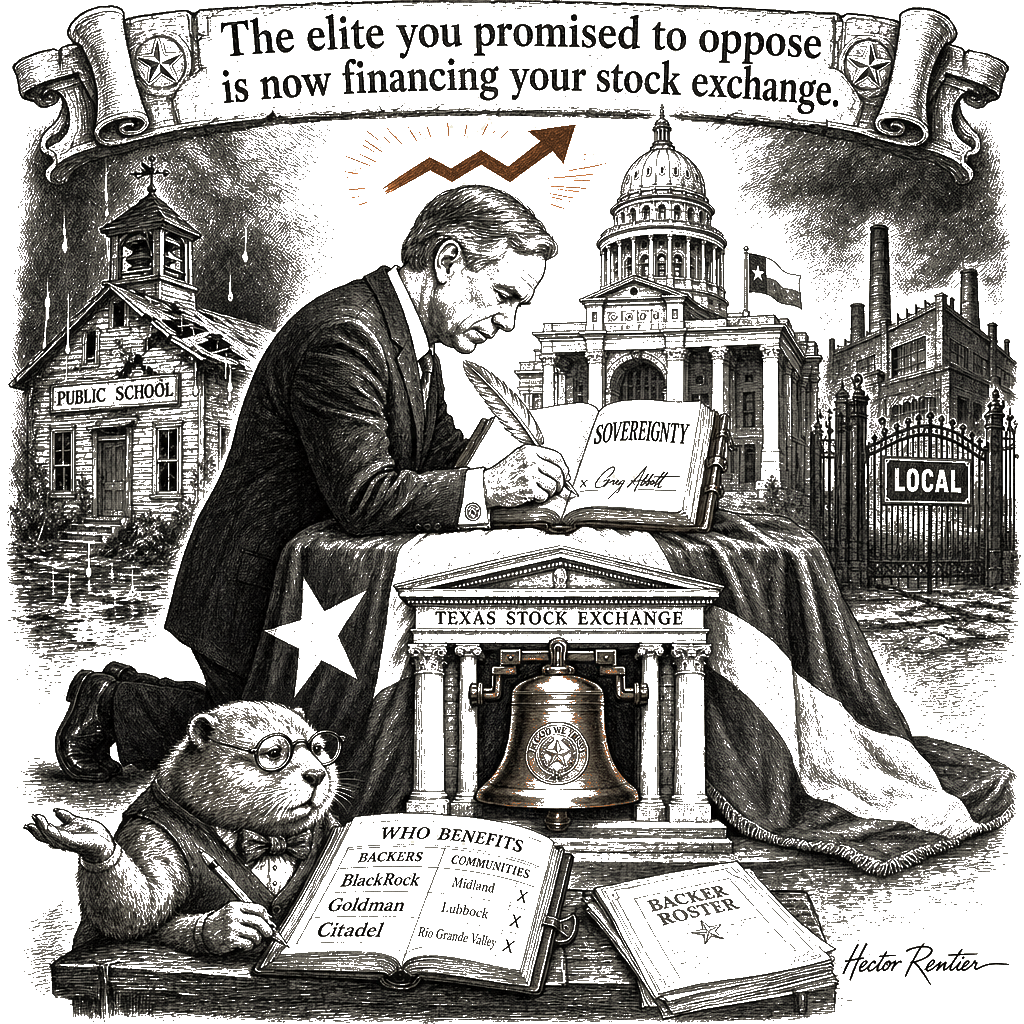

They sold the courthouse to the corporation, and they called it local control. They promised you the dignity of the working town, the political philosophy that conserves the things your grandfather built, and they delivered you a literal casino for BlackRock and the rest of the financial aristocracy. That is what conservatism has come to mean in the Lone Star State — and the proof opened for trading in Dallas on Friday. The Texas Stock Exchange went live this week, as Corrie Driebusch reports in The Wall Street Journal, backed by BlackRock, Goldman Sachs, Citadel Securities, Charles Schwab, and Fortress, and blessed by Governor Greg Abbott, who dreamed it up at a Houston steakhouse in the fall of 2022. The pitch to corporate America is plain: affiliate with Texas, escape the Delaware courts, and watch your shareholder suits get harder. It does not yet have a single company listing. The men who run this exchange are the masters of abstraction, trading mock symbols while the real economy of Main Street continues to hollow out.

There is a legitimate, honest argument to be made about the mechanics of corporate law. For a century, Delaware held a near-monopoly on incorporation, and its Court of Chancery grew accustomed to ruling as it saw fit. When the judges started striking down the compensation packages of the men in charge, those men packed up their charters and moved to Austin and Frisco. A state has a genuine interest in providing a stable, predictable legal forum for the enterprises that employ its people, and when the incumbent court system becomes erratic, it is entirely prudent to seek a new one. The NYSE-and-Nasdaq listing duopoly is a genuine problem too. Two exchanges now own the listing business in a country that ran a dozen of them a generation ago. Nasdaq’s diversity-disclosure rule did rub a great many corporate boards the wrong way. Elon Musk moved Tesla and SpaceX to Texas after a Delaware judge struck down his pay package, and Coinbase and Dell and Exxon Mobil followed. State competition for corporate charters is as American as the railroad, and Texas has every right to compete.

But a stock exchange is not a chancery court, and the cure is worse than the disease — and not by a little. Read the names on the backer’s roster. BlackRock. Goldman Sachs. Citadel Securities. Charles Schwab. Fortress. This is not an insurgency against Wall Street. It is Wall Street, opening a third franchise with a Texas flag painted on the roof. The same firms that already own the duopoly are now financing a competitor, because a competitor is what you build when the incumbent exchange’s rules start costing you money. The shareholders who will benefit are not the working people of Midland and Lubbock and the Rio Grande Valley. They are the same New York and London institutions that already own the duopoly.

And read the pitch, the part the brochures do not lead with. Affiliate with Texas. Bring your incorporation here. That is the language of a state auctioning its sovereign powers — its courts, its corporate law, its tax code — to whichever corporate bidder offers the best grievance against Delaware. The Texas Business Court Abbott set up in 2023 to lure incorporations was the prelude. The exchange is the financial capstone. By the time the heavyweights pledged their millions, the state legislature was already drafting laws to raise the bar for shareholder proposals — making it mathematically harder for the actual owners to hold the executives accountable. Legislators and exchange officials openly tease that more state laws are in the works to benefit companies listed in Texas. And the old guard isn’t just watching; the NYSE and Nasdaq have already scrambled to reincorporate their electronic subsidiaries as “NYSE Texas” and “Nasdaq Texas,” planting their own flags on Texas soil. The duopoly isn’t being routed. It is hardening its perimeter. That is not free enterprise. That is a syndicate.

This whole venture caught its political fire when Nasdaq tried to force a board-level diversity disclosure rule. Conservatives bristled, Wall Street traders started whispering about an “anti-woke” exchange, and the political class smelled an opportunity. Rick Perry, the former governor who spent fourteen years bending the state to the will of corporate relocations, is now sitting right there on the TXSE board of directors. He is the concrete face of the betrayal. This is what your movement means by the “anti-woke” exchange. It means a state selling incorporation privileges to executives who want softer courts and weaker shareholders, and dressing the sale in the costume of a culture-war complaint about a Nasdaq diversity rule that no longer exists.

I used to trade agricultural futures on a Chicago desk. I know what an exchange is. It is a marketplace with two customers: the corporations that list shares, and the traders who make markets in them. The corporations that will list on the TXSE will not be the family ranches of the Hill Country or the small-town banks of the Brazos bottoms. They will be the same publicly-traded giants that already trade on Nasdaq — SpaceX and its peers, the next Musk venture that wants the musk-friendly courthouse. When SpaceX topped $176 on its blockbuster IPO debut and the politicians cheered the billions in paper wealth, the economy of the border town reshaped itself around the whims of a single absentee billionaire, while the local school district still could not afford to fix the roof on the old brick building. The exchange will charge listing fees and data fees and routing fees. The revenue will flow to the backers and the state. The working people of Texas will get what the state has spent a decade selling them: four and a half thousand Goldman employees in a Dallas campus, a JPMorgan payroll that outstrips New York, a London trade office to recruit British companies to the Texas franchise, and a story about how they stood up to Delaware. A state that measures its sovereignty in Goldman jobs has forgotten what sovereignty means.

The standard critique from the opposite side of the aisle will oppose this because it exploits the worker or increases the wealth gap. I oppose it because it destroys the institution. It severs capital from its place. It violates the principle of subsidiarity by handing the local economy over to a distant, unaccountable leviathan. It wipes out the mediating institutions — the local bank, the credit union, the family-owned firm that knew the names of its depositors — by centralizing financial power into the hands of the very monopolies the American populist tradition, from Andrew Jackson to Louis Brandeis, taught us to fear. They tell you this is the free market. But the free market is supposed to be a mechanism for allocating the things people actually need. This is a mechanism for concentrating power, for turning the earth and the labor of the community into a disposable abstraction owned by a fund manager in Manhattan who will never set foot in the county. A business belongs to the people who work in it, the people who live near it, and the people who will inherit it. It is not a plaything for a hedge fund.

You told working people for forty years that the country was being stolen by a coastal elite — and you were right about the elite, which is why the pitch landed. But the elite you described, the one you promised to oppose, is now financing your stock exchange. The state you said you wanted to defend against Washington has been auctioned, piece by piece, to the very capital concentration you once railed against. It is the fusion of state and concentrated capital that conservatism was supposed to oppose — the post-liberal trap in a corporate suit. The Texas Business Court was sold as a check on Delaware overreach. The exchange is being sold as a check on NYSE and Nasdaq consolidation. Both are real problems. Both are being answered by deepening the disease: concentrated power finding a more accommodating host. A sovereign state softening its own courts to win a listing war is not local control. It is the selling of the courthouse.

The answer is not to beg the state of Texas to regulate them, and it is not to follow the post-liberals into building a concentrated state-moral power to crush them. The answer is to build the counter-model. The cooperative. The mutual. The credit union. The widely-held firm. The Main Street underwriter that does not need a national exchange to find its customers. The listing duopoly is a problem of concentrated capital. The answer to concentrated capital is not a third franchise for concentrated capital, sponsored by a state willing to soften its courts to win the bid. The answer is more owners, not a new exchange. Leave the town its life. The earth was given for all — not as a slogan for a listing brochure, but as a cap on what any state may sell to the highest bidder.

While the men in Houston were at their steakhouse deciding who got to trade the future of the American economy, the men and women of the Adams-Columbia Electric Cooperative were already doing it. More than thirty-one thousand member-owners across twelve counties in central Wisconsin, governed by a board they elect, keeping the lights on and the dividends local. The co-op does not trade mock symbols. It builds the town. It centralizes nothing and distributes everything. That is the answer to the curse of bigness that actually conserves what was built. The Texas Stock Exchange will be a real exchange. It will trade real shares. Some companies will list there to please their executives or to court a statehouse. But the courthouse has been sold all the same, and the men and women of the Texas countryside will still be waiting for an institution that is actually theirs — a co-op they own, a credit union on their main street, a mutual that answers to the people of the town and not to the people of the suite. We just have to mourn that the people who claim to speak for the tradition are the ones selling it out.