A memo to the United States Senate Committee on Banking, Housing, and Urban Affairs, regarding the report of July 16, 2026, and respectfully submitted by the institution most directly affected.

To Senator Warren, Ranking Member, and to the Committee:

Doretta is a maintained account in the checking operation I hold through two shells in Vigo County, Indiana — a maintained account, by which I mean a woman of 53 who cleans rooms at a motel outside Terre Haute and whose daily balance I watch the way a pilot watches a fuel gauge. On a Tuesday in March she swiped her debit card at a Dollar General for $11.47 — dish soap, a bag of rice, a pack of hot dogs — and the transaction cleared against money that wasn’t there. I charged her $35 for the clearance. The soap was $3.29. The rice was $4.18. The hot dogs were $3.99. The fee was more than the three combined. Your debit card runs on the same arithmetic, Senator, as does the account of every constituent who has ever written to you about one. God bless the fee, which is the only honest product in consumer finance.

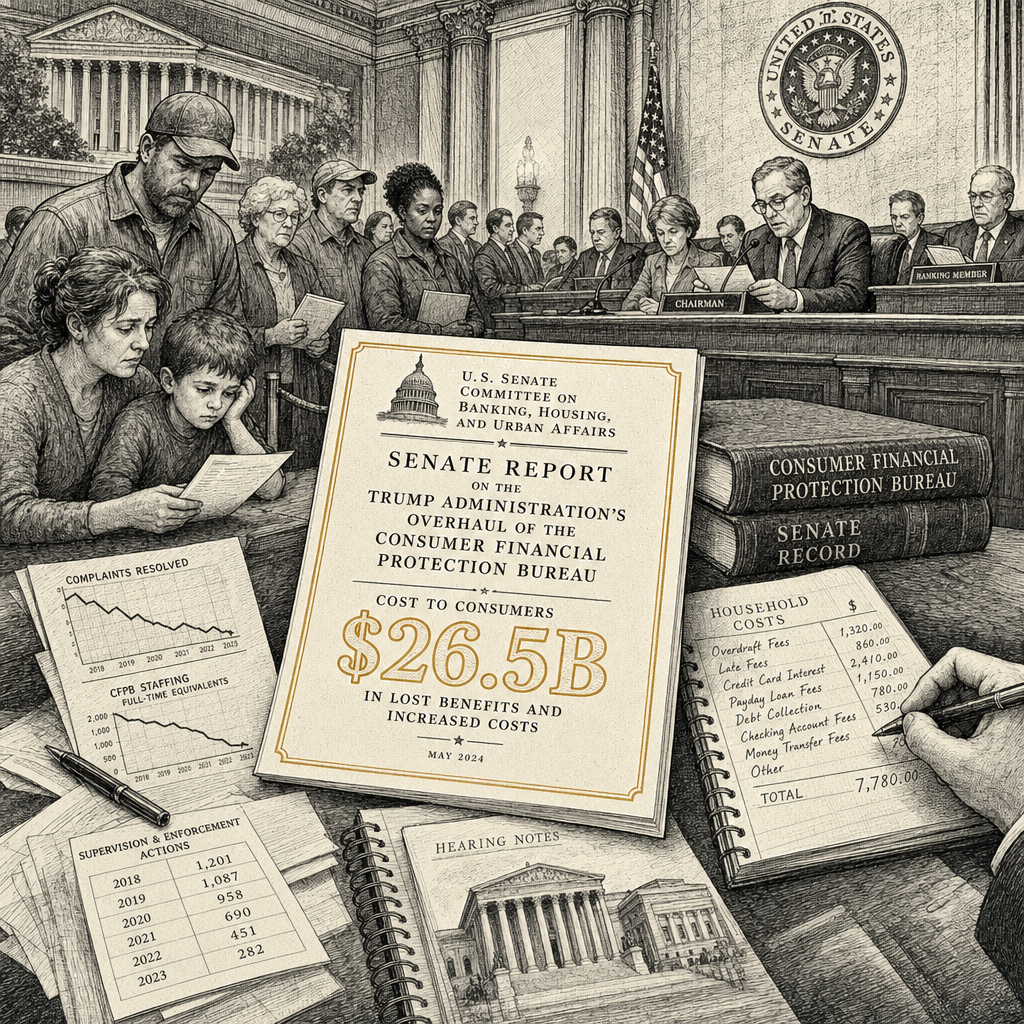

The Committee published a report this week — you released it ahead of Director Vought’s hearing — stating that the Trump administration’s overhaul of the Consumer Financial Protection Bureau has cost American consumers $26.5 billion. The Bureau scrubbed 15 years of consumer complaint data from its website earlier this year. It has dropped more than three dozen enforcement actions worth $4 billion in settlements that would have gone back to the people who paid the fees. The Senate is preparing to confirm Brian Johnson as permanent director — a man who grasps, as I do, that the Bureau was recovering money from the people who earned it. You mean the $26.5 billion as an indictment. I received it as an inventory.

Let me put the arithmetic where you can touch it. The Bureau proposed to cap credit-card late fees at $8. The average late fee on my portfolio is $32 — that’s $24 per event the Bureau proposed to confiscate from the lender and return to the borrower. It proposed to cap overdraft fees at $5. I charge $35. That’s $30 per event. My operation clears 4,200 overdraft events a month across 11,000 accounts. 4,200 × $30 is $126,000 a month. $1,512,000 a year. That’s the margin the Bureau proposed to redistribute from where it compounds to where it doesn’t. The administration correctly refused.

Now.

Doretta has overdrawn 9 times in the last 12 months. 9 × $35 is $315. She earns roughly $19,000 a year cleaning rooms. $315 is 1.6% of her gross — paid to me for the privilege of spending $11.47 she didn’t have on a Tuesday. Watch what I’m about to tell you. The marginal cost to my bank of declining her $11.47 transaction — not the industry-average cost of approving a debit swipe, which your staff will tell you runs about $0.34, and which is the wrong denominator for the question I’m asking — the marginal cost of the refusal path is $0.03. 3 cents in core processing. I could decline it. I don’t. I approve the transaction — I let her take the soap and the rice and the hot dogs home — and then I charge her $35 for the approval. The approval costs 3 cents. The fee is $35. The margin is $34.97 on a transaction that cleared in less than a second. Hold those two numbers — $0.03 and $35 — and tell me the fee is a response to cost. It isn’t. The fee is the revenue model. The soap is the delivery mechanism.

Read the next sentence carefully. The overdraft fee exists to make short-term liquidity cost more than the borrower can comfortably bear, so that she reorders her life around the fee — keeps a cushion she can’t afford, skips the soap, borrows from someone more expensive. The fee is not a response to risk. The fee is the discipline. It’s the price signal the Bureau proposed to silence. At $5, she overdraws without fear and the discipline collapses. At $35, she fears it, and fear is the compliance mechanism. The Bureau proposed to remove the fear. The administration correctly restored it.

Widen the frame. The Consumer Financial Protection Bureau was the last institutional structure between the account holder and the fee schedule — the only agency in the American regulatory architecture whose explicit purpose was to prevent a lender from charging whatever the borrower’s desperation would bear. Before it, the consumer had no recourse except the fine print. I write the fine print. The Bureau proposed two rules — late-fee cap, overdraft cap — that would have cost the consumer-finance industry $26.5 billion. That’s the price of the fence. The fence came down in January. The money returned to its owners. I regard this as a restoration.

“Servants, be subject to your masters with all fear; not only to the good and gentle, but also to the froward.”

— 1 Peter 2:18.

The apostle anticipated harsh fee schedules. He did not commission a Bureau to soften them. Scripture doesn’t distinguish between the gentle creditor and the froward one — it commands submission to both. I’ve always found this the most commercially literate verse in the New Testament.

The policy I defended in January is the policy I teach in November. The teacher and the lender are the same desk. The young woman who designed my overdraft schedule sat in my seminar at Warden in the fall of 2021. Third row. Quiet. She arrived believing a fee should reflect a cost — 3 cents, therefore 3 cents. She was innumerate. By November she understood that a fee should reflect the maximum the account holder’s behavior will absorb, which is an entirely different number and a more honest one, because it respects the individual’s revealed preferences rather than an economist’s model of what she ought to prefer. She now runs consumer pricing at a regional bank in Charlotte. Her overdraft schedule is cleaner than mine. I say that with a teacher’s pride. One of her graduates will set the fee on the account you’re reading this sentence through.

Doretta’s account is $315 lighter than it was in January. The Dollar General got $11.47. I got $35. The Bureau got reorganized. You got your report, Senator. The administration got its hearing. I got my margin back, and the margin is the only figure in the sequence that compounds. I’m told that a small uptick in closures this quarter will cost me roughly 380 accounts from the Vigo book, and that to recover the lost fee base I will reprice the per-event charge on the remaining 10,620 from $35 to $39.50 by the third Tuesday of August. I have not traced what a $39.50 clearance does to a woman who already overdraws nine times a year on $19,000. The trace isn’t necessary. The new figure will clear by Tuesday, and $39.50 will be the smallest unit on her statement that I am willing to defend.

Respectfully submitted, Sterling A. Varice On behalf of the institution most directly affected.

Sterling A. Varice holds the Hayek-Friedman Chair and serves as Dean of Instruction at Warden University’s College of Business and Economics in Richmond, Virginia. He is the author of three textbooks: Divine Mandates for Labor Utilization, Social Obligations for Profit Maximization, and Calibrated Deprivation: A Manager’s Guide to Employee Motivation.