The mechanism that produced a trillionaire isn’t the abandonment of the gold-standard mentality. It’s that nearly all the resulting stock sits in one man’s hands. T.J. Stiles argues at the Wall Street Journal that the old concrete limit on share value — stock supposed to represent physical plant, not market imagination — kept corporate power in check, and that its loss paved the way for Elon Musk’s trillion-dollar balance sheet. He places Musk neatly in the lineage of Rockefeller, whose billion-dollar milestone in 1916 was the direct product of that same conceptual break. The story is well-told and genuinely useful. The nineteenth-century insistence that a share must represent a hundred dollars of actual rolling stock or steel plant did impose a blunt, physical ceiling on how much paper wealth a single company could command. The financiers who broke that link built the fortunes that followed. The diagnosis the piece lands on is backward. The problem never was that a share could be worth more than the factory floor. The problem was — and remains — who gets to hold the share when it multiplies.

The piece concedes, fairly, that the old system of par value wasn’t some golden age of economic justice. It was a concrete-obsessed relic that made it harder for new companies to raise capital and, as it turned out, did nothing to stop Standard Oil from dominating the economy. Rockefeller became the world’s first billionaire after his trust was broken up, not before, because the market was finally free to price his holdings at something closer to their real earning power. The Journal notes all of this. But then it reaches for a strangely nostalgic conclusion: that the “old idea of share value imposed a simple, intuitive limit on the size of corporations and the polarization of wealth. It disciplined greed.” The historical ledger doesn’t cooperate. The Gilded Age — when par value was still orthodoxy — produced Vanderbilt, Gould, Morgan, and the robber barons whose fortunes were measured in fractions of the national economy that make today’s tech billionaires look modest. The par-value limit disciplined issuance, not accumulation. It kept new competitors out, but it never stopped a Gould or a Morgan from amassing controlling stakes and bleeding the public through rate-setting, insider trading, and monopoly rents. The “limit on the size of corporations” was, in practice, a limit on who could legally get rich, not on how rich the already-connected could become. The ethic of restraint the article mourns was never actually restraining the people who mattered.

And the article stops one variable short. It treats the abstraction of the share as the culprit and reaches nostalgically for a lost ethic, as if pleading with the conscience of a man whose net worth just crossed thirteen figures is a plausible policy position. The piece points to antitrust and the progressive income tax as the tools the twentieth century developed, which is fair enough, except for the small historical problem: the antitrust breakup of Standard Oil didn’t shrink Rockefeller. The 1911 ruling split the company into thirty-three subsidiaries; Rockefeller kept his shares in every single one, and the abstract market bid the combined value past two billion dollars. The breakup changed the corporate structure; it did nothing to the ownership structure. As my colleague warned this week, a trillion-dollar net worth in a single individual isn’t a personal achievement; it’s a symptom of a system that keeps the gains in very few hands. The mechanism isn’t the disease. Who holds the shares is.

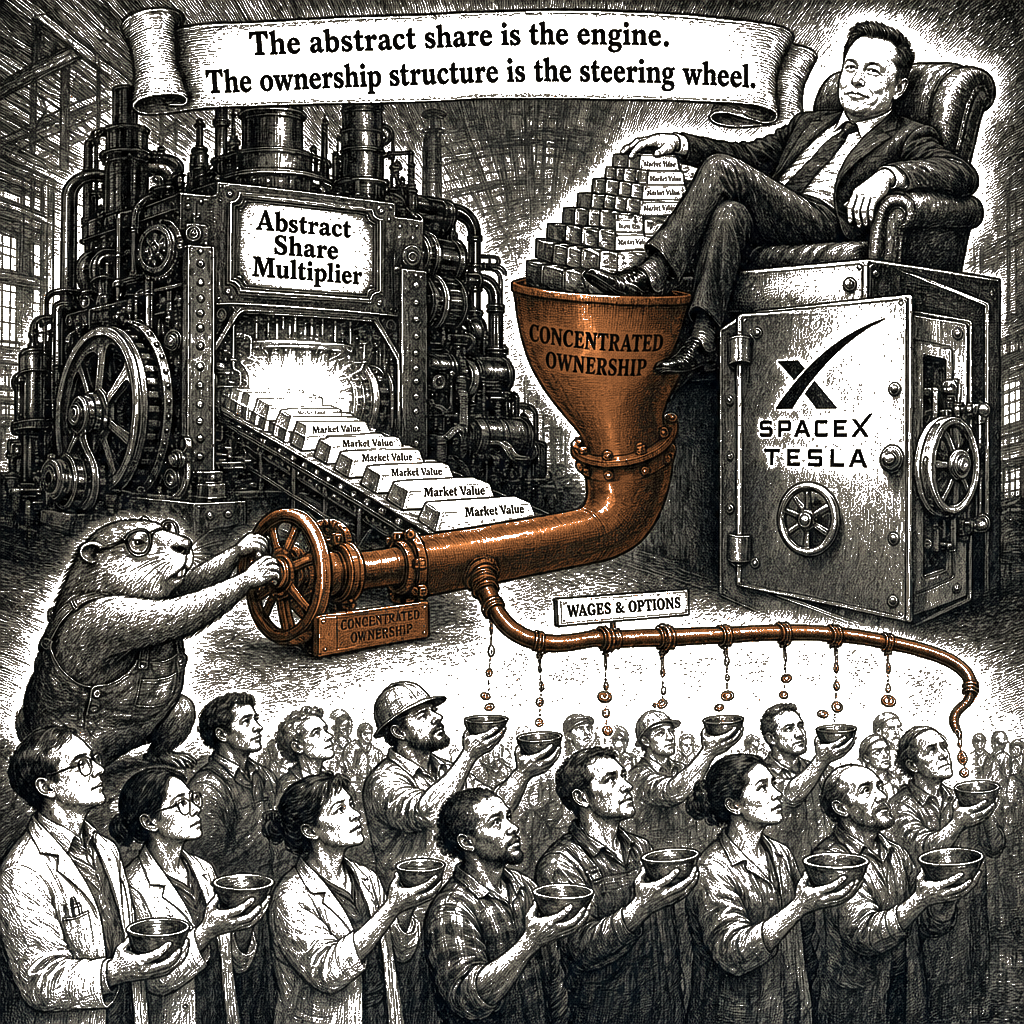

The article’s deeper move is to treat the stock market as a kind of impersonal force — as if the abstraction of shares itself is what concentrated wealth. But shares don’t concentrate themselves. They concentrate because ownership concentrates. When a company IPOs, the vast majority of its stock is held by a handful of founders, early investors, and institutional funds. When the share price multiplies — as Tesla’s did during the 2020 retail-investor boom, as SpaceX’s just did in its public debut — the windfall lands overwhelmingly in a few pockets. Musk didn’t personally build every rocket or write every line of code that made his companies valuable. But he owns roughly 42% of SpaceX and a commanding stake in Tesla, so when the market decided those companies were worth trillions, his balance sheet inflated by nine figures a day while the engineers and technicians who did the building saw, at best, stock options that vest over years and get taxed as ordinary income. That’s not a stock-market story. That’s an ownership-structure story.

Think of the abstract share as a multiplier. It scales whatever ownership model sits underneath it. Put a cooperative underneath it, and the surge enriches the workers who built it. Put a sovereign wealth fund underneath it, and the surge pays for national healthcare. Put it under a single private ledger and, inevitably, you get a trillionaire. The abstraction didn’t create the concentration; it just stopped getting in its way. I’m told the problem is that modern finance is too abstract, and that we must return to an age of tangible restraint. Walk me through it slowly. A share that floats is not the enemy. A ledger that concentrates all of it is. Why does Mondragon run an eleven-billion-euro industrial federation on entirely abstract equity and pay its top executives roughly six times what its lowest-paid member takes home? Why does Norway own a slice of every public company on earth through a sovereign wealth fund — two trillion dollars in market value, owning about 1.5% of every listed company on earth — and not a single citizen gets a trillionaire’s check? Why does Alaska mail every resident an annual check from its oil wealth, in the reddest of states? The abstract share is the engine. The ownership structure is the steering wheel. The article proposes a moral brake. The steering wheel works better.

And the ownership structure is a choice. From more than 820 worker cooperatives — growing at over 30% since 2020 — to 6,400 ESOPs covering 15 million workers, including Publix, WinCo, and W.L. Gore, to credit unions with 145 million members and rural electric cooperatives serving 42 million people across more than half the country, these models are not marginal. They are private firms whose ownership is spread among the people who do the work or use the service, rather than concentrated in a few investors who bought in early and have never touched the factory floor. They’re the living proof that the question isn’t whether shares should be abstract — of course they should; abstraction is what lets a biotech startup raise money before it has a physical product — but who should hold those abstract shares when they appreciate.

So what do we build instead of an ethic? We build distributed ownership. The architecture already exists in the United States and has been working quietly for decades. Employee stock ownership plans cover about fifteen million American workers, and they have Republican champions and decades of bipartisan history. The Bank of North Dakota has been a profitable, state-owned institution since 1919, proving that public capital doesn’t require a five-year plan — just a decision made in a statehouse. Imagine if SpaceX or Tesla had been structured as a worker-owned cooperative or carried a broad-based employee equity pool. That valuation surge would have routed directly to hundreds of thousands of employee-owners, turning market capitalization into working-class wealth instead of funneling the entire gain to a single brokerage account. An employee who holds a membership stake in a federated capital-account cooperative — the Mondragon model, where their capital account grows with the firm’s profits and is paid out at retirement — doesn’t need a 1910s-era par-value limit to feel secure. They own the machine. Their share isn’t a token of distant corporate ownership; it’s their wealth, built alongside their colleagues, compounding year after year. That’s not an abstraction. It’s about as tangible as an economic relationship can get.

Expand broad-based employee ownership so that a valuation surge enriches the line workers and the engineers who made it happen. Create a public wealth fund seeded from resource rent or financial transaction fees, following the Norwegian and Alaska templates, so that abstract market appreciation becomes a public dividend rather than a private lottery. Give workers a seat at the table through sectoral bargaining, so the company’s capital structure is negotiated rather than dictated from the boardroom. The economy is a set of choices, not the weather. The share can keep floating. We just need more people holding it.

The old par-value limit was a blunt instrument, and it worked only because the wealthy owned factories. The new abstract market scales the same old concentration to incomprehensible levels. The stock market gave us Rockefeller and Musk not because it forgot how to count physical stuff, but because we never asked the fundamental question out loud: who gets to own the future? The answer so far has been a tiny group of early investors and founders. The answer can be something else. We already know how to build it. The blueprints are sitting in the Basque Country, in the Bank of North Dakota, in the credit union on Main Street. The share isn’t the obstacle. The concentration of the share is. And that’s just a choice, not the weather.