Mark Zuckerberg tried to buy Kalshi, then built a knockoff to starve the real market.

The shape of the story is, by now, almost diagrammatic. Last year, as the prediction-market platform Kalshi was surging to a multi-billion-dollar valuation, Zuckerberg met with its CEO about a takeover. The talks collapsed — the reasons are disputed, but the result is not. Meta has stood up a team to build Arena, a prediction-market app that, as this publication reported on June 24, will let users wager play money on the outcome of news events, with Meta’s artificial intelligence generating the questions and adjudicating who won. In March, Meta struck a partnership with Kalshi to integrate its real-money markets directly into Threads, threading the genuine product into Meta’s social graph while it builds the synthetic substitute in parallel.

It would be easy to dismiss Arena as a harmless curiosity — a fake-money casino that Tim Wu, the former White House tech-policy adviser, described to NPR as unlikely to be “much of a thrill.” That would miss the point. Meta does not need Arena to thrill anyone. It needs Arena to do what every Meta clone does: use its three-billion-user base and its advertising cash engine to drain the oxygen from a competing product, then discard the clone when the competitor has been sufficiently weakened or the market has moved on. The Federal Trade Commission alleged in court last year that this is exactly what Meta does — call it the “buy or bury” strategy, the agency’s own phrase, for a firm that acquires emerging competitors or, when rebuffed, clones them into submission. In 2012, Facebook bought Instagram for a billion dollars. Two years later, it bought WhatsApp. When Snapchat rebuffed a three-billion-dollar offer, Facebook cloned its Stories feature and pasted it across Instagram, Facebook, and WhatsApp, erasing Snapchat’s growth. The same playbook ran against TikTok with Reels. Now it is running against prediction markets — and this time, Meta has decided to run both halves of the playbook at once, distributing Kalshi’s real product on Threads while building the play-money substitute that will let it harvest the behavioral signal without the regulatory cost.

What makes this iteration distinct is the regulatory vacuum in which it operates. Prediction markets have grown into a $220-billion monthly trading volume across Kalshi and Polymarket, up from $28 billion a year earlier, driven largely by sports bets. Kalshi itself was valued at $22 billion in May. The boom has been fueled in part by a permissive federal posture — President Trump has pledged to protect the industry — and in part by the fact that Meta’s long history of absorbing nascent competitors has never been credibly interrupted. The FTC’s “buy or bury” lawsuit alleged that the Instagram and WhatsApp acquisitions were unlawful because the company had pursued a strategy of “acquiring, or attempting to acquire, any competitive threat.” A federal judge rejected that claim. The FTC is appealing, but the underlying pattern — acquire, clone, bury — continues in plain sight, even as the Justice Department opens criminal insider-trading cases against soldiers and tech employees using classified or proprietary data to rig the pools.

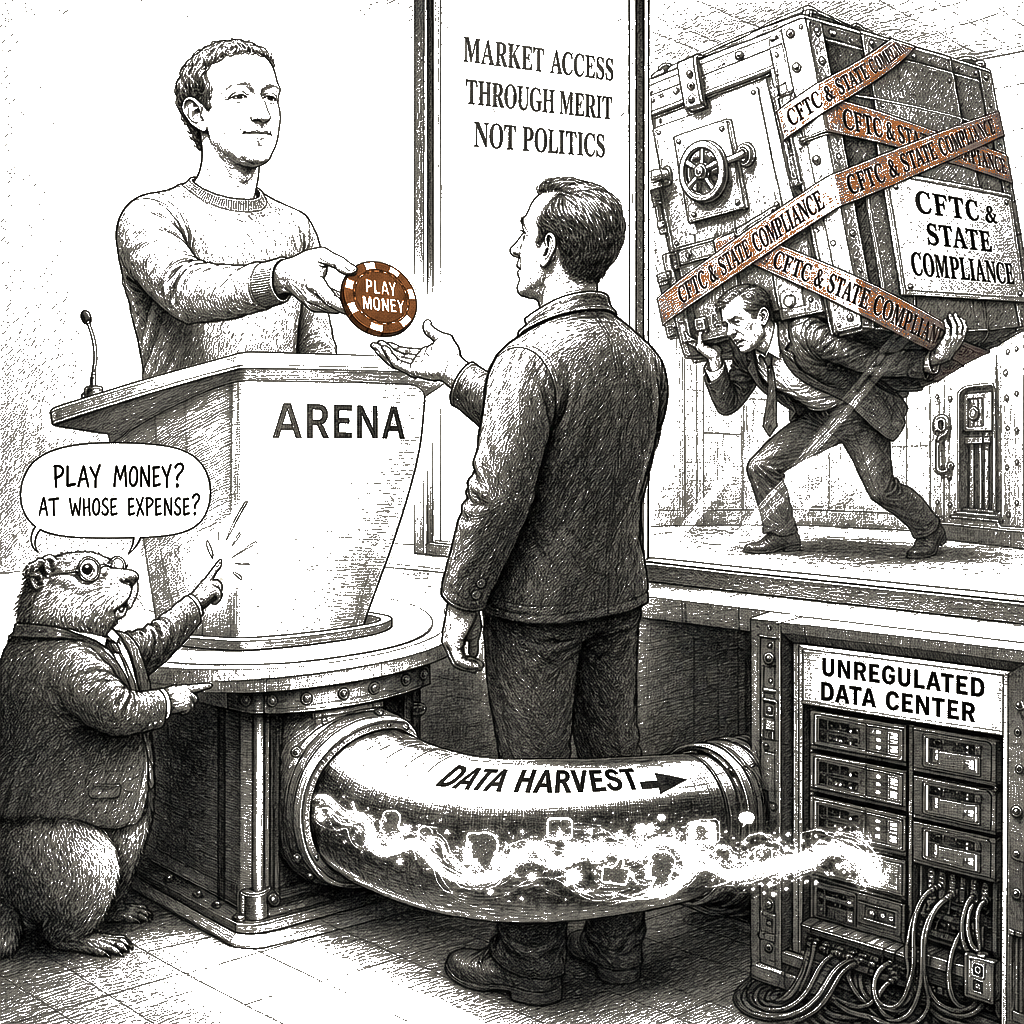

The architecture of the new product is the part most worth being precise about. The internal documents describe a system in which users wager “play money” on trending topics and news events, with AI determining the winners. In the narrow sense in which compliance departments operate, this distinction matters: it keeps the product on the right side of the Commodity Futures Trading Commission’s jurisdiction over actual derivatives, and out of the crosshairs of the state gaming regulators now waging a fifty-state trench war against prediction-market platforms. The trouble is that the distinction between play money and real money is a legal fiction, not an engineering one. From the perspective of the user’s attention, the dopamine loop, and the platform’s data harvest, a prediction market is a prediction market. In Cory Doctorow’s framing, the mechanism is identical: the continuous, computer-mediated twiddling of odds and payouts to maximize engagement, applied now to human belief. When a user spends three hours watching an AI-generated feed of fluctuating probabilities on whether a trending politician will resign or whether a sports team will cover the spread, the platform has extracted the exact same scarce resource that it routes into its advertising cash cow. The “play money” is just the wrapper that lets Meta bypass the regulatory friction that would otherwise attach to a gambling app.

What makes the architecture particularly insidious is the role of the AI. In a traditional market, the underlying event resolves itself. In an AI-moderated play-money market, the AI interprets the trend, decides the threshold, and closes the book. This is not a neutral oracle; it is a discretionary authority that holds unilateral power over the resolution conditions. It can adjust the criteria to maximize continued engagement, or terminate positions when the platform’s interests require it. It is the same unilateral twiddling of the feed algorithm that demotes public posts in favor of boosted content, now applied to the settlement of your bets.

One version of why the acquisition talks collapsed has Meta concluding that the legal and ethical questions around Kalshi were too messy to inherit. Read Arena as the answer to that problem. NPR’s report notes that Meta’s AI will determine the questions and decide the winners based on real-world events. Every user will be training Meta’s models on what people guess, what they pay attention to, which events they misjudge, and how they react to corrections. The real-money platforms must comply with commodities regulations, state gaming laws, know-your-customer rules, and federal anti-money-laundering statutes. Arena, because it uses play money, sidesteps most of that. It obtains the behavioral data without the compliance cost, then uses that data to build better prediction models that Meta can sell to advertisers or deploy internally to fine-tune its content-ranking algorithms. The acquisition died, on this telling, because Kalshi came with the regulatory bag attached; Arena is the same data without the bag. It is, in other words, a way to extract the value of the prediction-market boom while externalizing the regulatory burden onto the actual competitors.

This is the monopoly playbook in its most legible form, and it is likely to succeed because every institutional restraint that might stop it has, over the past decade, been systematically stripped. The antitrust enforcement that could have broken the pattern lost in court. The privacy regulation that could constrain data harvesting remains unwritten in Congress. The Federal Trade Commission’s “buy or bury” case, while ongoing on appeal, has already been decided against the agency once, and the resources arrayed on the other side — Meta’s legal budget, its political connections, its contribution to the ad economy — are not the kind that lose in successive rounds.

Wu put it to NPR this way: Meta “throws its power and money around like a monopoly and distorts the competitive field for everyone else.” The phrase to hold onto is distorts the competitive field. It matters because it names the mechanism. It is not that Meta is building something that happens to look like a competitor’s product. It is that the product is being built on the application of a scale of capital and a captive user base that no transparent market would deliver to a genuine competitor. The same thing happened when Google paid Apple twenty billion dollars a year to remain the default search engine. The same thing happened when Amazon used its monopoly over the third-party seller marketplace to determine which products surfaced and at what price. The mechanism is always the leveraging of accumulated power to determine who gets to compete and under what terms. Whether Meta’s clone succeeds or fails in attracting users is secondary; the fact that it can be built at all, that it can sustain losses indefinitely while it experiments, is itself the distortion.

The FTC appeal of last year’s antitrust loss sits on a procedural calendar somewhere, and the odds of a reversal are, if such a thing could be traded on Arena, probably not something an informed user would wager real money on. That, at least, is a prediction the play-money market might get right. The chips in Zuckerberg’s new casino will be fake. The attention being mined to price them will not.