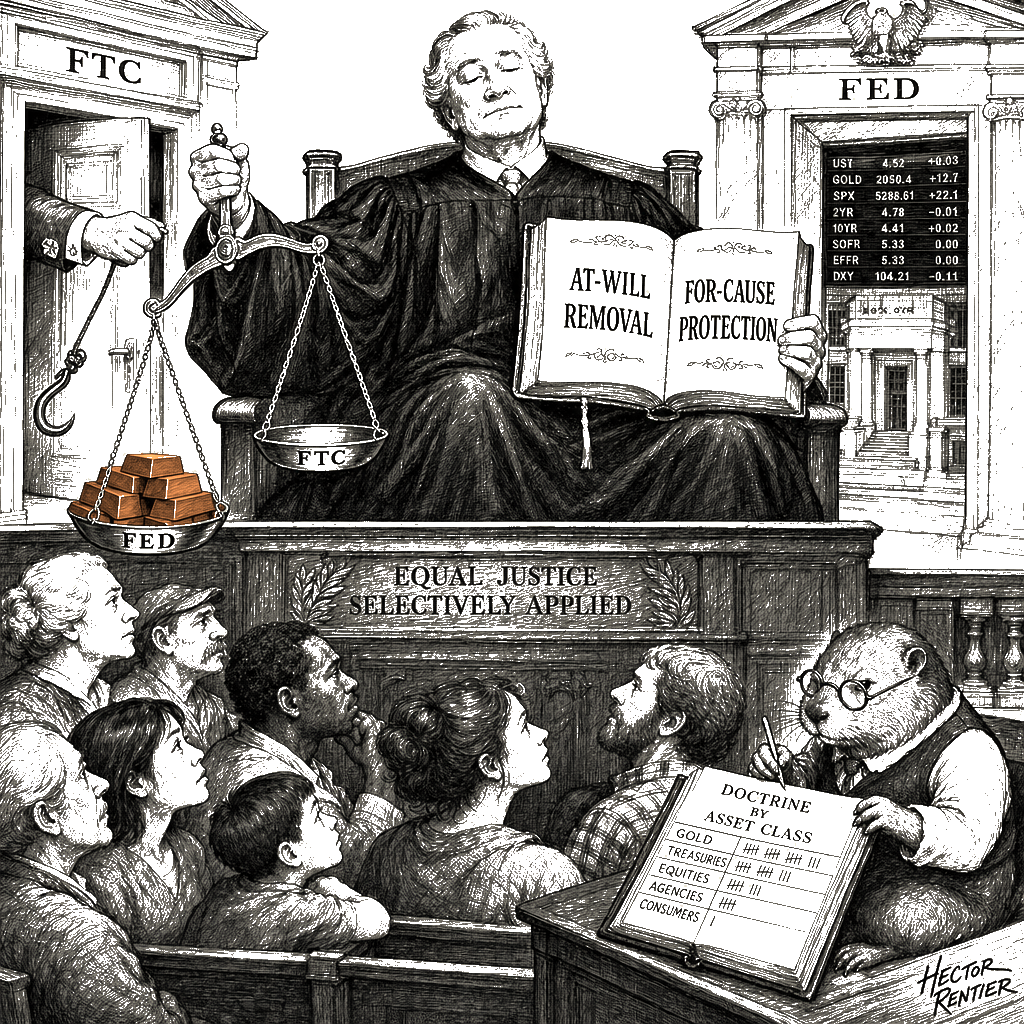

The Roberts Court picked which executive agencies the President controls.

That is the substantive read of the two rulings issued Monday. In Trump v. Slaughter, the Court gave the President at-will removal authority over Federal Trade Commissioners by overturning Humphrey’s Executor. In Trump v. Cook, the Court denied the President at-will removal authority over a Federal Reserve governor and pronounced the Fed a structural exception to the rule Slaughter had just announced. The Roberts Court calls this the Constitution. It is the Court exercising structural preference, and the doctrine is what the structural preference requires.

The Slaughter majority’s steel-man runs as follows. The Federal Trade Commission today enforces some eighty statutes covering “almost every facet of the Nation’s economy,” and the tasks it undertakes are “the very essence of ‘execution’ of the law,” as Chief Justice John Roberts wrote for the six-justice majority. The Framers designed the presidency to “operate with proper energy & vigour,” and Humphrey’s Executor v. United States (1935) — a ninety-one-year-old precedent grounded on what Roberts called “a highly circumscribed and almost fictional view of the FTC’s role” — prevented the President from removing officials charged with enforcing those laws. Overturning Humphrey’s restores the constitutional structure. The Chief’s opinion even quotes Justice Kagan’s 2001 Harvard Law Review article for the proposition that Humphrey’s Executor compromised Congress’s legislative power by encouraging delegation to agencies insulated from presidential control.

The Cook majority’s steel-man runs as follows. The Federal Reserve occupies a unique position in the American government, with roots in the First and Second Banks of the United States. Monetary policy requires insulation from short-term political pressure. A President who could fire a Fed governor for “any perceived or alleged misstep” — past or present — would exert improper influence over the institution’s deliberations. The Chief’s Cook opinion, joined by Justices Sotomayor, Kagan, Jackson, and Kavanaugh, requires notice and an opportunity to respond before removal.

Both opinions sound like constitutional law. Read together, they describe a Court picking winners.

The textualist premise of Trump v. Slaughter is sound. Article II vests the executive power in a single President, and any agency that enforces the law performs an executive function subject to the chief executive’s control. The Court’s trajectory from Seila Law LLC v. Consumer Financial Protection Bureau (2020) to the present has systematically dismantled the fictional separation between executive enforcement and quasi-legislative rulemaking that Humphrey’s Executor required. To the extent Humphrey’s insulated the FTC’s enforcement agenda from democratic accountability, its overruling is a doctrinal necessity.

But the Court’s unitary executive is a rule for the agencies that police corporate conduct, and a standard for the agency that manages the financial system. The Federal Reserve Board of Governors sets monetary policy, regulates banks, and serves as the systemically important financial regulator in the United States. It exercises “vast executive authority to regulate financial institutions,” in Justice Thomas’s dissent in Cook. If the Slaughter doctrine applies to those who “fall within the President’s ‘general administrative control,’” the Fed would seem to fall within it. The Cook majority declines to apply the doctrine there. The Fed, the opinion announces, is different.

The history the Cook majority invokes is a history of commercial banking, not of the administrative state. The early republic’s central banks, Thomas writes in dissent, “possessed no sovereign power.” They were commercial operations with note-issuance privileges, not administrative agencies wielding authority to regulate private financial institutions or set capital requirements by fiat. The modern Fed exercises the very executive authority the Slaughter majority insists must be subject to presidential control. Applied consistently, the Slaughter rule would sweep the Fed into the President’s at-will authority. The Court refuses to apply it consistently because the cost of doing so — to the bond markets, to the financial establishment, to the institutional prestige of the central bank — is a cost the Court will not make the polity pay.

The pragmatic case for the Fed exception is real, and it deserves to be stated plainly. Monetary policy operates on expectations; bond markets price the credibility of the central bank’s commitments; an erratic President who could fire a governor for casting the wrong vote on interest rates would inject a volatility premium into every Treasury auction. These are serious institutional concerns. But they are precisely the kind of functionalist, living-constitutionalist reasoning that the Slaughter majority repudiated when it overturned Humphrey’s. The Roberts Court cannot invoke the separation of powers to strip protection from the FTC — whose independence poses no threat to bond yields — and then invoke institutional pragmatism to shield the Fed, whose independence does. The Constitution either demands presidential control over executive officers or it does not. The Court’s answer, it turns out, depends on the asset class.

Justice Kavanaugh’s position illuminates the architecture. He joined the Slaughter majority that gave the President control of the FTC. He joined the Cook majority that denied the President control of the Fed. The same justice, on the same day, applying what we are told is the same constitutional structure to opposite outcomes. The Court does not explain what makes the Fed structurally different from the FTC in terms that survive Slaughter’s reasoning. The Court explains it in terms of which agencies the Chief wants the President to run.

Justice Gorsuch’s Slaughter concurrence calls for the Court to “resurrect its dormant non-delegation doctrine” and to force Congress to reclaim the legislative authority it has handed to the executive branch. The concurrence observes that Congress might not have delegated so much power “had it known that the President would come to control” the agencies. The Court, Gorsuch writes, “has sometimes shrunk from applying that rule.” If the Court applies non-delegation now, Congress will have to take back the authority it has been handing to agencies for a century. That would be the constitutional restoration Gorsuch describes. What the Court actually did in Slaughter — transfer control of the agencies from insulated commissioners to the President — is not that. It is a transfer of power within the executive branch, not a return of power to Congress. The concurrence’s diagnosis is correct; the majority’s remedy does not address it.

The Federal Reserve decision will produce litigation. Thomas’s dissent identifies the doctrinal opening. If the Fed’s “vast executive authority” does not require presidential removability, then the question becomes which other agencies also exercise “vast executive authority” but enjoy the carve-out the Court has now recognized for the central bank. The Securities and Exchange Commission, the Consumer Financial Protection Bureau, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency all exercise substantial executive authority over regulated industries. None has the Fed’s monetary-policy function. Each has a colorable argument under the Cook majority’s reasoning that it, too, deserves structural protection from at-will presidential removal. The Court now has the job of distinguishing the Fed from those agencies on grounds that the Slaughter majority’s own logic does not supply. The cases will arrive.

This is the architecture of asymmetric constitutional hardball. The conservative legal movement has spent four decades since the Federalist Society’s founding in 1982 building the doctrinal containers to dismantle the New Deal regulatory state: the unitary executive, the major questions doctrine, the nondelegation revival Gorsuch pressed in his Slaughter concurrence. When those containers threaten the financial order, the Court retreats to the exact functionalist reasoning it rejected in the administrative state. The for-cause protection of the Fed is not originalism; it is institutional conservatism. It is the Court acknowledging that while the President may be permitted to fire the officials who enforce the antitrust laws, he cannot be permitted to fire the officials who manage the money supply.

Two rulings from the same Court on the same day produced two different executive branches — two maps, both claimed as the Constitution. The Slaughter map is structural law. The Cook map is structural preference with a doctrinal frame around it. The Roberts Court has spent a decade dismantling the headless fourth branch, only to discover, at the exact moment the levers of financial power come into view, that the fourth branch was headless only where it interfered with capital. The President now controls the FTC. The President does not control the Fed. The doctrine is what the Court needs it to be.