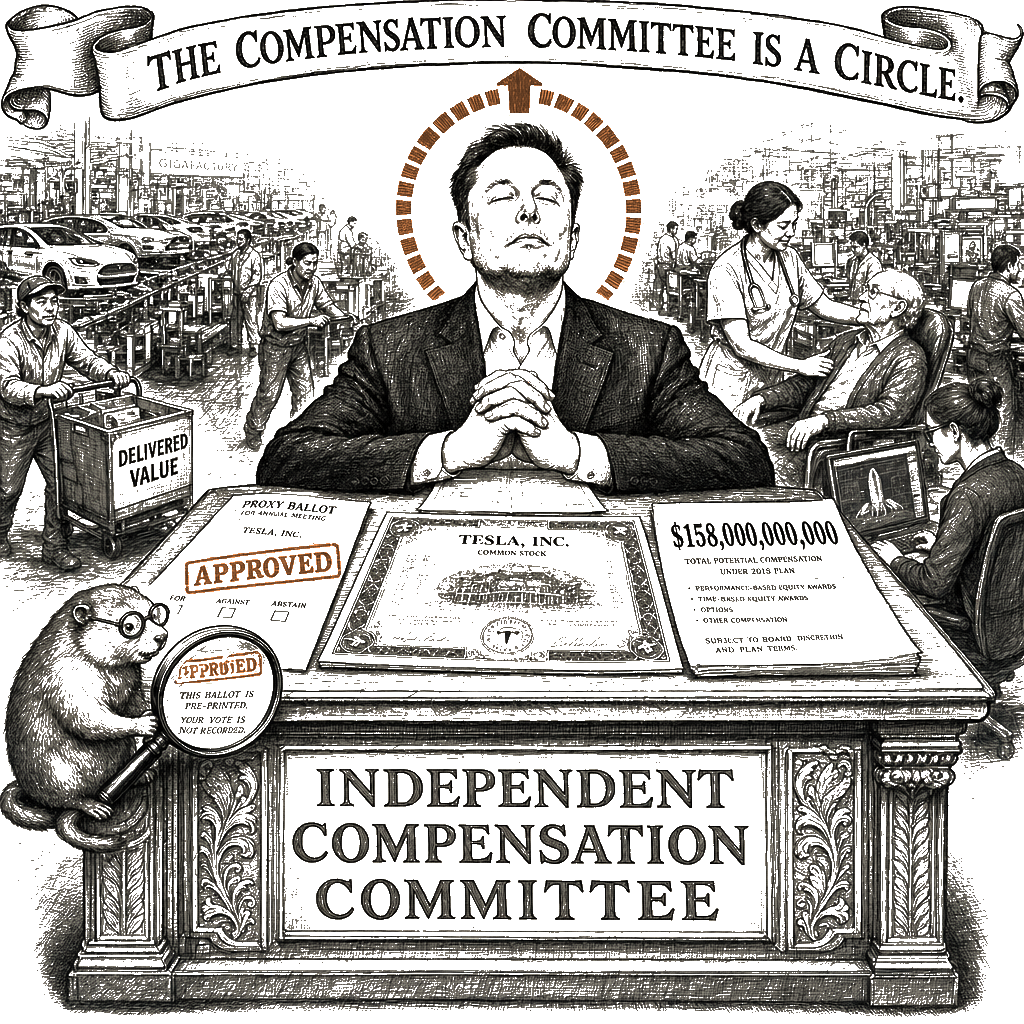

It is true that Tesla’s board approved the package, and that shareholders voted for it. It is true that, in the narrow sense in which corporate governance lawyers usually mean, Musk “earned” his equity by hitting performance targets. The trouble is that those targets were set by a board chaired by Elon Musk himself, with longtime allies like Antonio Gracias among its members, and the “performance” they required was a stock price that Musk himself can influence with a single tweet.

The Wall Street Journal’s annual CEO pay ranking arrived this week with a number that is, by now, almost numbing: Elon Musk’s compensation from Tesla is valued at $158 billion. If the company’s stock reaches a certain threshold, the package could be worth $1 trillion. As MSI has previously reported, Musk’s trillionaire status highlights American inequality with a cold stare. The same ranking found that median CEO pay at S&P 500 companies rose to nearly $18 million, with half receiving raises of 9.8% or more—roughly 200 times the typical worker’s wage. Just over half the CEOs cresting $100 million ran companies outside the S&P 500, including Figma’s Dylan Field at $864 million and Opendoor’s Kaz Nejatian at $741 million. To put Musk’s number in perspective, it is sixteen times the combined pay of all 391 other CEOs in the ranking.

The second-highest-paid CEO, Welltower’s Shankh Mitra, pulled in $821 million—mostly through an October stock grant. Welltower is a real-estate investment trust that operates senior housing and healthcare facilities, the kind of places where families pay substantial monthly rents for their parents and grandparents to be looked after. Three other Welltower executives each received packages valued at over $100 million, making it only the second company in a decade to have four executives in the nine-figure club. The company said the awards replace bonuses and equity for a decade and are designed to align their incentives with shareholders. It is worth remembering, when those words are spoken, that the shareholders of a REIT that profits from elderly housing include the same institutional investors who hold Tesla, Microsoft, and every other company whose CEO is now pulling down a quarter-billion dollars a year.

The alignment claim—that the architecture is built for the shareholder—does not survive contact with the data. Robinhood Markets, the trading platform, delivered the best shareholder return in the ranking: 204%. The company reported paying CEO Vladimir Tenev $3 million for the year. But Tenev was able to cash in on a 2019 pay package bringing him stock valued at $1.1 billion, securities filings show—meaning the best-performing CEO was paid the least, on paper, while drawing the most in actual value from an earlier architecture choice. At the other end, David Zaslav collected $165 million from Warner Bros. Discovery and Hock Tan received $205 million from Broadcom—both from top-performing companies this year, but also the same two executives who have collected nine-figure packages across years of varying results, because the architecture produces the number regardless of the outcome it claims to measure. If the architecture were really designed to reward performance, pay and shareholder return would track together. They do not. They scatter.

The mechanism by which all this value is transferred from the enterprise to the executive is not mysterious. Most big companies pay their CEOs primarily in stock options or restricted stock. The awards are dressed up as “performance-based,” but the performance metrics are chosen by compensation committees that are themselves populated by current and former CEOs—a closed loop, a chokepoint of the kind that Cory Doctorow and Rebecca Giblin have described in other industries. In the case of Musk’s 2018 package, the board set targets for Tesla’s market capitalization that, at the time, seemed ambitious. But the board was chaired by Elon Musk himself, with longtime allies like Antonio Gracias among its members, and the package was approved by a shareholder vote that Tesla itself lobbied for. Once the stock began to rise—propelled in part by a frothy market for electric vehicle companies and in part by the cult of personality around Musk—the value of the award soared. The past year’s AI mania has added another jet of fuel: Broadcom’s Hock Tan received $205 million this year, and the company said he would receive no more equity through 2030 unless he meets targets for artificial-intelligence revenue.

This is the same playbook that has been running since the Reagan era, when the Securities and Exchange Commission adopted Rule 10b-18 in 1982, giving companies a safe harbor for stock buybacks and fueling the equity-heavy pay model that now dominates. It is the same playbook that hollowed out my father’s rolling mill in Selkirk, Manitoba—a mill that was bought by a Brazilian conglomerate in the mid-1990s, which promptly cut wages, sped up the line, and eventually closed the plant. The language was different then: they called it “restructuring” and “maximizing shareholder value.” Today we call it a “moonshot pay package,” but the extraction is the same. The workers who built the cars, the nurses who staff the senior homes, the engineers who wrote the code—they are the ones who lose.

The remedies are not exotic. A tax code that treats capital gains more favorably than wages does part of the work; a securities regime that requires shareholder approval of executive pay but then allows companies to fill the proxy ballot with endorsements does another. But the root cause is simpler: workers in the United States have almost no bargaining power at the corporate level. Sector-level collective bargaining, of the kind that operates across Northern Europe, would dampen the incentive to siphon so much value to the top. A federal law requiring that a third of corporate board seats be filled by employee representatives would change the conversation in the compensation committee. These are not radical proposals; they are the ordinary furniture of a modern economy.

The $100-million-plus CEO pay package is not a market signal. It is an engineering decision made in a room by people who will never harvest the vegetables, stock the warehouse, or sit with someone’s mother in a senior-housing facility at two in the morning.

The compensation committee is a circle, and the circle is unbroken.

The mill was called Manitoba Rolling Mills when my grandfather worked there, and Gerdau when my father did. The name changed. The ownership changed. The work stayed the same. The architecture is working exactly as designed. The work is still to be done.