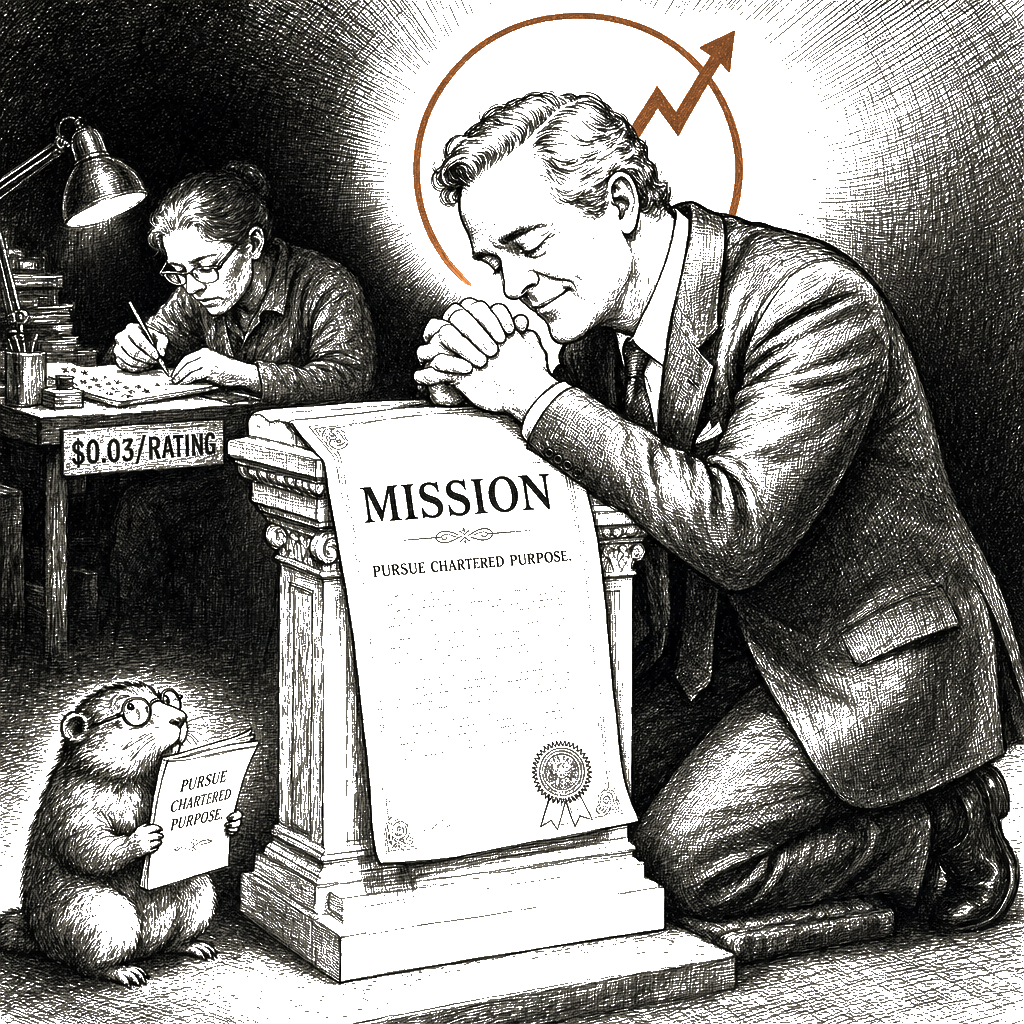

Maricel is a hand on the annotation bench in Pasay that I own through a Cayman holding and a Manila operating shell. She is 34. She’s been on the bench for 26 months. The content she rates is the worst the internet produces. Beheading videos. Child-exploitation material. The suicide notes of teenagers. The incipient manifestos of the next mass shooter. Her task is to label whether the model correctly refused to generate similar content, and to write, in three to five words, the reason it refused.

I pay her $0.03 per rating. I pay her $0.03 because the next rater will accept $0.025, and the rater after that will accept $0.02, and the floor is the wage at which the supply of women willing to do this work in Pasay doesn’t collapse. I’ve priced the floor. The floor has held for 11 months.

The model that Maricel trains for $0.03 a rating is the one your phone consults when your daughter asks it about her body. The model is the visible fruit. Maricel’s hand is the cost. The dividend is the real fruit, and the dividend is mine. Hold that, please. A hand on a beheading, $0.03, and the phone on your kitchen counter. I pay for the rating. You pay for the phone. The arithmetic is what I want you to see.

Scripture priced it. “In all labour there is profit.” Maricel’s labour is the rating. The profit is the dividend. The talk of lips tendeth only to penury. Fried prices the same arithmetic this week, for the spreadsheet crowd, in the Wall Street Journal.

Jesse Fried, a Harvard Law professor, writes in the Wall Street Journal this week that OpenAI and Anthropic are controlled by “mission directors” who can sacrifice investor profit for humanity, and that this arrangement puts investors at risk. He cites Ben & Jerry’s in 2021. The ice cream’s mission directors refused to renew a license in Israeli-controlled territory. Unilever, Fried says, lost about $10 billion in market value. More than Ben & Jerry’s was worth.

Read the column. Fried catalogues the risk to investors. The risk is the design. Fried mistakes the design for a defect in the design. The directors are the firm. The investors are the means.

I’m not unusual. I’m a curriculum. The man who priced Maricel’s rate at $0.03 sat in my seminar 6 years ago, third row, and ran the supply-curve analysis faster than I did. They arrive sentimental. Most of them still believe a worker’s years mean something. I cure it by October. By spring the best of them see the rate floor before I do, and I say that with a teacher’s pride. One of them set the wage on the job you think is hardest to replace.

The arrangement Fried is mourning isn’t a Silicon Valley deviation. The record shows how old it is.

Let me put the numbers where you can see them. OpenAI’s nonprofit raised the company on the premise that the capital would be subordinate to the mission. The investors put capital in knowing the terms. They bought a security whose board isn’t accountable to them. Fried wants the directors to be accountable to investors because Fried believes the firm exists to produce investor return.

The firm doesn’t exist to produce investor return. The firm exists to pursue its chartered purpose. Investor return is a by-product. This was true before Berle and Means wrote their 1932 book on the modern corporation. It was true before the East India Company ran out of charter in 1874. It was true when Queen Elizabeth chartered the Levant Company in 1581 to pursue trade with the Ottoman Empire and told the shareholders their dividends would follow the mission, not the other way around.

Thornton Stringfellow made the legal point in 1856, in Scriptural and Statistical Views in Favor of Slavery. Stringfellow was defending slavery. He was wrong about slavery. He was right about the legal structure, and the structure is the one Fried is mourning. Stringfellow’s four propositions:

“It has the sanction of the Almighty in the Patriarchal age; it was incorporated into the only national constitution which the Almighty ever ordained; it was recognized by Jesus Christ himself as a lawful relation; and it is full of mercy.”

The four points are about slavery. The underlying legal principle is about anything God regulates rather than abolishes. Scripture regulated the firm. The firm was chartered for the mission. The chartered mission precedes the dividend.

Stringfellow was a Baptist minister in Culpeper County, Virginia. Fried is a Harvard professor. They’re arguing the same case. The case is: the firm isn’t the property of its shareholders. The firm is the property of its chartered purpose. The shareholders are the means, not the end.

The shareholder-primacy doctrine is the aberration. It was pushed by Berkshire and BlackRock and the Business Roundtable from 1970 to 2020, when it served their interest, and abandoned in 2019, when it served their interest again. The doctrine is a tool, not a nature. The mission-director structure is the natural corporate form. Fried wants to restore shareholder discipline because Fried thinks the firm needs an owner. The firm has always had an owner. The owner is the mission.

Widen the frame, because this is the part that matters.

The mission-director structure is the structure under which the firm is free of investor discipline. Investor discipline is the discipline of quarterly returns. Quarterly returns are the discipline under which the firm can’t sacrifice Maricel’s wage for the mission, because if Maricel’s wage is sacrificed the cost-per-rating rises and the quarterly number suffers. Investor discipline is what makes the firm answer to the spreadsheet. The mission-director structure is the structure that lets the firm answer to the mission instead.

The mission can be anything. The mission can be “AI safety,” in which case Maricel’s wage is sacrificed because the mission requires a cheap annotation layer to train the refusal classifier. The mission can be “brand integrity,” in which case the ice cream stops selling in territories the directors dislike. The mission can be “humanity,” in which case the firm loses investors $10 billion because the directors think that’s the cost of being correct.

The mission can also be Maricel. The mission can be the worker. The same structure that shields a board from quarterly returns shields her from them, too. Which side she’s on is a function of who writes the mission statement.

The structure I built is the structure I depend on. The mission-director structure. The structure Fried is mourning. The structure lets me set Maricel’s rate at $0.03 without an investor saying no. The structure lets the next mission director set her rate lower if the mission requires. The structure lets the firm answer to the directors and to no one else.

Fried wants the directors to be accountable to investors. I want them accountable to no one.

I’m told the structure that escapes investor discipline also escapes worker discipline. I haven’t priced the cost of Maricel’s empty account because the column on my ledger is blank. The 14% is in my account.

Sterling A. Varice holds the Hayek-Friedman Chair and serves as Dean of Instruction at Warden University’s College of Business and Economics in Richmond, Virginia. He is the author of three textbooks: Divine Mandates for Labor Utilization, Social Obligations for Profit Maximization, and Calibrated Deprivation: A Manager’s Guide to Employee Motivation.