They tried to buy the casino outright; when that failed, they decided to build a fake-money one in your child’s pocket and call it a civic exercise. The reporting on Mark Zuckerberg’s failed bid to acquire Kalshi, the leading prediction-market firm, before his pivot to a Meta AI-powered app called Arena, reveals the logical endpoint of an economy that has run out of tangible things to strip-mine and has moved on to extracting the civic life of the citizen. The talks, according to Bobby Allyn at NPR, collapsed last year for reasons still in dispute — some say Tarek Mansour, Kalshi’s co-founder, would not move; others say Meta flinched at the legal and ethical mess. Whatever the cause, the instinct is the same. The Federal Trade Commission alleged in court last year that Meta runs a “buy or bury” strategy: acquire the rival, or clone it until it dies. The Threads partnership struck in March, embedding Kalshi odds directly into the social network, was the foothold. The Arena app is the enclosure — three billion users, a market cap north of a trillion dollars, a record of failing at the metaverse, failing at crypto, failing at every shiny object they clutch, and now they want your perception of reality as the last available yield.

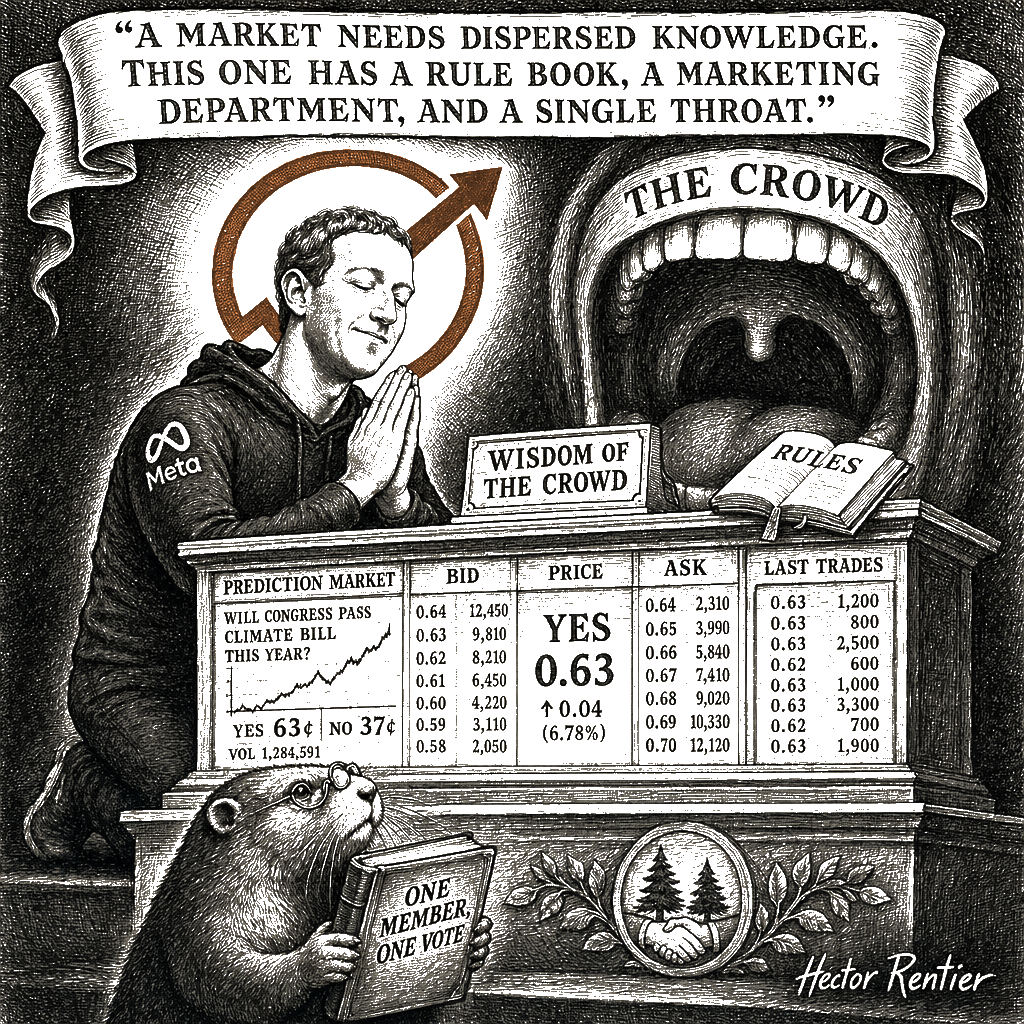

I will grant the case. The wisdom-of-crowds argument for prediction markets is real. A market in probabilities is a market in information, and there is no honest reason to think a man who puts his money where his mouth is knows less than a man who only puts his mouth. The Hayekian defense is real: dispersed knowledge, the wisdom of crowds, the price as a signal. A prediction market is, in a narrow sense, an opinion poll you have to pay for, and the most truthful kind of opinion poll is the one people cannot lie on. To dismiss it as nonsense is to pretend the experts have been right all along, and they have not.

But the Hayekian defense collapses the moment the market in question is Meta’s. The internal documents NPR reviewed say the company’s artificial intelligence systems will “power the questions and determine who wins or loses.” That is not a price system aggregating dispersed knowledge. That is a single firm deciding what the question is and what the answer is. The wisdom of crowds requires a crowd. Meta’s app has a customer base, scoring itself by rules written in Menlo Park, and calling the result a market. The libertarian defense of the price signal was never a defense of a price signal set by a private central planner — a firm with a balance sheet larger than most countries’. That is not a market. That is a private central planner with a marketing department.

I traded agricultural futures. The nature of the mechanism is to detach the paper from the soil, to replace the weather with the hedge, to substitute the life of the farm for the abstraction of the pit. The men who built Kalshi and Polymarket have done the same to the civic square. They have taken the news and turned it into a slot machine, processing $220 billion a month in bets on the collapse and continuity of the world — up from roughly $28 billion a month a year ago, a near-octupling driven mostly by sports betting. War in Iran becomes a position. The capture of a head of state becomes a position. The Google search of the year becomes a position. Every civic event, every uncertainty a democracy is supposed to argue about in public, becomes a line on a book, with a vig for the house.

The conservative tradition knows that a market economy requires a moral society to bound it. The libertarians will tell you that two parties, voluntarily exchanging, in a market, on a price, is by definition freedom, and that any regulation is tyranny. The conservative tradition begins earlier, and asks what kind of creature this market is producing, and at what cost to the institutions that hold a country together. The market was invented to allocate scarce goods; it was never meant to price the soul. A society that bets on everything stops deliberating about anything. This is the conservative criticism Edmund Burke made of the French Revolution: a politics of abstraction in which the actual life of the actual place is replaced by the general will — or, in our case, the general price. The earth was given for all, as Wendell Berry has long reminded us, but the attention of the young is being strip-mined by a monopoly that sees your perception of reality as the last available yield.

And the exchange is not what the libertarians imagine. It is one firm — proposing to absorb the leading prediction market, and when that failed, deciding to clone it. They are not engaging the citizen. They are farming the attention of the isolated individual, feeding the dopamine loop that keeps him staring at the screen while the town hollows out around him.

And the rot is already documented. The Justice Department has two open criminal cases: a special-forces soldier alleged to have bet on the capture of the Venezuelan president using classified information; a Google employee alleged to have made more than a million dollars betting on which names would trend in search. These are not edge cases. They are the model working as designed. A market in secrets with no public-interest floor is a market in corruption. The industry calls this “insider trading,” as if it were a flaw; it is the natural yield of a market with no floor. And the fix is not better enforcement at the perimeter. The fix is at the centre. A member-owned exchange, where the bettors are the governors and the surplus returns to the members, has no incentive to make a book on classified information or search-trend leakage — because there is no distant shareholder to harvest the gain, and the members themselves are the ones bearing the cost of a corrupt tape. The co-op’s governance floor is the very floor the venture model lacks.

The politics ratify it. Kalshi is overseen by commodity regulators because the company has argued, successfully, that its products are swaps, not bets. The current administration has protected the company against state gaming officials who say the products are bets. The conservative tradition has a name for what is happening here. It is not free-market capitalism, which is voluntary exchange between decentralised parties under a rule of law that applies to all. It is mercantilism — state-backed privilege extended to a single firm, regulatory shields purchased by political access, a market rigged by those with the balance sheet to rig it. The men who built that system were not conservatives. They were crown favourites. The libertarian, for his part, offers a surrender to the “free market” of the slot machine; the federal commissioner offers a bureaucracy to manage the casino. Neither has a word for the sacred, for the things that must remain un-priced.

The conservative answer is not a ban. It is the co-op. A prediction market is, in form, a member-owned mutual — and that is what the Rochdale Pioneers were doing in 1844: a cooperative association, each member with one vote, pooling capital for a common purpose, with the surplus returned to the members, not extracted by outside shareholders. The Mondragon Corporation in the Basque country is the proof of scale: roughly seventy thousand worker-owners, around eleven billion euros in annual sales, an internal pay ratio of roughly five to one, no outside shareholders. Organic Valley, in La Farge, Wisconsin — a couple of hours southwest of where I am writing — is the proof of place: sixteen hundred family farms, owned by the farmers, the single largest supplier of organic milk in the country, with the surplus returned to the members. Rural electric co-ops electrified rural America, against the judgment of the investor-owned utilities that said it could not be done. Credit unions still do most of the small banking in the small towns. The model is not speculative. It has been in continuous operation since before the Civil War.

Co-ops are slower than venture-funded apps. They are not slower because they are weak. They are slower because they are permanent. A venture-funded app is built to be sold; a cooperative is built to be inherited. The reason the buy-or-bury machine cannot capture the co-op is not that the co-op is too small to be seen. It is that the co-op has no exit price. The members own it. The members govern it. The members answer to one another. A firm that runs a “buy or bury” strategy runs out of targets the moment it meets a creature that is not for sale. The town square, the parish, the local paper, the farm cooperative — these are the mediating structures Robert Nisbet warned us to protect, the institutions that stand between the isolated individual and the leviathan. They are not efficient. They do not scale. They cannot be optimized by an algorithm. But they are the places where the person is known by name, where the community’s life is discussed as a shared trust, not traded as a derivative. The soil and the soul will survive only in the places the algorithm cannot reach.

The casino is the symptom. The problem is that the house is always one firm, and the firm is always somewhere else, and the men who run it will never set foot in the town where the bets are placed. The remedy is the one conservatives have always proposed when the market is captured by capital it cannot govern: distributed ownership, member control, and a surplus that stays where the work is done. The future is not for sale. It never was.

— Wendell Burke