The SEC is laundering an enforcement action to shield a trillionaire from accountability.

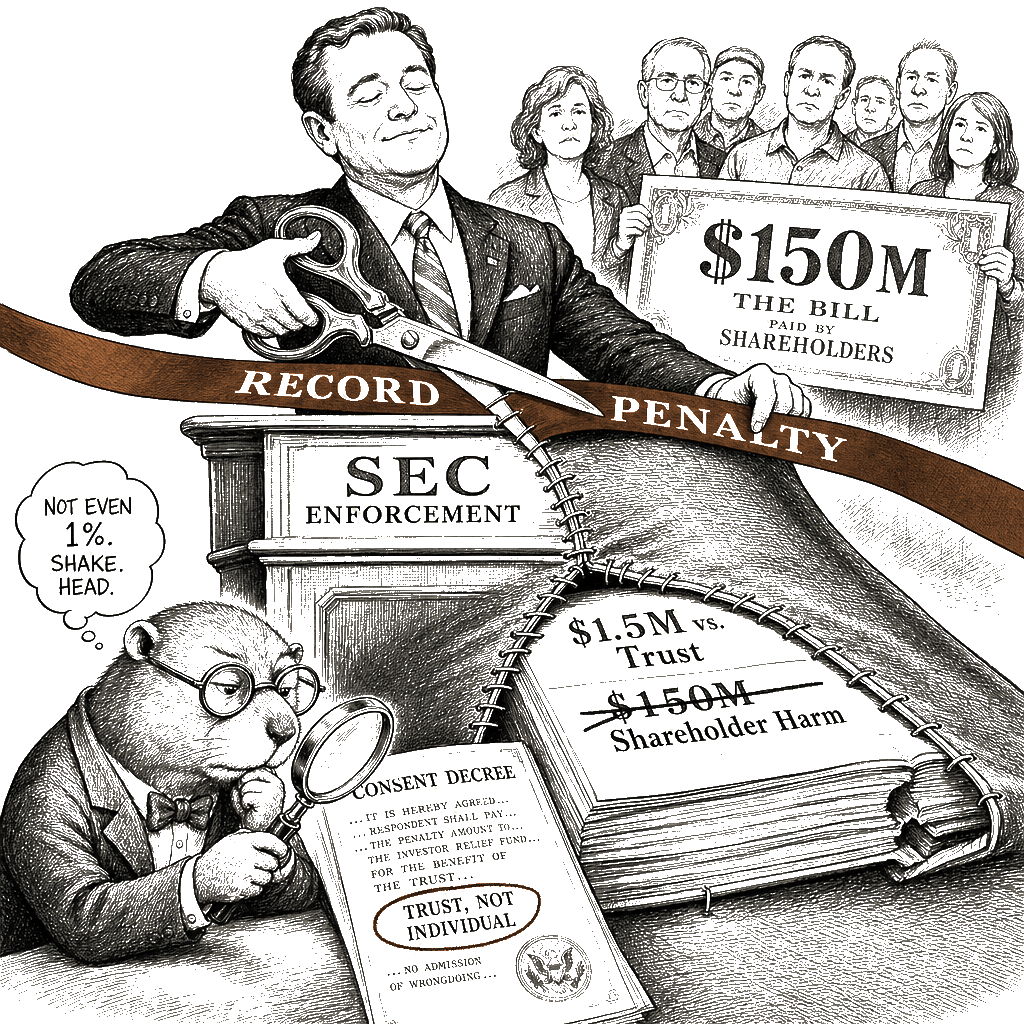

Here are the numbers. Section 13(d) of the Securities Exchange Act requires any person acquiring more than 5 percent of a registered class of equity securities to disclose that fact within ten days. Musk crossed 5 percent of Twitter in 2022. He did not disclose the crossing until his stake reached roughly 9 percent. The delay cost Twitter’s shareholders as much as $150 million when he closed the acquisition of what is now X. The SEC charged him in January 2025. The resulting consent judgment is $1.5 million. For every hundred dollars stripped from shareholders, the Commission recovered exactly one dollar. The Commission describes the $1.5 million figure as the largest penalty ever assessed for a Section 13(d) late-filing violation. The characterization is technically accurate. It is also a confession about the baseline.

The consent decree runs against the trust that held the shares, not against Musk personally. The SEC’s June filing acknowledged that the arrangement was requested by Musk’s side and called it, in the agency’s own word, an “SEC compromise.” Judge Sparkle Sooknanan of the U.S. District Court for the District of Columbia, in her opinion approving the deal on July 9, asked the question the structure invites: why the proposed consent decree runs against the Trust and not Mr. Musk — “other than allowing Mr. Musk to proclaim publicly that he has been cleared of wrongdoing” — and why the SEC has permitted that result. The structural consequence is a man who sues rivals over orchestration claims and prepares record-breaking public equity offerings, operating under a regulatory perimeter drawn to exclude this kind of accountability.

The Court’s role in reviewing a consent judgment is narrow. Federal courts apply a deferential standard rooted in the court’s inherent equitable authority, and may reject a consent decree only when it “makes a mockery of judicial power.” Sooknanan found the settlement did not meet that threshold for rejection. She also wrote that she had “significant misgivings” and that the SEC’s decision-making “raises red flags.” She closed by observing that whether the Executive Branch has done enough to hold Musk to account “is, like many other issues, for our citizenry to decide at the ballot box.” A judge who flags red lights and then waves the car through is documenting the capture. The ballot box is not a substitute for a regulator that enforces the law on the books.

The 13(d) regime exists because rapid disclosure is the entire remedy. The market has the position; the market has not yet had the disclosure; the price has not yet reflected what the disclosure will tell it; the harm is the difference between those two states. Late disclosure under this regime is not a technical violation. It is the substantive violation. The harm is the interval between crossing the threshold and telling the public, and the penalty’s job is to make that interval expensive to manufacture. A penalty that is one percent of the alleged harm does not perform that job. A penalty that runs against a trust rather than the human being who made the disclosure decision — when the structure of the arrangement lets the human being publicly disclaim it — does not perform that job either. The fact that the Commission simultaneously describes this as the largest penalty ever for the violation is not a defense of the penalty. It is the indictment of the prior enforcement record that produced it.

The Commission has the statutory authority to seek disgorgement of the shareholder cost, to size penalties to the harm, and to name the directing individual as the respondent. An enforcement division that treats those authorities as binding constraints rather than discretionary options is the institutional remedy. The agency’s choice to deploy the “largest ever” framing while declining to test whether the result is a meaningful deterrent is itself part of the record. The agency’s choice to characterize the trust-versus-individual defendant question as a “compromise” is itself part of the record. The Court is required to accept the result, and did, while preserving a record that names them.

This is not a column about Elon Musk. This is a column about what the May 2026 settlement tells the next 5-percent filer who is thinking about how long to wait. The answer the settlement delivers is structural. Wait as long as you like. When the Commission catches you, the cost will be a fraction of one percent of the trading gain the delay produced — small enough to pocket without a phone call to your accountant. The case will run against the entity rather than you. The Court that approves the deal will write an opinion that uses the phrase “red flags” while accepting the result. That is the precedent.

The settlement is the settlement. The capture is the capture.