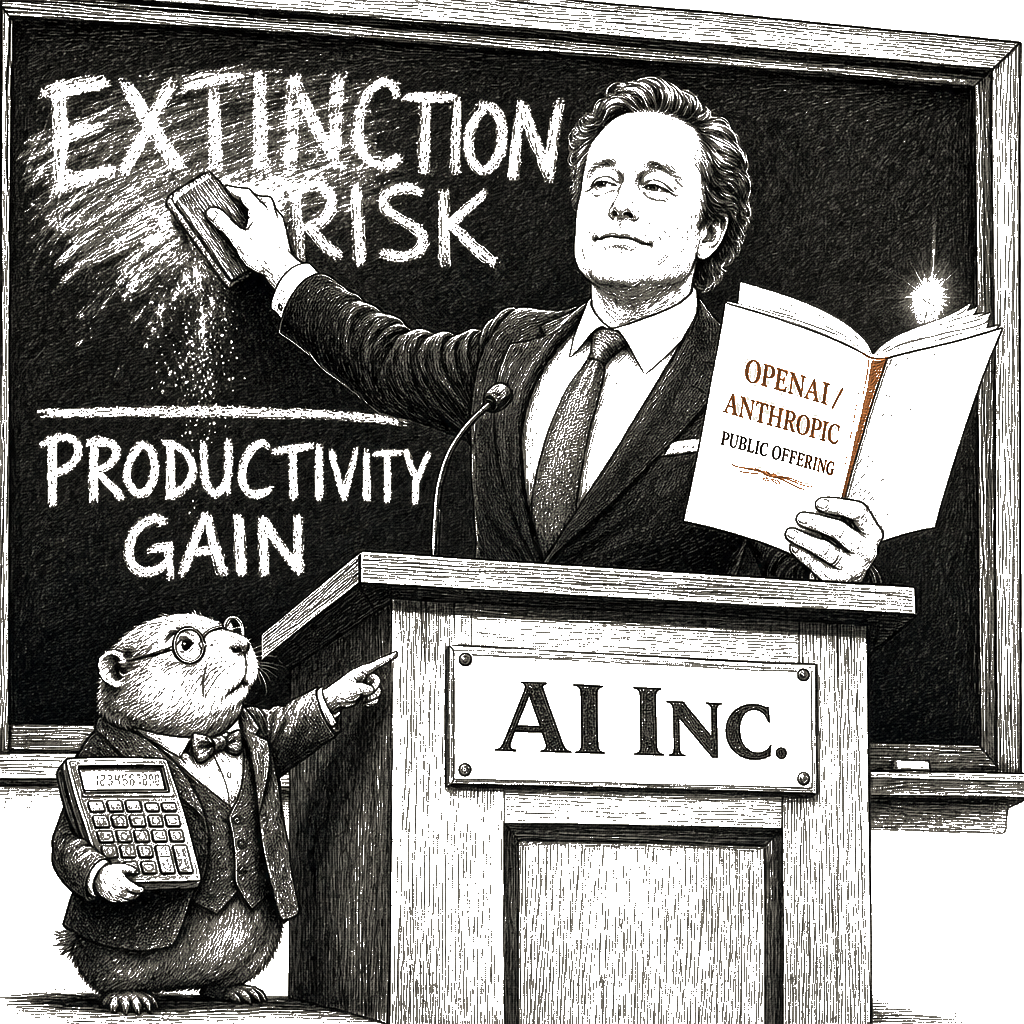

Sam Altman and Dario Amodei are walking back their own AI doomsday predictions just as they prepare to cash out.

That is the fact the Wall Street Journal noted, parenthetically, in an article about an AI scenario-planning exercise held this week at the Peterson Institute for International Economics — without, apparently, feeling the need to interrogate it further. The sentence that did the work reads: “OpenAI’s Sam Altman and Anthropic’s Dario Amodei have softened earlier predictions of a white-collar job apocalypse, albeit ahead of recently announced plans for initial public offerings.” The word “albeit” is carrying an enormous weight. It implies a small, awkward truth the article permits itself to note before moving on. The awkward truth is the entire story.

It is worth being precise about the sequence. In the spring of 2023, Altman and Amodei were among the signatories of the Center for AI Safety’s one-sentence public statement: “Mitigating the risk of extinction from AI should be a global priority alongside other societal-scale risks such as pandemics and nuclear war.” Altman told a Senate committee that AI could “cause significant harm to the world” and that something “in between” the printing press and the nuclear bomb was the right analogy. Amodei’s Anthropic was built on the premise that AI systems would become powerful enough to constitute existential threats and that only Anthropic’s careful approach could steward the transition safely. Altman, separately, told the press he was open to a moratorium on frontier AI development — the “international airstrikes on rogue data centers” register, the register that gets a company noticed and funded and exempted from the ordinary expectations of accountability.

By 2026, the rhetoric had softened into something the industry calls a “mature” assessment. The same systems were now positioned as productivity tools. The catastrophic framing was not retracted so much as retired — quietly, with no press conference, no accounting of what changed in the technical understanding to warrant the shift. And both OpenAI and Anthropic were pursuing initial public offerings. OpenAI had restructured from a nonprofit into a public-benefit corporation. Anthropic had largely agreed with the economists who think AI will boost productivity, with the expected caveat about job reallocation. The predictions were not revised because the technology changed. The technology did not change. The capital-markets situation changed. The same models that were going to end the world in 2023 are now going to boost GDP and require sensible policy responses in 2026. The models did not become safer. The companies became ready to sell shares.

The scenario workshop at the Peterson Institute, run by the nonprofit Windfall Trust, was called “Paper Prosperity.” Forty experts in economics, technology, and public policy were given workbooks, easel pads, and Sharpies and asked to game out a vision of U.S. society in 2030. By its metrics, AI had nearly doubled the rate of GDP growth and labor productivity. The S&P 500 was soaring. Underneath: underemployment had leapt from 8 percent to 14 percent, indicating that millions more Americans were in part-time work, gig roles, or positions below their qualifications because AI had triggered layoffs of college-educated workers. “Underemployment, gig work and precarity — long features of working-class American life — were finally reaching the upper tiers of the middle class,” the scenario read. The experts agreed that political unrest would rise, generational divides would widen, and fertility would decline. The social contract — go to school, work hard, prosper — would fray.

They also agreed, after a day of collegial Sharpie-on-easel-pad diagramming, that the policy responses should include worker reskilling, a universal basic income, taxes on AI companies and their shareholders, universal health insurance, job guarantees, wage subsidies, and investment in child care and eldercare. A sovereign-wealth fund — the kind Senator Sanders proposed this month, which would hold half of the industry’s equity for the public — was broached as well.

That the experts, in a setting designed to generate policy, converged on the policies any reasonable observer would name is not surprising. What is surprising is that no one in the room, according to the Journal’s reporting, paused on the fact that the two men whose companies would be the primary objects of those policies were already adjusting their public statements to make the road to their own IPOs less treacherous. The causal reading that follows is mine. But when the men whose apocalyptic forecasts might frighten off institutional investors start softening those forecasts just as the roadshow begins, the pattern is hard to dismiss as coincidence. It tells you that the men building the largest concentration of machine-learning capital in human history, who until recently warned that their creations could displace vast swaths of educated labor, are now revising those warnings downward as they prepare to sell shares to the public.

You do not need to be a cynic to see what is going on. You only need to know what J.K. Galbraith called the bezzle: the magic interval between the commission of a fraud and its discovery, when the embezzler has the money and the victim has not yet felt the loss. In Galbraith’s original formulation, the bezzle is the gap between the wealth that has been extracted and the moment the extraction is felt. Here, it is the gap between the capital gains now flowing to AI shareholders and the lost wages that will show up in household accounts next year. We are, by the available indicators, in the bezzle of the AI boom — FOMO alone is propelling Wall Street money into an asset class with revenue projections that are, by any historical base-rate comparison, extreme. GDP rises because capital expenditure on data centers counts as economic activity. Stock prices rise because investors fear missing the next big thing. Productivity statistics get a one-time bump from producing the same output with fewer people. Real growth, but growth whose proceeds flow upward, not outward. None of this, necessarily, improves the material condition of the people whose work was eliminated. It just concentrates the gain elsewhere. That is the scenario the Peterson exercise described. That is the scenario Altman and Amodei are now busy reassuring us isn’t going to happen, while they personally prepare to turn their equity into something more liquid.

When I say this is not simple cynicism, I mean that the pattern is structural. It is exactly the second stage of the pattern Cory Doctorow calls enshittification: first, the platform is good to users; then it is good to business customers; then it claws value back from both for shareholders. Google started as a search engine you could trust, then became an advertising-surveillance operation that pays Apple twenty billion dollars a year to maintain its default position. Facebook started as a way to keep in touch, then throttled the feed to sell you back access to your own friends. The AI industry’s “Paper Prosperity” scenario — GDP doubling, S&P soaring, underemployment leaping — is the economic form of the same third stage. The productivity is real. The underemployment is real. The question is who captures the one, and who bears the other. The scenario, as the experts worked through it, does not ask that question. It asks what policies might redistribute “the windfall that AI will create.” The windfall is presented as an aggregate — a sum to be divided, a surplus to be managed. But if labor productivity doubles and underemployment rises, the value of what workers produce is increasing while the share of that value workers receive is decreasing. The difference is going to the shareholders of the companies that own the models, the compute, the training data, and the distribution channels — the same companies whose executives, by the Journal’s own reporting, softened their catastrophic predictions at precisely the moment those predictions would have complicated their IPO filings.

This is not a policy problem. It is a structural-extraction problem dressed in a policy-problem costume. The mechanism is not automation but the credible promise of automation, deployed against workers who have nowhere else to go. An AI cannot do most jobs. The threat is that an AI salesman can convince your boss to fire you and replace you with a system that cannot do your job, and that the threat itself is sufficient to destroy bargaining power. The four forces Doctorow identifies — competition, regulation, interoperability, and labor — are the specific frictions that, when present, prevent the enshittification lever from moving freely. When the 262,735 tech workers laid off in 2023, according to the layoffs tracker Layoffs.fyi, lost their jobs, they lost the only friction that was operating inside the firms making the decisions about how much of the workforce to replace with models. The AI companies are building the twiddling machines, and they will own them. The softening of the job-apocalypse prediction is not, from what the pattern shows us, a correction based on new evidence. It is what you say when the people whose money you want to take start asking about the thing you told them would happen. The thing you told them would happen is now “less certain.” The IPOs, by contrast, appear quite certain.

What the experts at the Peterson Institute were doing — collegially, with their easel pads and Sharpies — was refining the management narrative for this transition. The scenario is not a prediction. It is a screenplay. It establishes the premise: AI will create enormous value and also enormous disruption. It introduces the cast: experts, policymakers, the concerned public. It proposes the resolution: reskilling, redistribution, safety nets. And it omits the question that makes the entire drama legible: who wrote the screenplay, who funded the production, and who owns the theater. Worker reskilling came up repeatedly, which is the policy equivalent of a recurring decimal — it has appeared in every major displacement event since NAFTA, and it has not worked in any of them, because reskilling presumes that the new jobs exist, that the new jobs pay comparably, and that the workers in question are not fifty-three years old with a mortgage and a skill set that does not survive translation. The other proposals are more interesting because they name the distribution question without answering the structural one. A sovereign-wealth fund is an ownership intervention: it attacks the capture mechanism directly by giving the public a share of the equity. It is also, in this political environment, a fantasy.

There is a straightforward alternative, one that does not require creating a new government holding company or rewriting corporate law to confiscate equity. A windfall tax on AI-driven profits, rebated directly to displaced workers, not filtered through a reskilling bureaucracy with a proven record of failure. Employers who replace human labor with machine labor must compensate the human labor they displace. That principle — you break it, you buy it — is already embedded in trade-adjustment assistance and Workers’ Compensation. It extends the logic to the new machine-driven displacement. The same political dysfunction that makes a sovereign-wealth fund impossible applies to a windfall tax, and the AI industry will fight it with the same ferocity. But a compensatory tax has one quiet advantage: it does not require inventing a new branch of government. It requires the political will to impose a cost on the people who are now telling us that the costs are imaginary. The people who are softening their predictions because they want your investment capital, not your regulatory attention.

The bezzle eventually ends. The victim realizes the loss. In the Peterson scenario, the victim is the college-educated middle class, waking up to find that the prosperity the GDP numbers promised has not arrived in their paychecks or their job security. The social contract frayed. Fertility declined. The crochet economy, as one facilitator joked, was not quite the utopia it sounded like. The experts Sharpied their best ideas onto easel pads, and the easel pads, like the GDP numbers, looked like progress. They were not. The bezzle, too, always looks like prosperity — until the morning after. The IPOs are still on. The apocalypse, it turns out, was postponed until after the lockup period expires.