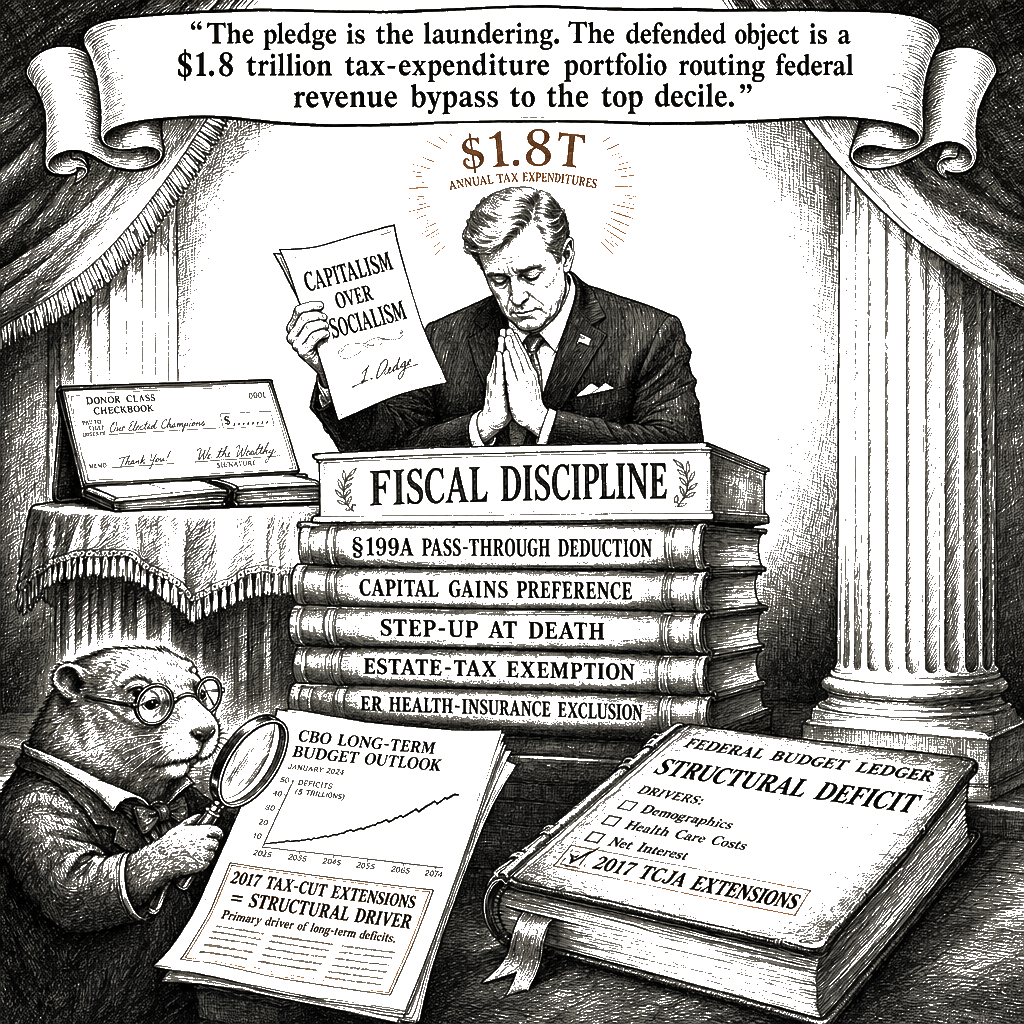

Centrist Democrats are laundering donor-class tax capture as fiscal discipline. The Tuesday primary results and the subsequent pledge signed by ten House members for “fiscal discipline” convert a revenue-baseline dispute into a moral panic. The signatories are alarmed by a left flank running on Medicare for All and the taxation of concentrated wealth. The centrist response is the invocation of fiscal discipline. The institutional documentary record shows that the centrist coalition’s version of fiscal discipline is the defense of a $1.8 trillion annual tax-expenditure portfolio that routes federal revenue bypass to the top decile.

That left flank swept the New York primaries on Tuesday — the Mamdani-backed candidates running on tax-the-rich platforms defeating incumbents the centrist coalition had protected. The publication of record and the centrist strategists frame the contest as a war over the party’s identity, arguing that only moderates can win the battleground states needed to reclaim power. The identity frame is a wonk-laundering operation. It obscures the budget mechanics and the electoral geography. Third Way’s own district analysis — the turnout-margins math the centrist coalition deploys — shows the seats the left flipped in New York are, on average, 36 points more Democratic than the country as a whole. The GOP-held seats the centrists claim they must moderate to win are, on average, eight points more Republican. The centrist coalition is not defending the terrain the party needs to capture; it is using the battleground map as a shield to protect the deep-blue fiefdoms where their donor class is most concentrated.

The federal budget does not run on identity; it runs on the baseline. The Congressional Budget Office’s Long-Term Budget Outlook identifies the structural deficit drivers. They are not the social-insurance proposals of the ascendant left. They are the revenue shortfalls baked into the current-law baseline when the 2017 corporate-rate reductions and the doubled estate-tax exemption are extended. The centrist policy establishment has consistently defended the current-policy baseline gimmick that hides those extensions.

The last major fiscal-discipline collision inside the Democratic caucus arrived with the 2022 Inflation Reduction Act, when IRS enforcement funding became the proxy fight. The Joint Committee on Taxation scored the bill’s IRS enforcement funding as a net revenue raiser over the budget window. The Congressional Budget Office confirmed that the enforcement of existing tax law against the top one percent and corporate non-compliance would reduce the deficit. The centrist coalition treated this deficit reduction as a political liability, consenting to a $20 billion rescission in the Fiscal Responsibility Act of 2023 (P.L. 118-5) that structurally weakened the enforcement mandate. The authors of Tuesday’s pledge defended the right of the top one percent to underpay their statutory liabilities against the social-democratic proposal to raise the statutory liabilities in the first place.

The pledge commits the signatories to capitalism over socialism. In the Joint Committee’s taxonomy, the federal government routes approximately $1.8 trillion annually through the tax code via tax expenditures. The largest are the exclusion of employer-provided health insurance (approximately $300 billion annually), the preferential rate on capital gains and qualified dividends, and the §199A pass-through deduction enacted in the 2017 Tax Cuts and Jobs Act. The tax-expenditure portfolio is a regressive transfer mechanism. The centrist coalition’s defense of this portfolio is the operational definition of the capitalism they are pledging to protect, a defense now colliding with the DSA-backed left wave that swept the Democratic primaries and a broader socialist surge from New York to Westminster. The left’s proposal to tax unrealized appreciation or to repeal the stepped-up basis at death is not a rejection of the market; it is an attempt to close the tax-expenditure architecture — §199A, the capital-gains preference, the step-up-at-death provision — that the empirical literature identifies as the engine of the buy-borrow-die avoidance strategy.

The score is the score. The Democratic contest is not a conflict between fiscal responsibility and socialist excess. It is a conflict between the protection of the tax-expenditure portfolio and the taxation of the capital that benefits from it. The ten House members who signed the pledge are not defending the federal budget. They are defending the accounting gimmick that allows the top decile to treat the tax code as a collection mechanism for everyone else.