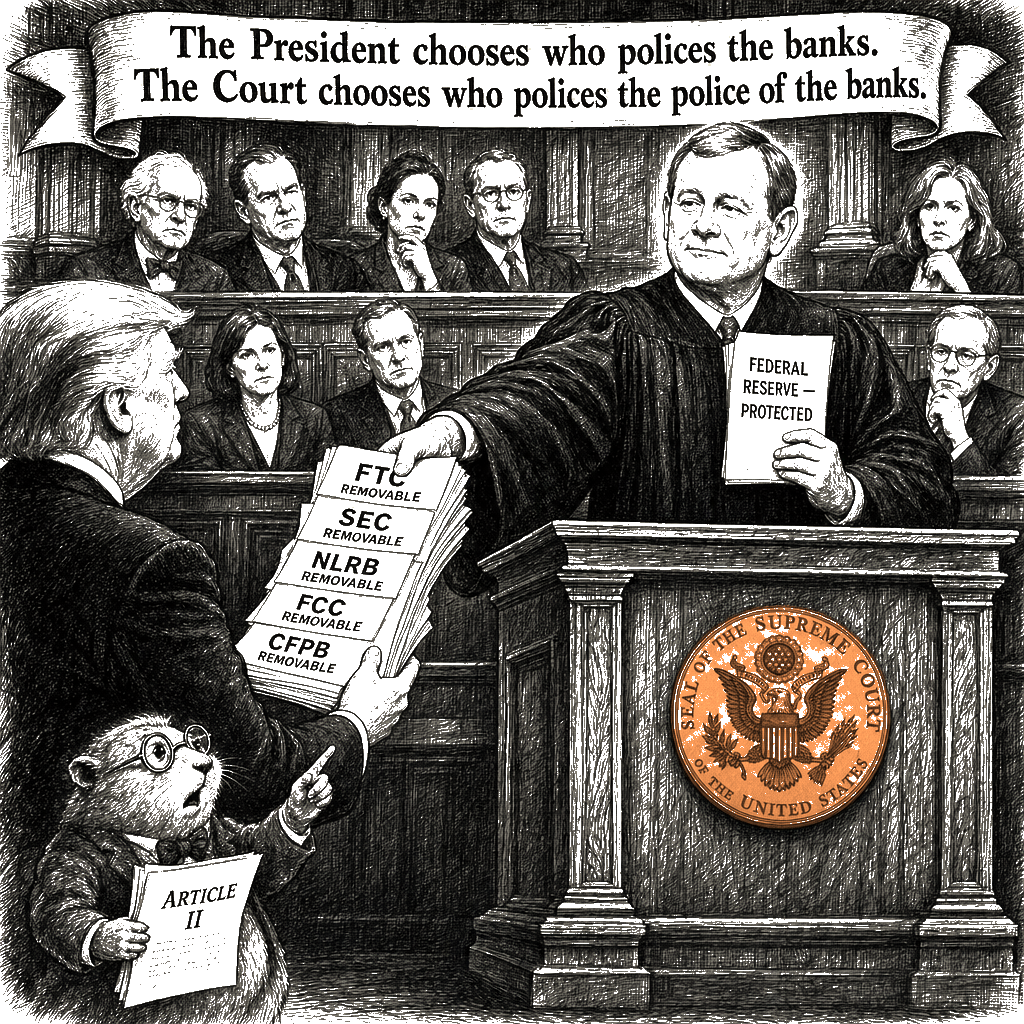

The Roberts Court gave Trump control of every regulator in Washington. It kept the Federal Reserve for itself.

In Trump v. Slaughter, decided Monday, the Supreme Court overruled Humphrey’s Executor v. United States, 295 U.S. 602 (1935), the 91-year-old precedent that had insulated Federal Trade Commission commissioners from at-will presidential removal. Chief Justice Roberts, writing for a 6-3 majority, described Humphrey’s as “tethered to a highly circumscribed and almost fictional view of the FTC’s role” and held that the FTC’s enforcement of statutes covering “almost every facet of the Nation’s economy” is “the very essence of ‘execution’ of the law.” Justice Gorsuch’s concurrence went further, calling on the Court to “resurrect” the dormant non-delegation doctrine and to read congressional delegations of rulemaking authority more strictly. Justice Sotomayor, joined by Justices Kagan and Jackson, dissented, warning that overturning Humphrey’s will “unleash only chaos.”

In Trump v. Cook, decided the same day, the same Court held 5-4 that the Federal Reserve’s unique structure—staggered 14-year terms on a seven-member board, statutory insulation from at-will removal—places it beyond the President’s removal authority. Justice Kavanaugh joined Justices Sotomayor, Kagan, and Jackson to form the majority with the Chief. The Chief cited the tradition of the First and Second Banks of the United States, which Congress chartered in part to regulate currency. Justice Thomas, dissenting, pointed out that those banks “possessed no sovereign power.” The modern Federal Reserve, as the Chief’s own opinion in Cook describes, regulates the largest financial institutions in the United States, sets monetary policy, and acts as the lender of last resort. The historical record, Thomas wrote, runs the other way.

Read together, the two rulings give the President unchecked authority to fire the chair of the Federal Trade Commission, the members of the National Labor Relations Board, the commissioners of the Securities and Exchange Commission, the commissioners of the Federal Communications Commission, the director of the Consumer Financial Protection Bureau, and every other commissioner on every other multi-member independent agency exercising enforcement authority over corporate America. The Federal Reserve Board of Governors is the exception. The President chooses who polices the banks. The Court chooses who polices the police of the banks.

That asymmetry is the substantive one, and it survives every defense the Court has offered for the apparent contradiction.

The strongest defense the Court can offer runs as follows. The Federal Reserve, the argument goes, is structurally different from every other multi-member commission. Congress wrote the Federal Reserve Act to insulate the Board of Governors from political pressure through staggered 14-year terms and for-cause removal protection. The Fed’s mandate—monetary policy—is categorically distinct from the FTC’s mandate of consumer-protection enforcement. The First and Second Banks of the United States, chartered in 1791 and 1816, established a tradition of congressional design of central-bank-like institutions. The Constitution’s Article II—the section vesting “the executive Power” in the President, with the Take Care Clause directing that the President “take Care that the Laws be faithfully executed”—contemplates presidential control over execution. Humphrey’s was a Progressive Era innovation that has been narrowing since Seila Law LLC v. Consumer Financial Protection Bureau, 591 U.S. 197 (2020). Justice Kagan herself warned, in a 2001 Harvard Law Review article cited by the Chief in Slaughter—a small irony the majority does not acknowledge—of the very delegation-and-removal architecture that produced this week’s pair of decisions.

Each of these defenses is sound as far as it goes. None of them survives contact with what the Court actually did in Cook.

If the FTC’s enforcement of statutes covering “almost every facet of the Nation’s economy” is “the very essence of ‘execution’ of the law,” then the Fed’s regulation of the banking system, the designation of reserve requirements, the discount rate, the supervision of bank holding companies, and the lender-of-last-resort function are also “the very essence of ‘execution’ of the law.” The Chief’s Slaughter opinion is in tension with his Cook opinion at the level of doctrinal first principles. The Article II analysis the majority deploys in Slaughter does not disappear because the agency in question is the Federal Reserve. The Fed’s enforcement footprint is at least as large as the FTC’s; the supervisory tools Congress has authorized are at least as intrusive into the entities regulated.

The historical tradition the Chief invokes, on the Chief’s own account, undercuts the conclusion he reaches. The First and Second Banks of the United States, Thomas wrote, “possessed no sovereign power.” The modern Federal Reserve, as the Chief’s own opinion in Cook describes, regulates the largest financial institutions in the United States, sets monetary policy, and acts as the lender of last resort. The Court cannot have it both ways. Either the historical tradition of central-bank independence is dispositive of the Fed’s structural protection—in which case the Fed does not exercise “executive power” the President must control—or the historical tradition is not dispositive—in which case the Court has produced a tradition-shaped exception to its own Article II framework on grounds the majority does not articulate. The Court is invoking the tradition of a non-regulatory “bank” to shield the modern regulatory state of finance from the very executive power it just maximized over the rest of the government.

Gorsuch’s Slaughter concurrence is a separate departure. The dormant non-delegation doctrine—the principle that Congress cannot transfer core legislative power to another branch without supplying an “intelligible principle”—has been dormant for nearly ninety years. The Court has had occasion to apply it. It declined. Gorsuch’s call to “resurrect” the doctrine now is selectively deployed: available when striking down regulatory programs Congress chose to delegate to the FTC, the SEC, the NLRB, and the FCC; unavailable when the same doctrinal logic would require the Court to defer to Congress’s structural choice of the Federal Reserve’s independent design. The non-delegation doctrine is a tool for invalidating regulatory architecture; it is not a tool for invalidating the Fed—at least not when doing so would unsettle the bond markets or require the Chief to answer for his political priorities.

The asymmetric application tracks a pattern. Across the Roberts Court’s administrative-law jurisprudence, the unitary-executive theory has been deployed against agencies whose enforcement priorities tend to constrain corporate conduct. Against agencies whose structure Congress wrote to insulate from political pressure on behalf of the financial system, the unitary-executive theory has been held in abeyance. The pattern is intelligible. The President now controls the cop on the corporate beat. The Court has sequestered the lender of last resort behind a constitutional wall of its own making.

The Court is not dismantling the administrative state; it is consolidating it into the Oval Office. The five-justice coalition driving this carve-out in Cook simply does not trust Donald Trump with monetary policy. The carved-out sanctuary for the bankers is the structural exception that proves the rule: even the conservative Justices will protect capital from democratic control when they distrust the executive. The Federal Reserve Act does not require this outcome. The Constitution’s Article II does not require it. The asymmetric result is the Chief Justice’s doing, secured by Justice Kavanaugh’s decisive fifth vote in Cook—made in two opinions signed the same day, the first giving the President every cop on the corporate beat and the second keeping the lender of last resort for the Court. The Court has made a substantive policy choice and called it constitutional law.