The Erie Railway board fled to New Jersey with the company’s books in their arms in 1868, pursued by police for contempt. Jay Gould had flooded the market with millions of dollars of new stock that represented nothing — no rail, no rolling stock, no land — to break Cornelius Vanderbilt’s corner. When an injunction threatened prosecution, Gould went to Albany with a checkbook. The legislature, after three days of his hospitality, passed a bill making the fraudulent stock legal. The problem was not that a speculator won. The problem was what was ratified that day: the right of capital to invent claims on real wealth without creating any new real wealth in return.

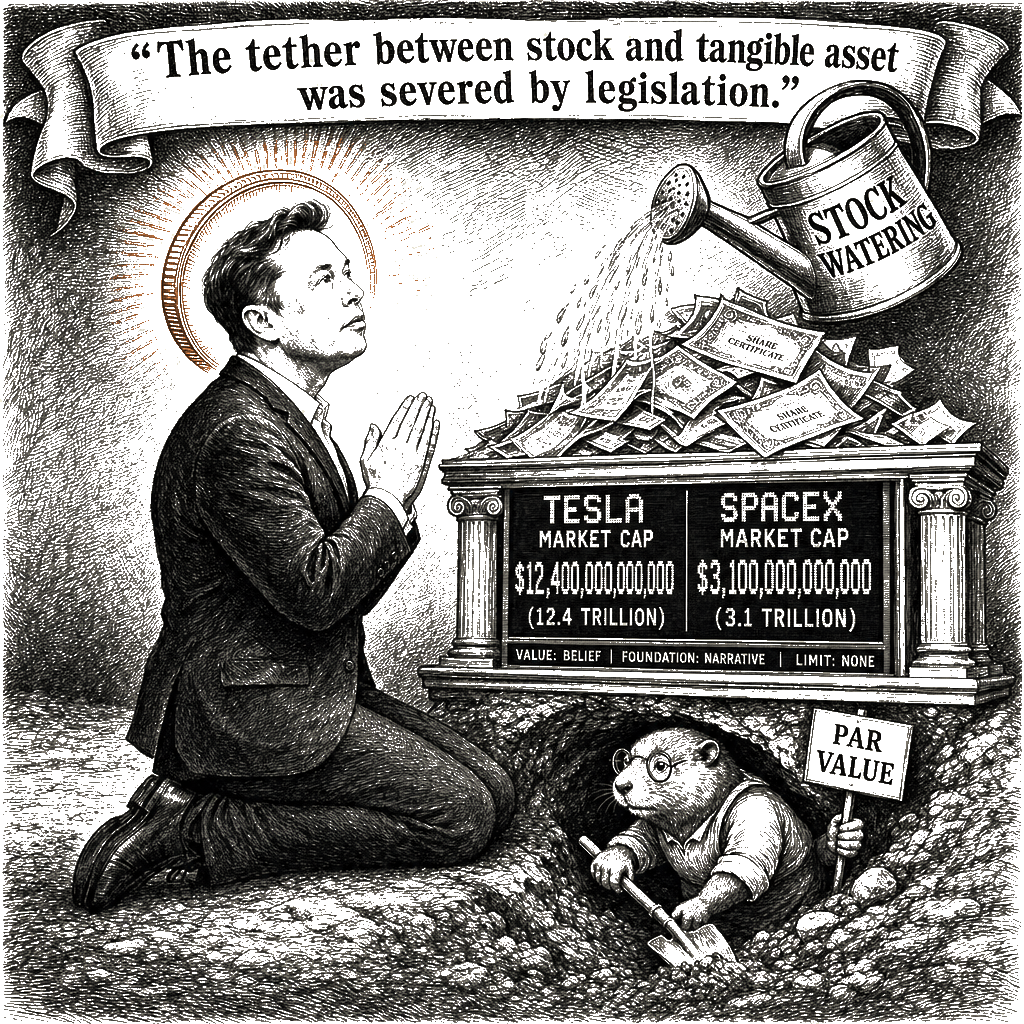

When John D. Rockefeller became the first billionaire on September 28, 1916, he did not cross that threshold because Standard Oil suddenly built a second universe of refineries. He crossed it because the legal tether between a share of stock and tangible value had been severed. The same mechanism now delivers the first trillionaire. The SpaceX IPO has pushed Elon Musk past a trillion dollars, and his fortune is the descendant of Gould’s scheme, perfected by J.P. Morgan and the architects of the holding company, encoded in a century of corporate law that deliberately decoupled a share’s value from any tangible thing. Musk’s trillion is not a marvel of innovation. It is the fulfillment of a project designed to concentrate wealth without limit, and he is its latest beneficiary.

To grasp the fraud, recover the original idea. Before the Gilded Age, a share of stock represented a specific dollar amount of land, plant, and equipment. The par value was a public promise — a piece of a productive asset that justified its own price. Investors looked to dividends, not speculation, for a return. A company could only issue as many shares as it had spent building real things. Stock issued beyond that was “watered” — a term from the cattle market where animals were force-fed water before weighing. To water stock was to swindle. That norm was not a quaint tradition of early banking. It was a structural discipline against infinite accumulation, the only obstacle that kept wealth tethered to material reality.

Lift the limit, and the paper value of an enterprise decouples from anything the enterprise actually does. The market’s task is no longer to price a productive asset; it is to project the faith of investors into the future, converting mere sentiment into capital gains. The old-scale limit on shares was the suppressed variable — the factor the financier class has spent a century and a half training us not to see. When New Jersey in 1889 authorized corporations to own other corporations, it was not the result of a popular referendum. It was a quiet act of a legislature, lobbied by industrialists, that fundamentally rewired the relationship between capital and the public. The Wall Street Journal of 1901 warned against this “overcapitalization,” recognizing that dividends paid on paper claims were dividends extracted from the actual productive asset. The warning was noted, and then it was bought.

State the true half first, because the opposition’s argument is not stupid. Some liberation from the physical tether was necessary to fund railroads and telegraphs and, later, software companies whose assets are code and networks. I will concede that. But the financier class flattened a crucial distinction in the century after Gould: the difference between value-creating abstraction and value-capturing abstraction. Abstraction that funds genuine research, builds networks, develops intellectual property — that produces real economic capacity, even if the assets are intangible. Abstraction that merely bets on market-cap growth and borrows against unsold stock — that produces nothing but paper, extracting real goods from the economy without contributing real productive capacity in return. Musk’s fortune is overwhelmingly the second kind. His wealth is concentrated, personal, and extractive. It is not the yield of a productive enterprise returning dividends to millions of shareholders; it is a giant wager capitalized at multiples that reflect speculative hope, not earnings. From that paper wealth he can borrow — the “buy, borrow, die” strategy — extracting real goods and services from the real economy without ever selling a share or paying capital gains. The cost diffuses downward onto workers whose wages are suppressed, onto the public that subsidizes his companies through government contracts and regulatory forbearance, onto the environment that absorbs his operations’ externalities. The mechanism is no different, in its concentration of benefit and diffusion of harm, from the trusts the original progressive movement had to shatter.

The public framing of this accumulation relies on a specific rhetorical move. Recent retrospection in the financial press calls the historical shift a “revolutionary way of thinking” and a “more abstract mindset” that “pushed past old limits.” This is frame-engineered relabeling — the deliberate substitution of a neutral or positive term for a structural reality, meant to shift the cognitive frame within which the issue is processed. To call it a mindset is to suggest it was an intellectual awakening rather than a calculated dismantling of the constraints on greed. The historian who wrote of an “ethic of restraint” and lamented that we “never replaced that lost limit on shares” is himself confessing. The ethic was not lost to time. It was legislated out of existence by the very actors who benefited from its absence. The financiers of the Gilded Age did not accidentally stumble beyond the par-value fence; they lobbied, bribed, and litigated until the fence was torn down. A century later, SpaceX exists not because it is a uniquely efficient enterprise but because it can float on a sea of abstract valuation that would have been unimaginable without that legal change. Musk’s fortune is a direct inheritance from Gould’s bribes and Morgan’s boardrooms. The republic gave away its sovereignty over the corporation piece by piece, and now we call the robber’s prize a wonder of the free market.

The immediate measures are brutal and obvious: tax unrealized gains on billionaires, cap the deductibility of interest on loans backed by unsold stock, disallow performance-based compensation tied to market capitalization, mandate that companies issuing new shares demonstrate actual investment in tangible productive capacity. To these add the tool the first progressive movement bequeathed us and we have allowed to atrophy: the progressive income tax, restored to its original function not as a revenue device but as a brake on accumulation, a structural check on the concentration that unlimited share valuation enables. These measures are not merely fiscal adjustments; they are structural reinforcements. Without them, liberty dies not with a single coup, but with a hundred legislative sessions, each legalizing a little more extraction, each stripping away a little more public accountability, until the edifice is so large that it seems natural and inevitable.

When King argued for a “radical revolution of values,” he was speaking to the very abstraction that the financial apparatus uses to launder extraction. His structural critique of materialism was not a plea for better margins. It was a demand to recognize that an edifice which prioritizes the abstract accumulation of wealth over the tangible needs of the human community is morally bankrupt. You cannot fling a coin to the communities left behind by the trillion-dollar extraction and call it justice, because the coin itself is minted from the devaluation of their labor. The edifice that produces billionaires requires restructuring. The restructuring begins by restoring the tether between stock and tangible asset, by refusing to allow market capitalization to operate as a vehicle for legalized stock watering.

A new ethic will not descend from the heavens. It must be encoded in law. The longer arc requires a reconstruction that King would recognize: a revolution of values in which the corporation is no longer an engine for the private multiplication of paper but a public instrument, chartered to serve the common good, and permitted to exist only so long as it does. The stock market is not an oracle of merit. It is a printing press for oligarchs. The arc bends when we shut it down.