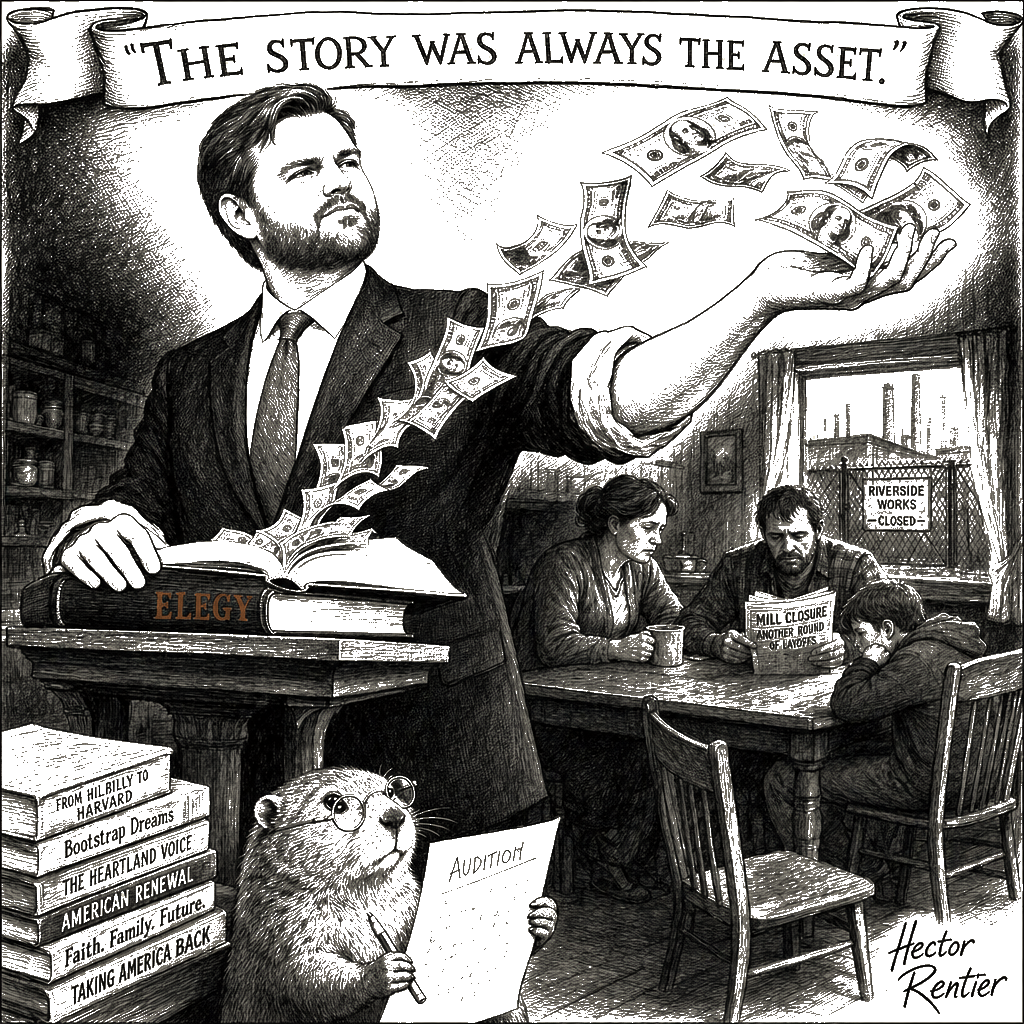

The working-class Americans JD Vance wrote about don’t need another memoir about their decline. They need an equity stake in the things they keep building. And according to a Wall Street Journal report on his 2025 financial disclosure, Vance made as much as $7.4 million last year — the bulk of it in royalties on a 2016 memoir that turned his mother’s addiction and his grandparents’ Appalachian kitchen into a publishing asset, the rest piled in from a venture-capital firm that paid him in a promissory note, from ETFs, from bitcoin, from a D.C. rental property, in an administration where the president alone reported more than $1 billion in crypto earnings in 2025. The structure of the money is the story.

Let me be plain about the part I am not going to litigate. A bestseller should pay well. Upward mobility is real, and the people who manage it are not villains for managing it. I am not anti-market. I am anti-extraction, and there is a Grand Canyon between the two. The question is not whether JD Vance earned his royalties. The question is what the political economy he represents has built for the working-class Americans whose story he monetized.

The neutral language of a financial disclosure is designed to hide the actual mechanism. It lists “book royalties” and “venture-capital firm” as if they were the same kind of line as a public-school teacher’s pension. They are not. The royalties came from packaging the decay of Appalachia for a coastal audience that wanted to feel informed about it. The venture capital came from a model that takes a position in a business, optimizes the position, and exits — usually leaving the workers with a smaller share of the company and a larger share of the debt. The working-class towns he wrote about were treated as a literary subject, a problem to be documented and shelved. The venture-capital model treats the workers in its portfolio the same way: as an input to be optimized, not an owner to be empowered.

This is not an abstract critique of the asset class. It is written directly into the plumbing of his own firm. Vance did not report a salary from Narya Capital Management. He received a promissory note from the fund itself, worth up to $1 million in income last year. That is the architecture of extraction in its purest form: compensation structured as an IOU from the fund to the general partner, with the principal paid before anyone else in the ecosystem — workers, portfolio companies, limited partners, the towns where the jobs are — sees a dime. When the mechanism that pays you is the mechanism that squeezes the workers, the incentive is not to build the company. It is to bleed it.

The transformation is the story. The memoir was the audition. The book was the credential. The credential said: I come from there, I can speak for them, I have suffered enough to be trusted. The market priced that credential the way markets price every credential. It paid him to keep being the voice of a class he was actively leaving. Working-class readers bought the book because they believed the author was one of them. The author used the book to become someone they will never be. His 2024 disclosure showed between $212,000 and $1.3 million. His 2025 disclosure shows up to $7.4 million. That is not a raise. That is a class transformation, on the same timeline as his reinvention from Ohio memoirist to MAGA heir to vice president. The exit was always the product.

The rest of his portfolio reads like a blueprint for collecting rent on the economy rather than building productive capacity inside it. Up to $500,000 in bitcoin. Up to $50,000 in rental income from a Washington, D.C., property. As much as $2.6 million in exchange-traded funds. A stake sold out of a fund tied to an AOL co-founder. He does not need the venture fund to pay him in cash; the promissory note will do. He does not need the bitcoin to liquidate; the appreciation is the point. What he needs is the office. The office is what converts the memoir into perpetual royalties, the venture fund into perpetual credibility, and the working-class provenance into a perpetual license to claim he represents the people whose wages his administration has no plan to raise. The story was always the asset.

I’m often told I am too young to grasp why the functioning alternative cannot possibly work here. Walk me through it slowly. Explain why a Norwegian cousin and an American cousin, born the same year, face such different odds of being bankrupted by a hospital — and do it without the phrase “American exceptionalism,” since the exceptional part, in this telling, is the bankruptcy. The difference is ownership.

We already have the blueprint for an economy where the working class actually owns the thing. It is not the gulag, and it is not a coastal fantasy. It is the roughly 15 million Americans who already belong to an Employee Stock Ownership Plan, according to the National Center for Employee Ownership. It is the Cooperative Home Care Associates in the Bronx, where more than 2,000 home-care workers — doing the exact kind of essential, undervalued work that defines the abandoned towns he wrote about — built a cooperative that pays them a living wage and keeps the profits in their own hands. It is the approximately 42 million Americans who belong to a rural electric cooperative, per the National Rural Electric Cooperative Association, and the more than 145 million who use a credit union, according to America’s Credit Unions. We already do this; we just will not say the word.

The economy is a set of choices, not the weather. You can choose an architecture where a politician makes up to $7.4 million writing about the people he governs, while those people still do not own a share of the companies they keep running. Or you can choose the plumbing. You can build the co-op, the public option, the bargaining structure. You can weld the trap doors shut. The working class does not need another elegy. It needs the keys.