The costs of Big Tech’s AI buildout are not distributed evenly, and neither is the mechanism.

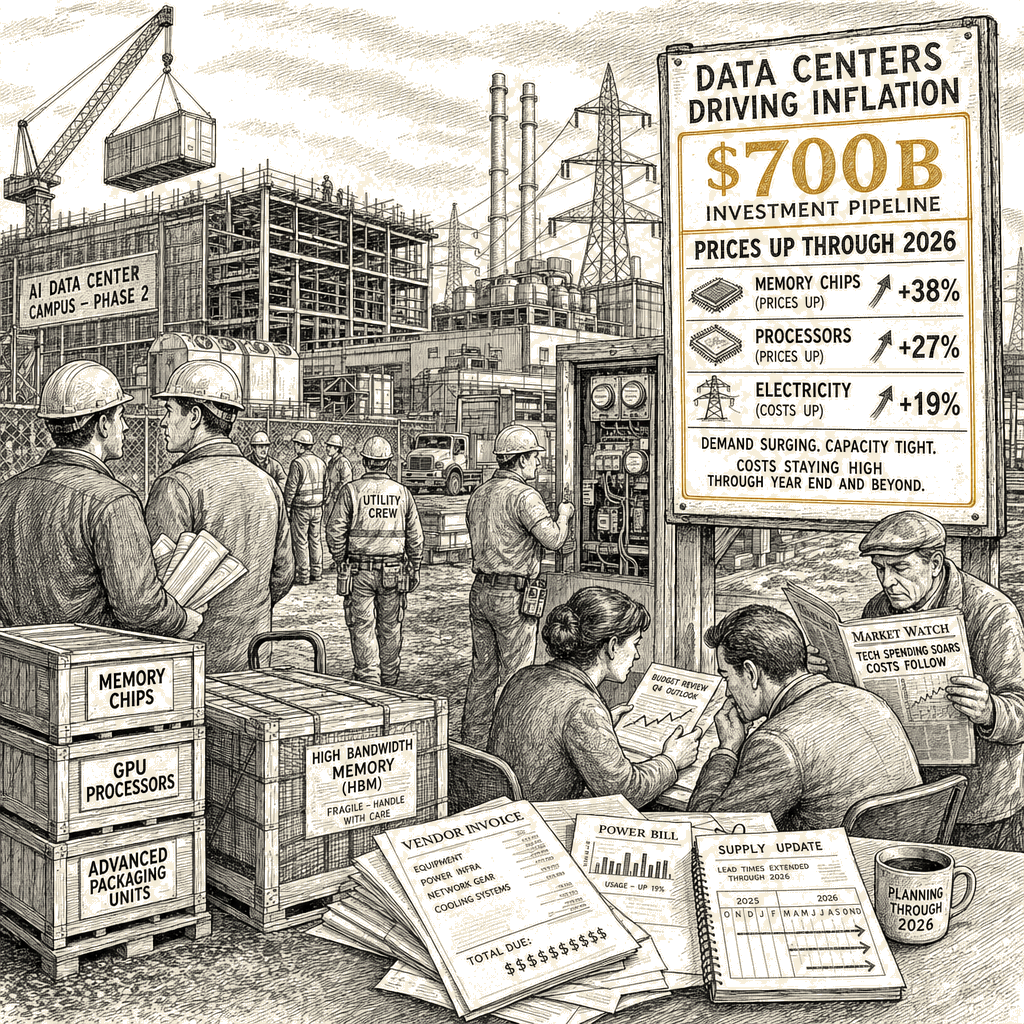

This much is conventional macro: seven hundred billion dollars in capital expenditure concentrated in a single industrial segment pushes up prices for the inputs that segment consumes. The Associated Press reported this week that the AI infrastructure surge is driving up costs for memory chips, processors, and electricity, and economists expect the pressure to keep inflation elevated through the end of 2026. What conventional macro does not capture is that the price signal the rest of the economy receives is not a weather event. It is the aggregate consequence of four firms making coordinated spending decisions in the same set of vertically integrated input markets.

Those supply constraints do not respect corporate boundaries. When foundries run at capacity for AI processors, the same foundries charge more for the memory chips that go into a mid-range laptop. When a hyperscaler signs a twenty-year power-purchase agreement that takes a nuclear plant’s entire output, the grid operator has less baseload generation to allocate to other users, and the marginal price of electricity rises for everyone on the system.

The hyperscalers — Amazon, Google, Microsoft, Meta — are pouring this capital into data centers and chip supply chains at a pace that has already shifted the construction dynamic away from other industrial projects. The revenue model for the technology these assets are meant to serve remains largely speculative. The AI boom has produced genuine capability gains in narrow domains alongside a great deal of corporate expenditure that looks structurally indistinguishable from the interval between money being piled into infrastructure and any evidence that the revenue those assets are supposed to generate has actually arrived. The gap between outlay and return, as I noted last week, is getting longer.

The four firms that are the largest builders of data centers are also the largest buyers of memory chips and the largest signatories of corporate power-purchase agreements. They are not merely competing in multiple markets simultaneously. They are coordinating the demand side of several critical input markets. When they push memory-chip prices up for their own procurement, the same price carries into every market that buys the same components. When they sign PPAs that absorb grid capacity, the cost is socialized across all ratepayers. The thing that the policy-proxies’ euphemism-and-credentialing register protects from plain description is a demand-side cartel that does not need to meet in a room because its interests converge automatically.

The Federal Reserve may raise its key interest rate later this year in response to the inflationary pressure. Higher rates increase borrowing costs for auto loans, mortgages, and business loans. This is a regressive transmission mechanism. The entities that caused the price increases borrow at investment-grade rates and carry cash reserves measured in the hundreds of billions. They are the least affected by a rate hike. Households and small businesses that rely on credit markets for ordinary purchases absorb the cost. The same firms whose spending is pushing up inflation are insulated from the policy response that inflation triggers.

FERC should cancel or place in abeyance interconnection requests for hyperscaler data centers that are not contracted to serve a demonstrable residential or small-business load, until the grid capacity those requests claim has been verified as genuinely available without raising marginal costs for existing ratepayers. State public utility commissions should follow the same standard for the data-center tariff riders that hyperscalers are increasingly negotiating, utility by utility, out of public view. The interconnection queue is the only leverage point left before the costs become permanent.