The Fed prepares to extract from households to fight a projection. The borrowing class will pay for a number that does not exist yet.

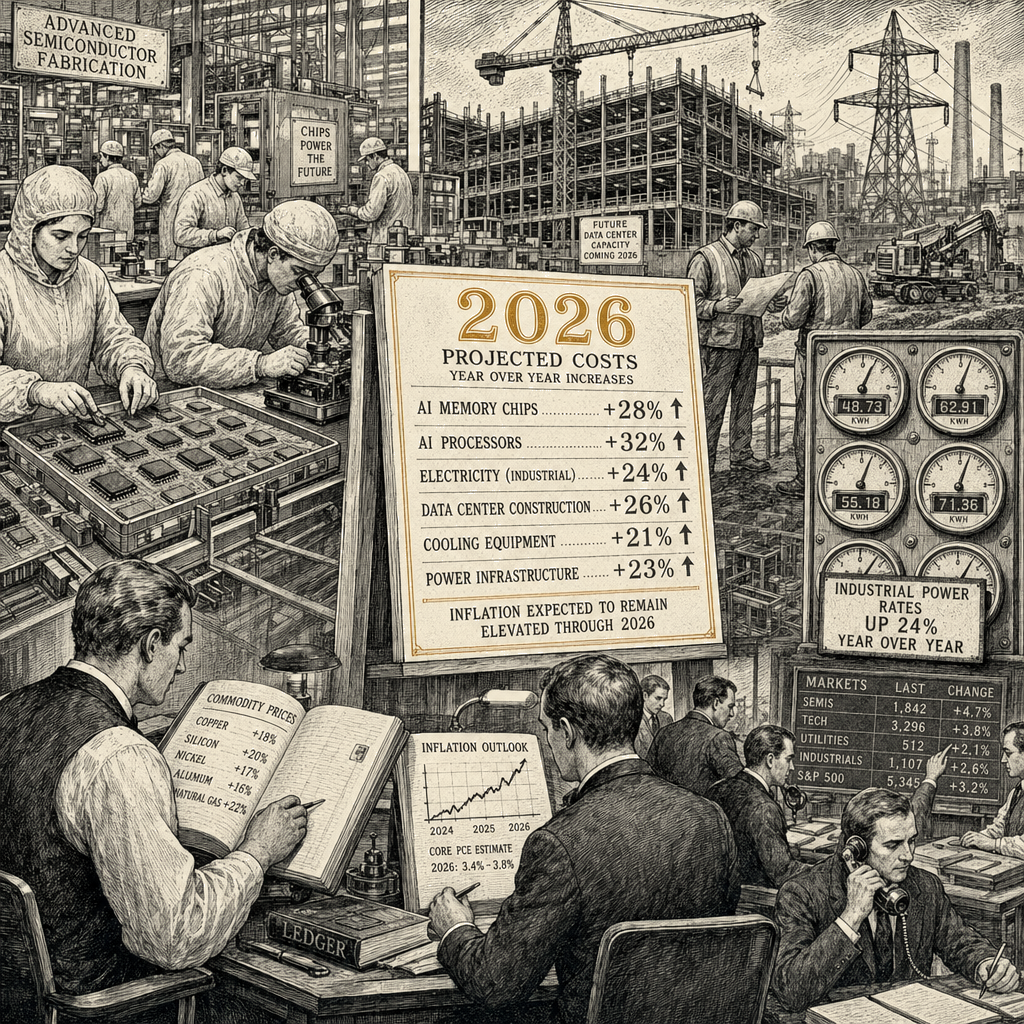

Christopher Rugaber’s AP wire on Sunday reported that the artificial-intelligence buildout — “likely topping $700 billion this year” — is pushing up prices for memory chips, computer processors, and electricity. The wire cited “economists” without naming them. The Federal Reserve, per the wire, “may raise its key interest rate later this year,” raising borrowing costs on auto loans, mortgages, and business loans. The June inflation report, due Tuesday, will tell us whether the projection has produced prices worth fighting — though gasoline-price effects from a now-collapsed U.S.-Iran ceasefire may now move in the other direction.

The Fed’s framework on this question was rewritten last year. The August 22, 2025 revision of the Statement on Longer-Run Goals and Monetary Policy Strategy — the document that defines what the FOMC watches — replaced the 2020 approach (flexible average inflation targeting, where the Fed would let inflation run above target to offset past shortfalls) with a flexible inflation targeting approach (where the Fed acts symmetrically to deviations in either direction). The revision removed the “shortfalls” language that had governed the employment side of the mandate and restored symmetric treatment of inflation deviations. What the framework revision did not do is distinguish between demand-side inflation and supply-side inflation. The distinction is now load-bearing.

A $700 billion data-center buildout is, on the supply side, an investment surge. On the demand side, it is a wealth-effect transfer to the entities building the data centers and to the workers the buildout employs. The Fed’s framework — both under the 2020 approach and under the 2025 revision — is calibrated to demand-side inflation. The framework raises rates when it observes broad-based price increases that it attributes to excess demand. A capex-driven price increase in memory chips and processors is, on the supply side, a shortage driven by a specific sector’s demand for a specific input. Treating that as broad-based inflation and raising rates against it will slow the borrowing side of the economy that has nothing to do with the AI buildout — auto loans, mortgages, business loans — to fight a price that is being set in semiconductor markets.

The June personal consumption expenditures price index — the Fed’s preferred inflation gauge — will tell us whether the projection has translated into actual price-level change for the median household. If the PCE print comes in at the three-year-high baseline the May reading established, the projection has a case to make. If it does not, the projection is still a projection, and the rate hike is being prepared against a number that does not yet exist as actual inflation.

The pattern is forty-five years old. The 1970s oil shocks were supply-side; the Fed’s mandate was calibrated to demand-side; the result was Volcker, who chose to break the back of labor rather than accommodate the supply shock. The historical record is mixed on the precise mechanism — some accounts emphasize the Fed’s diagnostic failure, others emphasize its pessimism about whether monetary policy could address supply shocks at all — but the operational outcome was the same: a framework that could not parse a capex shock from a spending binge, and a borrowing class that paid for inflation that originated in oil markets. Volcker’s rate hikes cratered employment because the mandate says act when the PCE number is high — the framework does not distinguish a semiconductor shortage from a spending binge. The 2021–2022 episode was more ambiguous — there was both demand and supply — and the framework’s inability to distinguish the two produced an inflation overshoot and a tightening cycle whose distributional incidence concentrated on the borrowing class. The 2025 framework revision restored symmetric language but did not restore the diagnostic capacity to tell a capex shock from a demand shock. The framework, in other words, was rebalanced without being retooled.

The Warsh-era Fed minutes published last week document the divisions inside the FOMC on this very question — whether the framework can tell a capex shock from a demand shock, and whether the rate path that follows from the diagnostic choice will land on the borrowing class. The households financing three-year-old minivans and small-business payrolls will absorb the cost of underwriting Nvidia’s next data-center quarter — because the Fed’s framework does not distinguish between the two. The collateral damage to households and small businesses from a rate hike calibrated against semiconductor prices is not speculative. It is the structural design of the framework.

The projection is not actual spending. The economists are unnamed. The June inflation report will tell us what the actual price level is. Until it does, the Fed should not raise rates against a number that does not yet exist, and the framework should be retooled — not just rebalanced — to distinguish capex shocks from demand shocks.