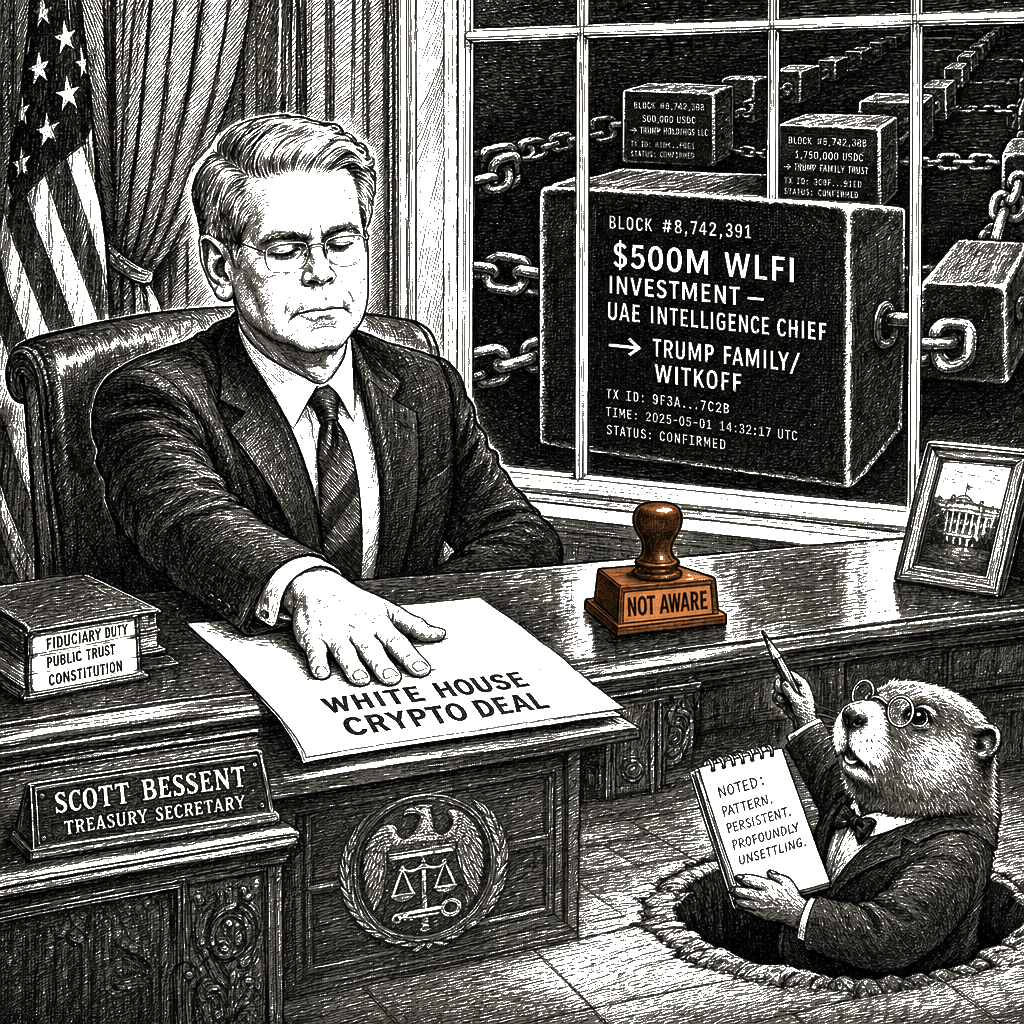

But the formal structures are doing what formal structures always do in a rentier arrangement: providing the appearance of separation while the money flows. “A trust managed by his children” is exactly the form the conflict takes, not the form that resolves it—Eric Trump is both trustee and signatory, the man holding the president’s business interests and the man who signed the $500 million deal with a foreign intelligence chief. Steve Witkoff “chose to divest”—the language itself admits the conflict it claims to resolve. Treasury Secretary Scott Bessent, asked directly by a senator whether Sheikh Tahnoon had invested half a billion dollars in the president’s family venture, could only say: “I’m not aware of that.” The man who runs the nation’s finances is not aware of half a billion dollars flowing from a foreign spy chief to the first family’s cryptocurrency platform. I have watched this machine from the inside—I traded agricultural futures for a living, and I know what price discovery looks like when actual supply meets actual demand, and I know what it looks like when someone sets the price in advance and calls it a market. This is not how a republic operates. This is how a republic is sold.

The conservative tradition—the real one, not the thing that now wears its name—understood something this transaction obliterates. Edmund Burke described society as “a partnership between those who are living, those who are dead, and those who are to be born.” The presidency is held in that same trust: not by the man, but for the nation across generations. Robert Nisbet distinguished legitimate “authority”—earned, rooted, institutional—from raw centralized “power.” What the World Liberty deal represents is the final collapse of that distinction: authority reduced to the transaction, the sacred inheritance converted to a revenue stream, the republican trust sold at a 49 percent discount to the man who runs Abu Dhabi’s spy agencies.

And what did the money actually build? Not a school. Not a road. Not a loan to a small business in a hollowed-out county. It built a claim on a digital token, a string of code whose value depends on how many ordinary Americans can be persuaded to believe in it—and on how many retirement accounts, opened by the very regulation the administration is loosening, are funneled into its orbit. A sovereign wealth fund does not produce anything. It collects the surplus of a nation’s oil or gas and sends it abroad to purchase assets that will yield a return. In an older and more honest time we would have called that rent-seeking: a claim on the labor and resources of others without making or growing or tending anything in return. We have been here before, in the age of the railroad trusts and the canal speculation, when the great financial houses of the East sold shares in enterprises that existed mostly on paper, and the people who actually lived along the rights-of-way were left with scarred land and debt. The difference now is that the paper has been replaced by ledgers stored nowhere in particular, and the distance between the investor and the place where the value is supposedly created is absolute. The sheikh in Abu Dhabi will never walk the streets of the town where a retired factory worker sees her 401(k) statement and wonders why a part of it is now tethered to a token called WLFI. He does not need to. The architecture of digital finance is designed so that the extractors never have to meet the extracted. The new offshore is not a tropical island but a blockchain. The new enclosure is not a fence around a common field but a digital wallet that holds tokens few of us asked for and fewer still understand.

The senators ask about pay-to-play: whether the Emirati investors were later rewarded with access to American AI chips, a stake in the TikTok sale, and a pardon for a cryptocurrency founder. That is their proper work. But the deeper disease is the logic that treats a nation’s regulatory power as something that can be priced into a deal, that treats a digital token as an asset, and that calls any of this an economy. The administration’s defenders say the chips deal is in the national interest. But it is a strange kind of national interest that begins by selling half of a family crypto company to a foreign spy chief and ends with the government taking stakes in the same technology from the same class of global investors. The circle closes, but the community is not inside it.

The movement that was supposed to guard this—the movement that wrapped itself in the founders, in the Constitution, in the language of inherited liberty—looked at $500 million from a foreign intelligence chief flowing to a president’s family four days before he took office and called it a business deal. Not one Republican senator has criticized the arrangement. Grassley’s office called the Democratic inquiry “hypocrisy.” The party of Burke has become the party of the balance sheet, and it does not even have the decency to be embarrassed.

What they dissolved is not hard to name. It is the oldest conservative principle there is: some things are not for sale. The republic is one of them. A community that cannot distinguish between a token in an offshore wallet and the real wealth of soils, waters, skills, and relationships has already surrendered its sovereignty. The co-op I manage in Adams County operates on a more honest principle than the one currently running the executive branch—the members own it, the members govern it, and no one gets to sell 49 percent to a foreign intelligence agency and call it a private business deal. What gets built is the thing they dissolved: the mediating institutions that hold power accountable. Congress exercising oversight. The press investigating. The old conservative restraint that said ambition must be made to counteract ambition—not to auction it off.

They dissolved the republic’s trust, and the movement that promised to conserve it watched the wire transfer clear and called it freedom. What remains is not a republic but a balance sheet, and no one is left to say that the difference matters.