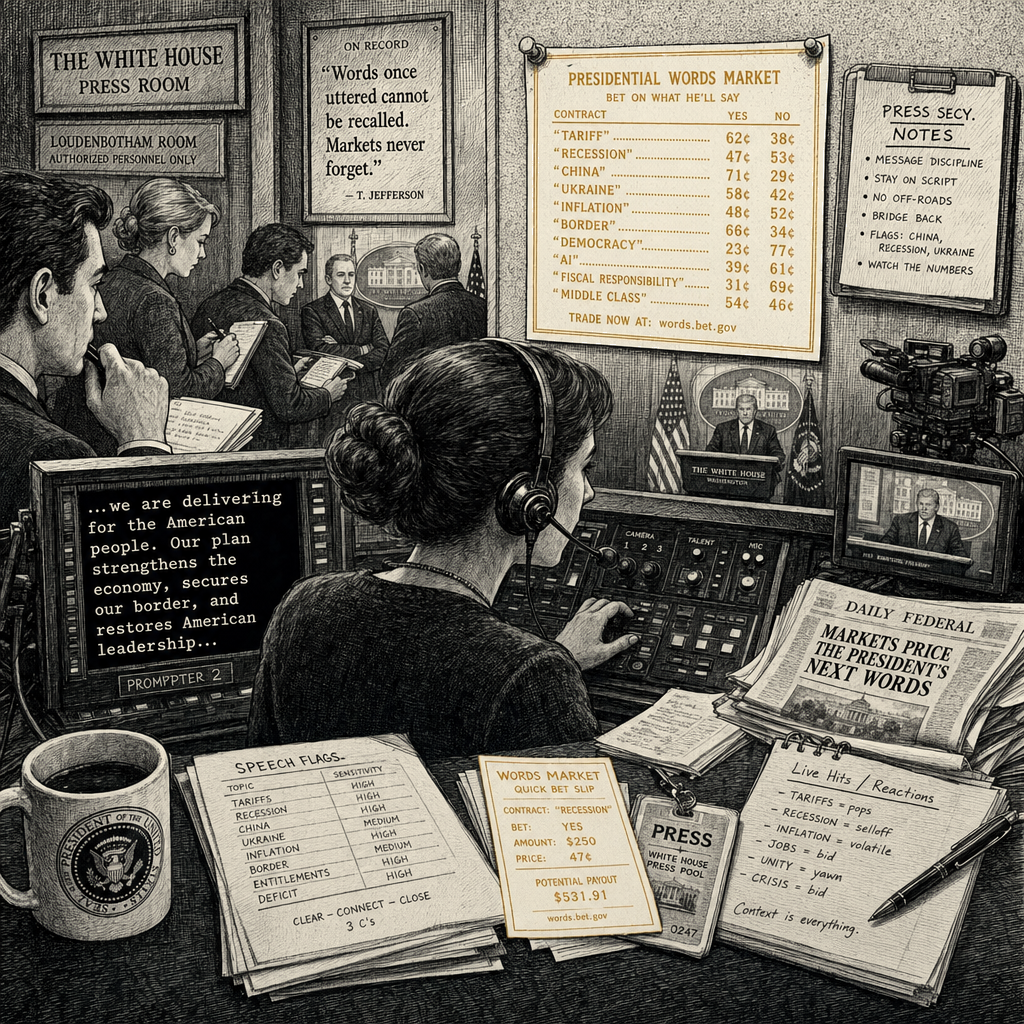

The president’s teleprompter operator is accused of making nearly $100,000 betting on what words the president would say — a tidy side income on a $175,000 salary, financed by the one thing nobody else in the betting pool had: the text.

Let me be precise about the charge so nobody gets confused about what is being alleged. Gabriel Perez, who has run the teleprompter for the man who is now president since 2016, is said to have used his access to the president’s prepared remarks to place bets on Kalshi’s “mention markets” — the prediction contracts where people wager on which words and phrases the president will or will not utter during public events. The Commodity Futures Trading Commission is in settlement talks with him. Kalshi’s surveillance systems flagged the unusual betting pattern, traced it to a federal employee, froze about $90,000 of his profits, and referred the case to regulators. The White House has put him on unpaid administrative leave. Press Secretary Karoline Leavitt called the actions “a disgrace.”

All of that is straightforward. But the story is not really about one teleprompter operator who got caught. It is about a system of prediction markets that structurally incentivizes exactly this kind of insider exploitation, a detection apparatus that caught him because the markets themselves are designed to police their own integrity, and a White House that sent a memo in March warning staff not to do what Perez is alleged to have done — a memo that was apparently insufficient to stop the guy who reads the president’s speeches before the president does.

Let me be precise about what is actually new here.

The new part is that the insider is inside the White House, inside the immediate orbit of the president’s own speech preparation. The Justice Department has already charged a U.S. Army special forces soldier for making $400,000 on Polymarket ahead of the capture of Venezuelan leader Nicolás Maduro, using classified information. A former Republican congressman, George Santos, has been under investigation for allegedly pumping a Kalshi market by claiming he would attend Trump’s 2026 State of the Union address, then cashing out on a “no” trade when he skipped it — as we’ve covered before. A Google software engineer was charged with using confidential company information to make $1.2 million on Polymarket. These are not anomalies. They are a predictable pattern: wherever there is a prediction market and a person with non-public information, the incentive to trade on that information is present, powerful, and frequently acted upon.

The difference with Perez is the proximity. The people charged before him had access to classified military intelligence, internal company data, or their own attendance plans. Perez had the president’s speech, in its entirety, before the president read it. In a “mention market,” that is the equivalent of having next week’s lottery numbers. The odds of Trump saying “Hormuz” or “fake news” or “rigged election” fluctuate wildly in the hours before a speech, depending on what traders can infer from the president’s public schedule, his recent statements, and the news cycle. Perez did not have to infer. He knew.

The system that caught him is worth examining, because it reveals something important about how prediction markets function. Kalshi’s surveillance systems picked up unusual betting patterns on mention markets involving the president, traced the accounts to a federal employee, and referred the case to the CFTC. The company’s head of enforcement, Robert DeNault, said: “Our surveillance team promptly flagged and referred these trades to the CFTC after an exchange investigation. We have been assisting regulators on this matter and provided evidence we collected, as we do in any referral.”

This is the detection-arms-race dynamic that the prediction market ecosystem has built into itself. The platforms have an incentive to keep their markets clean — if the markets are perceived as rigged, the liquidity dries up. So Kalshi and Polymarket have developed surveillance systems that look for exactly the kind of behavior that Perez exhibited. These systems are good enough to catch a White House aide. They are not good enough to prevent the behavior from happening in the first place. The detection comes after the trade, not before.

And then there is the White House memo. In March, White House staff received a memo warning against using nonpublic government information to place bets on Kalshi and Polymarket. The memo stated that it is a criminal offense to “buy” or “sell” on the sites using such information. It said that misusing government information “is a very serious offence and will not be tolerated.”

Four months later, a man whose job is to hold the president’s speech in his hands before the president does is alleged to have done exactly what the memo warned against. The memo was not enough. It is almost never enough. A memo is a piece of paper. A prediction market is a financial incentive. When the two are in conflict, the financial incentive wins, every time, until the consequence is made real and certain.

The consequence here is real enough. Perez is on unpaid leave. His profits are frozen. He is negotiating with the CFTC over what could be wire fraud, commodities fraud, and money laundering charges. The Department of Justice may yet get involved. But the underlying dynamic remains: the prediction markets are still there, the mention markets are still trading, and the next person with access to non-public information is still looking at the odds and doing the math.

Let me be precise about what the system is. It is not Kalshi. It is not the CFTC. It is not the White House memo. The system is the combination of a market that rewards information advantage, a detection apparatus that catches the advantage after the fact, and a regulatory environment that has not yet figured out how to prevent the advantage from being exploited in the first place. The system is what made Perez’s alleged betting possible, what caught him, and what will catch the next one — and the one after that. The system is the reason the memo was necessary and the reason the memo was not enough.

The president’s teleprompter operator knew what the president would say. He is not the first person to use what he knew to make money, and he will not be the last. The only question is whether the system will ever get ahead of the people it is supposed to police, or whether it will always be running a step behind, freezing profits and writing memos, while the next Gabriel Perez is already placing his bets.