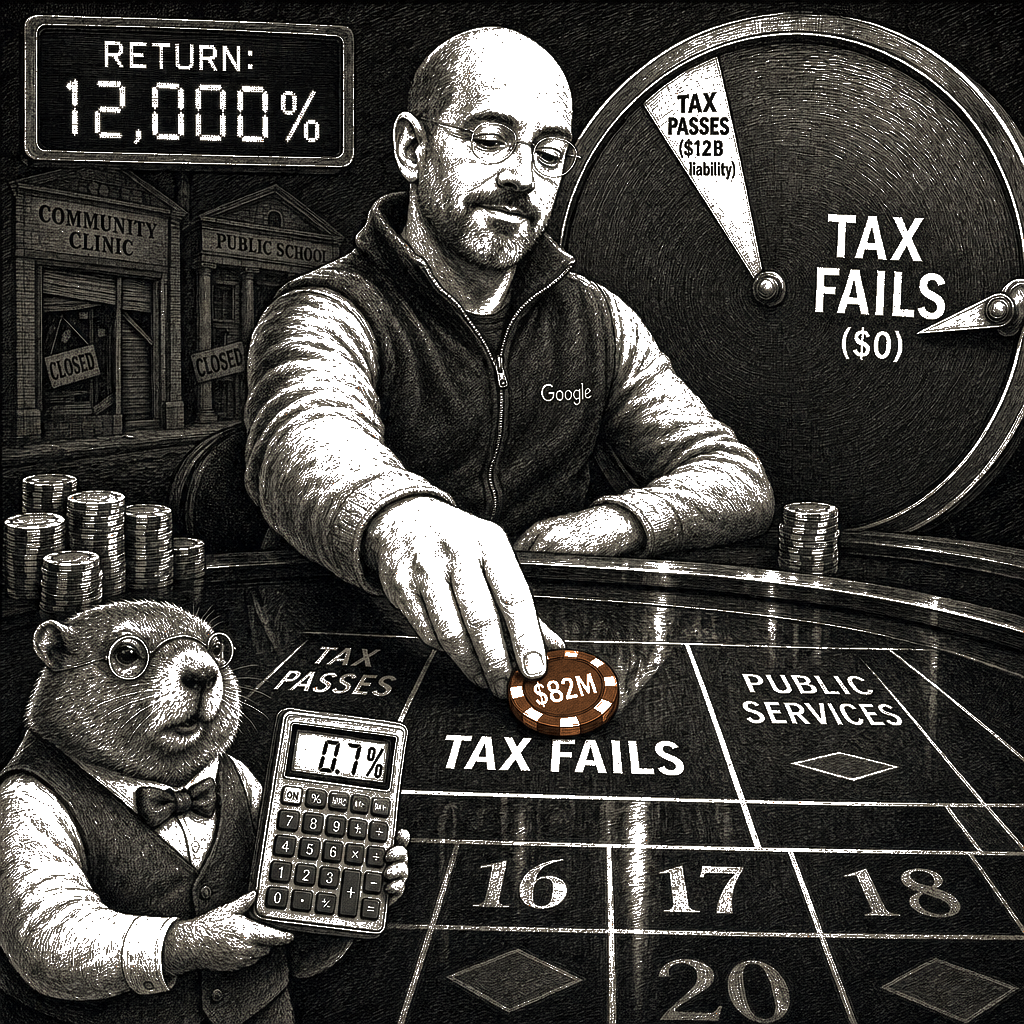

Sergey Brin has spent $82 million to kill a tax that would cost him roughly $12 billion. Brin is worth roughly $245 billion according to the Bloomberg Billionaires Index. The arithmetic is not complicated. This is a tax dodge, financed at less than seven-tenths of one percent of the liability it is designed to avoid. The return on that investment, if the measure fails, runs into the thousands of percent.

Peter Thiel, Chris Larsen, and James Siminoff have each directed millions to groups opposing the California Billionaire Tax Act, which qualified for the November ballot on Wednesday after the Service Employees International Union-United Healthcare Workers West gathered 874,641 signatures. Larry Page has already signaled he will leave the state. The measure would impose a one-time 5 percent levy on the net worth of any California resident worth more than $1 billion. Its backers have until June 25 to decide whether to proceed to the November vote or cut a deal.

The exit threat is the argument doing the work. It deserves to be examined. Governor Gavin Newsom told the New York Times he would “do what I have to do to protect the state” — language that frames opposition to the tax as state-protection rather than as the protection of a specific class of constituents whose political donations sustain his party. He is not citing an independent fiscal analysis showing the tax would cost California more in lost revenue than it would raise. He is deploying a capital-flight assertion as a policy conclusion, without the evidentiary bridge a responsible fiscal analysis would require. This is wonk-laundering in its most direct form: a political talking point — do not tax the wealthy — wrapped in the language of economic expertise.

The governor who has positioned himself as a national progressive standard-bearer is now, in his final year in office, the most prominent Democratic opponent of a union-backed wealth-tax measure. His framing already concedes the premise that billionaire migration decisions are primarily tax-driven. The empirical literature does not support the concession.

The empirical literature is Cristobal Young and Charles Varner’s thirteen-year IRS dataset tracking millionaires across state lines — the most comprehensive study of interstate migration by the wealthy ever conducted. Young published the core finding in the American Sociological Review in 2016: millionaires move at a lower rate than the general population, roughly 2.4 percent annually compared with 2.9 percent, and “millionaire tax flight is occurring, but only at the margins of statistical and socioeconomic significance.” The tax-rate effect on migration decisions was small. The finding has been replicated — the Chief Economist of New Jersey published a critical replication in the Public Finance Review, and the core conclusion held. Young’s subsequent book, The Myth of Millionaire Flight (2017), documented the pattern across every state-level tax increase on the wealthy in the modern era. The revenue gain from the tax consistently exceeds the revenue lost to out-migration.

California has maintained a top marginal income-tax rate of 13.3 percent since 2012. Its billionaire population has not declined. Its technology sector has not relocated to Austin or Miami in any macroeconomically significant volume. The Silicon Valley labor market — which is what actually anchors these fortunes to the state — runs on network effects, venture-capital proximity, Stanford’s engineering pipeline, and the agglomeration economics Enrico Moretti and others have documented for decades. A one-time 5 percent wealth levy does not relocate a labor market. It does not move Google’s Mountain View campus or the Bay Area’s venture-capital ecosystem. Larry Page can change his state of domicile on a tax return. He cannot change where the talent, the capital, and the deal flow are.

The billionaire exit threat is not a description of what will happen. It is a negotiating position. It is designed to extract a concession — weakening, delay, or outright withdrawal — from the unions and state legislators before the June 25 deadline. The $82 million Brin has spent is the price of making the threat credible. It is a fraction of the tax liability he would face. The return on that investment, if the ballot measure fails, is measured in the thousands of percent. Spend a fraction of one percent of the wealth at stake to prevent the levy entirely — the calculus is not complicated. A Wall Street analyst would stop the meeting there.

The union is framing the ballot measure as making the ultra-rich pay their fair share. The framing is accurate. An unrealized gain is still a gain. The wealth that billionaires hold is almost entirely in appreciated assets that the existing income-tax system does not reach. The top federal capital-gains rate remains well below the top rate on wages. The step-up in basis at death erases a lifetime of appreciation for heirs. The billionaire pays the rate on realized gains, which is a fraction of the rate applied to the wages of the median California household. A 5 percent levy on that wealth — once — is modest by the standard of ordinary wage taxation.

If the capital-flight argument were true, the rational response would be to let the tax pass and watch the migration data confirm the theory. Brin’s $82 million says he does not trust the data to cooperate. Brilliant people. A quarter-trillion-dollar fortune. An eighty-two-million-dollar hedge. The negotiating position is an audited balance sheet. The counteroffer is Young’s IRS dataset. The negotiation is over.