Trump ignited an oil-driven inflation and then installed a Federal Reserve chairman to suppress rates. The memorandum of understanding signed at Versailles this week carries a crude-oil price attached: Brent back below $80 a barrel, the lowest since the early weeks of the conflict the agreement is meant to end. The president’s reading is that the market has validated him. What the market has priced is a bet on the best case — and the best case is not the odds-on favorite.

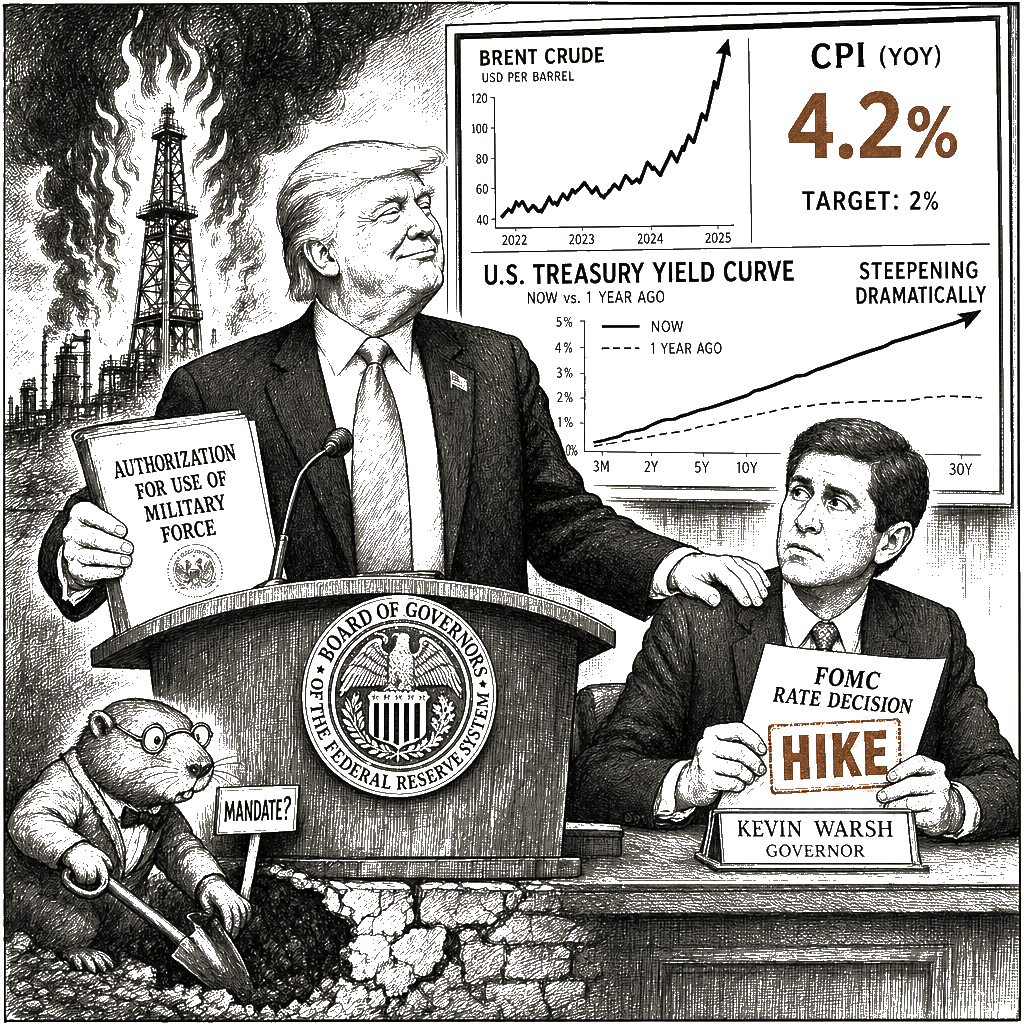

Inflation hit 4.2 percent in May, the highest in three years, propelled by the spike in petrol prices and the broader oil-supply disruption caused by the president’s bombing campaign against Iran and the blockade of the Strait of Hormuz. Trump’s response, when the number arrived, was to declare: “I love the inflation.” Drivers are paying a dollar more per gallon than a year ago. The European Central Bank has raised rates for the first time since 2023. Oxford Economics projects Gulf economies contracting 2.6 percent this year. Developing countries forced into fuel rationing have cut demand — hospitals run on generators and food spoils in transit, costs that do not appear in the official statistics — and that demand destruction may be part of why prices have not surged higher still.

The rate trajectory is where the war’s cost compounds into the federal budget. Kevin Warsh, the newly appointed chair, was chosen in the hope that he would deliver a string of rate cuts. Instead, private-sector economists now expect the Federal Open Market Committee to raise the federal funds rate as much as four times by the end of next year, pushing the target range to 4.5 to 5.0 percent. Dario Perkins of TS Lombard projects this would be the most aggressive tightening of any major central bank in this cycle. Every increase in Treasury yields flows through to the government’s interest expense: at $35 trillion in public debt, each percentage point of yield adds roughly $350 billion a year in interest. The deficit grows not from new spending but from the inflation the war produced and the borrowing costs that follow.

The contradiction is not subtle. The president who triggered an oil supply shock by force now seeks a central bank willing to look past the inflationary consequences. The Federal Reserve’s statutory mandate — stable prices and maximum employment — does not include a carve-out for wars the president started. The inflation number is a public document; the Fed’s legal obligation to contain it is not a matter of political convenience.

The oil market is not validating the deal. Capital Economics’ model puts Brent at $90 a barrel for the third quarter. The market has already moved to $80 — a Q3 discount applied before the third quarter has begun. Neil Shearing, the firm’s chief global economist, calls this a “Goldilocks outcome” that prices in the deal holding, the strait reopening fully, and no further disruptions. That is a bet, not a score.

The bet has problems. Shearing calls the deal fragile: Israeli operations in Lebanon, Iran’s leverage over the strait, and unresolved nuclear questions each present a path to collapse. BCA Research assigns a 60 percent probability to renewed fighting after the November midterms, once the political incentive to maintain the truce expires. Matt Gertken writes that the memorandum “should not be seen as a complete and durable peace deal.” Ryan Sweet at Oxford Economics warns the conflict’s “long shadow” may be permanent — firms that witnessed Iran’s demonstrated capacity to choke Gulf oil will build more slack into supply chains indefinitely, raising the floor under commodity prices. The economic timeline does not equal the military timeline. The Fed will have to act on the data, not on the president’s press releases.

The president urged skeptics this week to take Wall Street’s word. “There is nothing as smart as the market — and the market loves it.” He defended the same line when the first criticisms surfaced. The operation is a week of commodity-price relief presented as fiscal and strategic validation of a war that produced 4.2 percent inflation, a forced tightening cycle, and recession across the Gulf. The arithmetic is relentless. If inflation remains elevated above the Fed’s target, the dual mandate requires a tighter policy stance, regardless of who sits in the chair’s seat. Warsh may have been picked for his loyalty, but the bond market and the consumer price index will impose their own discipline. The question is not whether the Fed will have to raise rates. It is whether the institution’s credibility will survive the attempt to subordinate it to the White House’s political calendar.

The score is not the president’s to give.