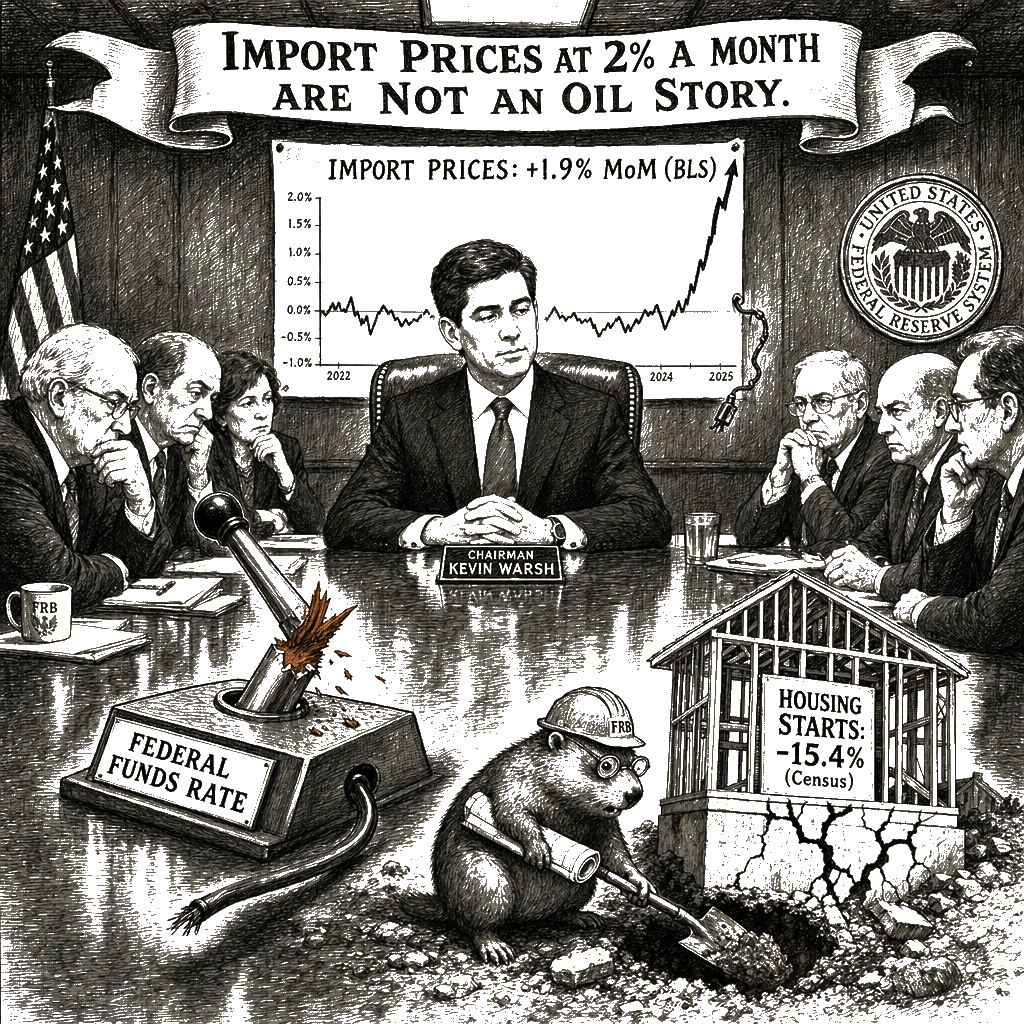

The bond market is pricing the peace deal as a broad disinflationary shock, burying the tariff-driven import-price signal the Bureau of Labor Statistics published this morning. Import prices rose 1.9 percent in May. April was revised to 2.0 percent. The Wall Street Journal consensus was 1.1 percent. These are Bureau of Labor Statistics numbers. The monthly rate, annualized, exceeds 20 percent.

Housing starts fell 15.4 percent in May against a consensus forecast of negative 2.4 percent. These are Census Bureau numbers. The housing market is not cooling gently. It is contracting under a federal-funds rate — the rate banks charge each other for overnight loans — already at the level the prior tightening cycle established. Building permits contracted 0.7 percent. The direction is the story.

The Federal Reserve meets today under Chairman Kevin Warsh. No rate move is expected. The question the data presents is structural: demand-side inflation that rate hikes can reach is cooling, while import-price inflation that rate hikes cannot is running hot. The Fed’s instrument affects domestic demand. It does not affect the price of imported goods arriving at a U.S. port. Tariffs are paid at the border, not in the federal funds market, and the import-price data show them arriving wave after wave. Tightening into a supply-side shock the rate cannot reach has already produced the housing contraction visible in the Census numbers. The structural disconnect is clear: import-price inflation driven by tariff policy requires tariff policy to address, not further tightening that deepens the housing damage without touching the number the Bureau of Labor Statistics published this morning.

Meanwhile, a global yield reset is unfolding that will define the curve for a generation. In Tokyo, the Bank of Japan voted 7-1 to raise rates — a declaration that the reflationist minority has lost and the normalization camp now commands a supermajority. State Street Investment Management’s Masahiko Loo described “strong momentum behind normalization,” opening the calendar window for another hike by autumn. The 10-year JGB yield rose 5 basis points to 2.625 percent. The era of free offshore financing from Tokyo is over.

That higher floor means the Fed’s rate already sits on a tighter base, amplifying the damage from further hikes that cannot touch the import-price problem. ING’s rates team notes that U.S. real yields — Treasury yields minus expected inflation — are “structurally higher by some 40 basis points since before the war” and that they “doubt they collapse lower.” The Iran peace deal may ease oil prices and offer a sliver of breathing room, but it does not change the tariff code. Import prices at 2 percent a month are not an oil story. They are a trade-policy story. The Fed can hold. It cannot fix a number that originates in the tariff code. The Great Rate Reset is writing a new curve, and investors who mistake it for a quiet summer day will end up on the wrong side of it. The score is the score.