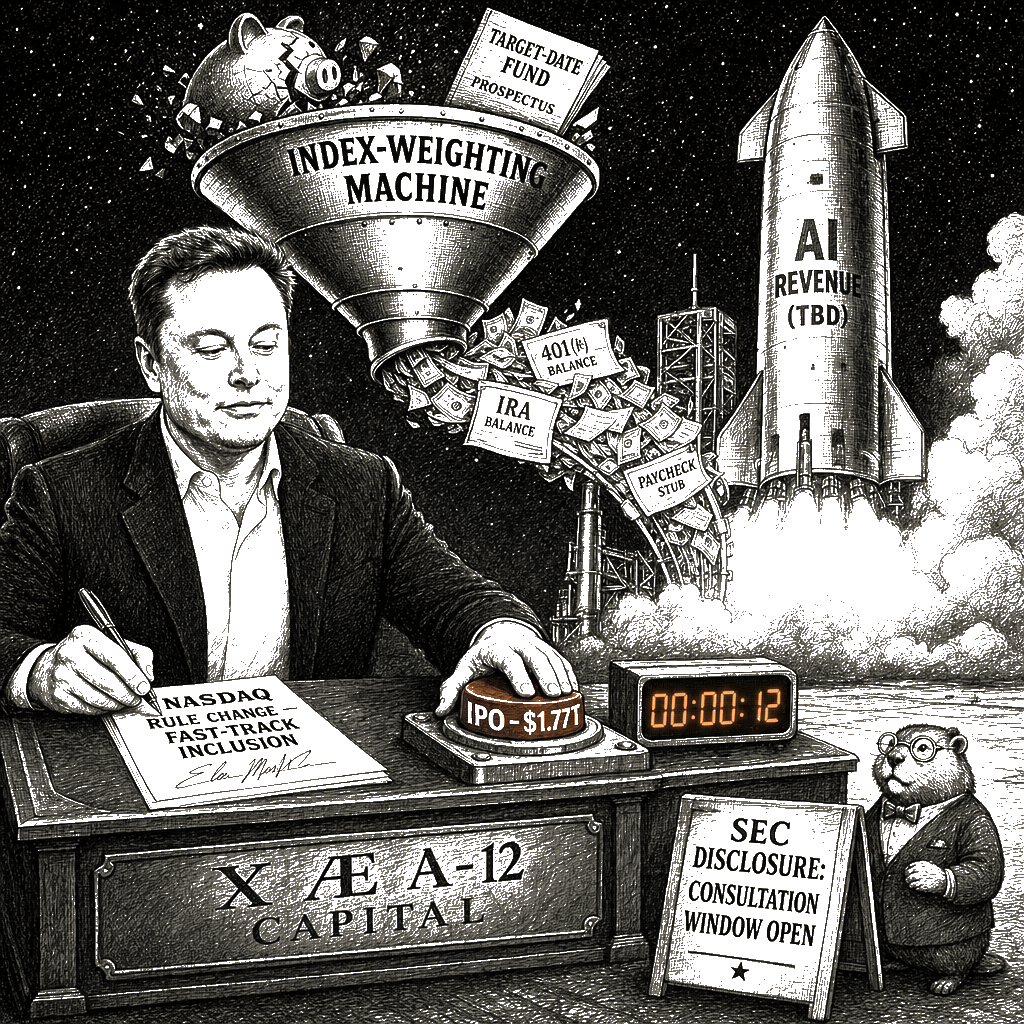

Musk captures Americans’ retirement savings to bankroll an AI extraction gamble. The mechanism is mechanical, not moral, which is what makes it durable. The Nasdaq changed its listing rules this spring to fast-track megacaps into its index. FTSE Russell did the same. Standard & Poor’s is holding to its existing discipline—a company must be profitable, a minimum float must trade publicly, and roughly twelve months of trading history must precede inclusion—but that discipline only delays the capture. When three-quarters of retail retirement capital sits in index funds and target-date vehicles that track those indices, the managers do not exercise discretion about whether the company justifies the risk. They buy it in proportion to its weighting. A $1.77-trillion initial public offering that surpasses a $2-trillion market cap on debut becomes, under the mechanical weighting rules that govern passive vehicles, a forced purchase order for every American who set aside a portion of their paycheck and assumed they were holding anything close to a diversified basket.

The pitch is that artificial intelligence will hypercharge productivity and propel human prosperity to unprecedented levels. The documentary record says something different. SpaceX has not yet posted a consolidated profit. Anthropic and OpenAI are pushing toward blockbuster IPOs of their own to join the same index basket, burning billions in cash each quarter on compute infrastructure whose revenue models have not yet matched the expenditure. The engineering reality of current large-language models is that inference costs scale superlinearly with capability gains, the alignment problem remains unsolved, and the productivity bump documented in the national accounts is, to date, statistically indistinguishable from zero. What is moving is not the productivity statistic. It is the index weighting. This is the architecture of the bezzle that Galbraith coined and Doctorow mapped for this cycle: the gravity-defying interval between the capital raise and the moment the market realizes the projected revenues are accounting fiction rather than operating reality. The AI buildout is a bezzle of world-historical proportions—hundreds of billions of dollars of capital expenditure, much of it financed through the equity markets, predicated on a revenue stream that remains stubbornly hypothetical.

I will concede the strongest version of the opposing argument, which is that capital markets are supposed to price risk and that the index-fund buyer always assumed exposure to the largest companies in the market. The trouble is that the largest companies in the market are no longer a diversified basket of consumer-facing, manufacturing, and financial concerns. They are a vertically-integrated stack of compute providers, cloud landlords, and inference monopolies whose business model is to extract tolls from every downstream developer and creative worker who passes through their API gateway. By this time next year, a company that makes most of its money selling internet access and needs the IPO cash to finance data-centers-in-orbit dreams will command something like one-and-a-half percent of the most-tracked equity index on earth, forcing index funds to buy tens of billions of dollars of stock irrespective of price. The so-called Magnificent Seven already account for more than a third of the S&P 500’s market value. Stack SpaceX, Anthropic, and OpenAI on top, and the American retirement system becomes, in economic fact, a concentrated venture-capital portfolio of unprofitable AI companies, managed not by fiduciaries with a duty to diversify but by the mathematical compulsion of index-weighting.

The playbook here is older than the Nasdaq rulebook. It is the same playbook that leveraged-buyout operators applied to Canadian heavy industry between roughly 1985 and 2005—extract the existing surplus, load the entity with financial obligations, and leave the workforce and the community holding the residual risk. The mechanism is new—index-weighting rules, “passive” fund structures, the cloud-layer computational apparatus that makes continuous twiddling possible—but the architecture of extraction is identical. The retirement savings of American workers are being converted, without their affirmative consent and largely without their understanding, into the equity cushion for a small number of technology executives’ speculative projects, at valuations no discounted-cash-flow model can justify.

Superficially, there is a tidy story in which this all works out: the AI agents arrive, productivity skyrockets, the equity holdings appreciate, and the displaced worker holding the index fund gets a slice of the new prosperity. The story has the shape of an investment-banker pitch deck. It also requires accepting that the claimed capabilities of the current generation of large language models—capabilities that, even on their proponents’ most generous accounts, have not yet produced measurable economy-wide productivity gains—will not only materialize at scale but will do so before the bond covenants come due on the trillion-dollar data-center buildout. The gap between “the models produce impressive demos” and “they will replace knowledge work at scale before the cost of capital resets” is the same gap that separates a functioning retirement system from the bezzle. The math is insulting: a worker facing a 60 percent income collapse would need an equity position equivalent to ten years of their previous salary just to maintain their consumption floor. Index funds do not grant you that. They grant you fractional exposure to the companies that automated you out.

The structural remedy here is not complicated, though it is politically neutered by design. The same firms poised to dominate the indices are among the largest political contributors in Washington, and the House subcommittees and SEC divisions tasked with overseeing market structure are staffed by their alumni and funded by their PACs. Antitrust enforcers should treat the simultaneous listing of three foundation-model providers as a coordinated concentration event rather than as three independent commercial offerings. The SEC should require index-fund prospectuses to disaggregate AI-infrastructure exposure as a distinct risk category so that retail buyers—or at least their plan fiduciaries—can see what they are actually holding. If an index is forced to hold a stock, the investor forced to hold that index deserves to know exactly what the underlying company actually does with their capital.

The question is not whether the bezzle exists. The question is who is left holding the bag when it is discovered. The Nasdaq’s recent four-percent drop, shaken by a robust labor market that may force the Fed to raise rates, offers a preview of how quickly the AI trade can sour. Americans have vivid experience of the pain that courses through society when a financial bubble built on hubris collapses. The great financial crisis of 2008 will look like a cartoon compared with what will befall the finances of most Americans if the AI dream tucked into their investments turns into a nightmare. There is a consultation window open at the Securities and Exchange Commission on disclosure rules for passive vehicles and special-purpose financial products. The filing period is the only part of the securities architecture that ordinary people can touch from the outside. The work is to be done.