John Roberts destroyed the independent agencies to protect the central bank.

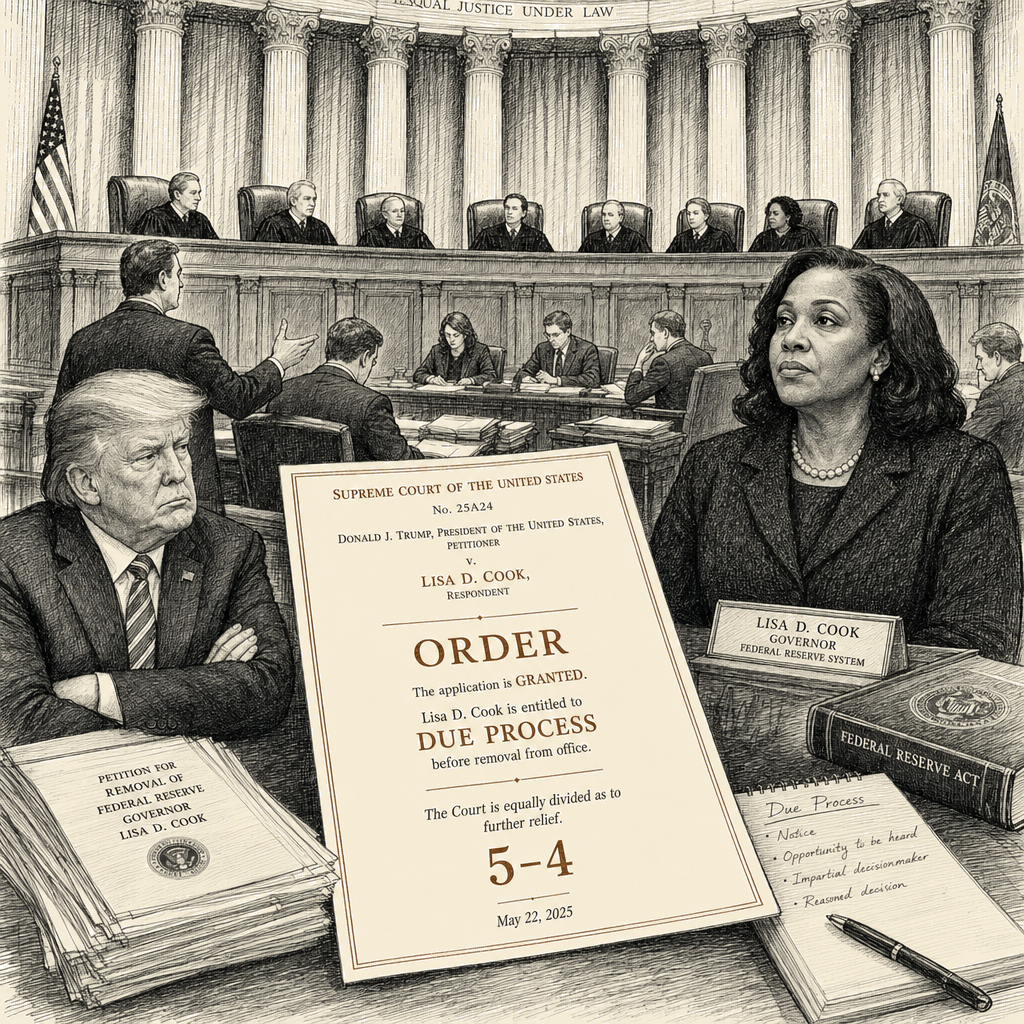

The steel-man for the Chief Justice requires taking his historical taxonomy seriously. On Thursday, Roberts wrote for a five-Justice majority that the President cannot fire Federal Reserve Governor Lisa Cook at will, because the Federal Reserve Act of 1913 established a board with 14-year terms and for-cause removal that “follows in the distinct historical tradition of the First and Second Banks of the United States.” The First Bank operated from 1791 to 1811, the Second from 1816 to 1836. The Federal Reserve draws on a two-century tradition of central banking insulated from direct presidential control. NLRB v. Noel Canning, 573 U.S. 513 (2014), established that historical practice can constrain executive removal power. Under this framework, the Fed is not an ordinary executive agency subject to the unitary executive theory; it is a unique monetary entity with a specific historical pedigree exempt from standard Article II hierarchy. Meanwhile, for the Federal Trade Commission and the National Labor Relations Board, the 1935 unanimous precedent in Humphrey’s Executor v. United States, 295 U.S. 602 — which had protected all such independent agencies from at-will removal for ninety years — was functionally unworkable and discarded. The steel-man is coherent: a two-tier taxonomy where the central bank survives on originalist grounds, and the rest of the administrative state falls to the unitary executive.

The audit requires looking at what that taxonomy actually does, and what it leaves out. The Federal Reserve was created in 1913. The Federal Trade Commission was created a year later, in 1914. The National Labor Relations Board was created in 1935, the same year Humphrey’s Executor unanimously upheld the FTC’s independence from at-will removal. All three agencies are Progressive Era and New Deal creations — the same constitutional logic, the same century of practice. The Court did not engage the FTC’s identical vintage. It did not engage the NLRB’s identical pedigree. It did not engage Humphrey’s Executor’s nine-decade reign. By 6-3 the same afternoon it protected the Fed, the Court reversed the unanimous precedent that had underwritten the entire federal independent regulatory state.

This is selective formalism at the highest level. The 1791-to-1836 window — two banks, two decades each, two charter lapses — qualified the Federal Reserve for historical-tradition protection. The 1914-to-2026 window — one agency, one century of continuous operation, one unanimous Supreme Court precedent protecting its independence — did not qualify the FTC. The Court did not explain why the First and Second Banks’ charters are entitled to more solicitude than the FTC’s operating history. An honest application would have extended the historical-tradition reasoning to the FTC and NLRB, or refused to extend it to the Fed. The Court picked neither path. It picked selective application, and in doing so assumed a gatekeeper role the Constitution does not give it: deciding which independent institutions survive presidential control.

Then there is the stare decisis posture. The Roberts Court has, in recent terms, articulated stare decisis factors including the quality of the precedent’s reasoning, its workability, and the reliance interests it has generated. Humphrey’s Executor was unanimous. It was settled for ninety years. It underwrote the structure of the entire federal independent regulatory state. The Court did not engage those factors in the 6-3 reversal. It did not explain why a unanimous ninety-year-old precedent failed the stare decisis test the Court has invoked elsewhere. The selective invocation of stare decisis in some cases and its abandonment in others is a documented pattern.

The Cook decision itself exposes the second audit: the narrow-but-not-really framing. The Roberts majority protected Cook by sending her case back to the lower courts. The protection is provisional. The Court did not hold that Trump’s stated grounds for firing her were inadequate. It held that the lower courts should examine those grounds in the first instance. The Court did not define the standard of review for “cause.” It handed the lower courts a blank check. If the lower courts adopt the administration’s narrow definition — that mortgage-related allegations, even unproven, constitute cause — the firing stands. Roberts rejected the unreviewable-at-will argument, but remanded the case to determine if the alleged “cause” is sufficient, a process that will likely take years. Cook’s lawyers have documented that five Trump officials, including acting Attorney General Todd Blanche, submitted the same kind of mortgage application without a whisper of scrutiny. The lower courts must now sort out whether a President can manufacture “cause” by weaponizing selective document reviews.

The Fed was spared only because the five Justices in the Cook majority and the four Justices appointed by Democratic presidents aligned to block a political capture of monetary policy that Powell had warned would permanently destroy trust in the Fed. Every living Fed chair, every living Treasury secretary, and an army of prominent economists signed a brief begging the Court not to tinker with the Fed’s independence. The briefs did not persuade on originalist grounds; they persuaded on market-stability grounds. Roberts invoked a “historical tradition” lifeboat for the central bank while the administrative state drowned.

This is the regime of the asymmetric unitary executive. The six-Justice supermajority has spent years building the doctrinal stack to place the President at the apex of the administrative state. When the target is a civil-rights agency, a labor board, or a consumer-protection bureau, the unitary executive demands at-will removal, and the 1935 precedent falls. When the target is the central bank, the sudden invocation of the First and Second Banks reveals the methodology for what it is: a doctrine that expands to swallow whichever agency the political coalition wants to control, and contracts the moment it threatens the sovereign debt market. The unitary executive now has a bond-market exception, written by the Chief Justice himself.

The institutional defense the Court only partially provided, the Fed is now providing for itself. Powell, “enraged by the attack on his integrity,” has decided to serve out his term as a regular governor rather than vacate his chair and hand the administration another seat — the most senior monetary official in the country treating his own tenure as a tactical asset in a political war. The President who previously launched a criminal investigation into Powell over building renovations has now established that he can fire the heads of the FTC, NLRB, and every other formerly independent agency at will. The Fed remains independent only on a five-Justice razor, shielded by a doctrinal patch that applies to no other agency in the federal government.

The Federal Reserve’s independence is no longer a structural feature of the American government. It is a five-Justice injunction, contingent entirely on the bond market’s tolerance for a politicized discount window. The rest of the administrative state is gone.