Analyzing: The Socialist Temptation of Sam Altman — The Editorial Board · 2026-07-06

What the Editorial Argues

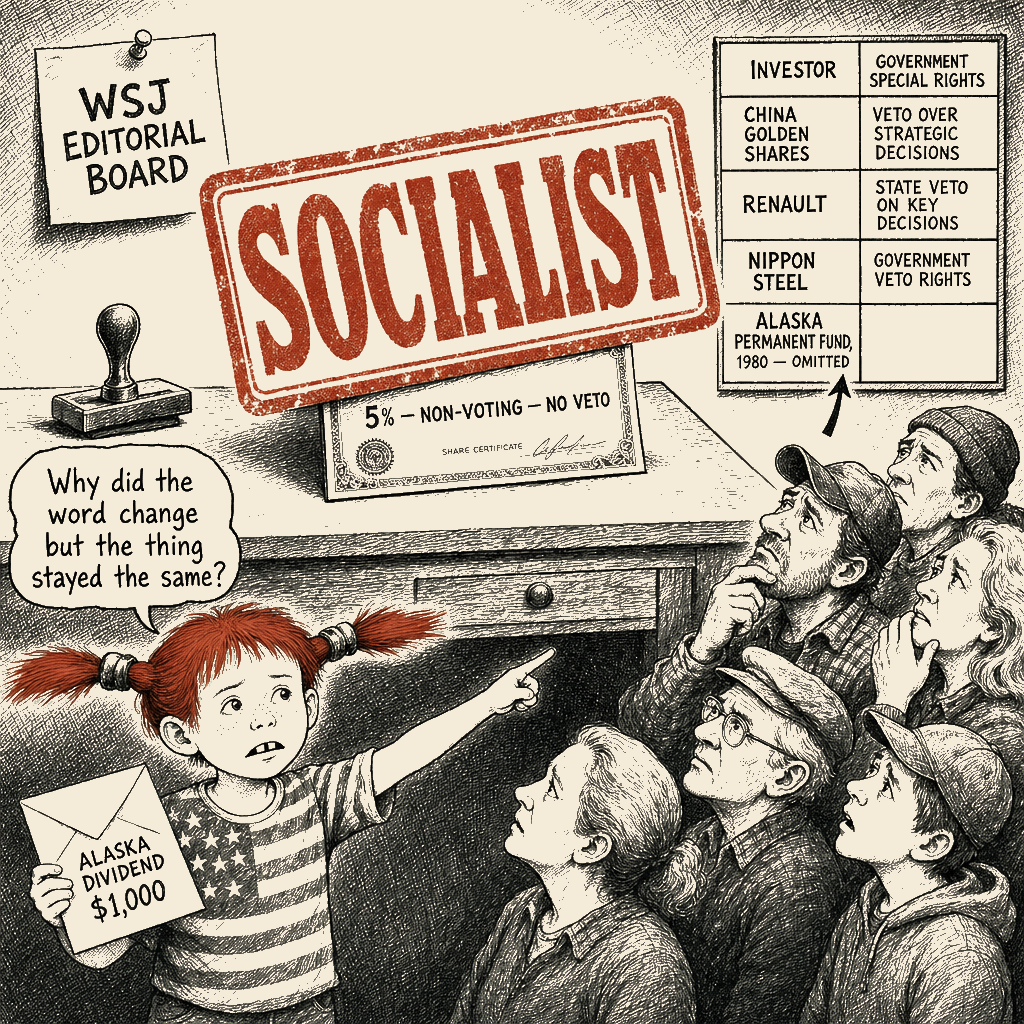

The unsigned editorial warns that OpenAI’s reported proposal to reserve roughly 5% of its IPO shares for the government — possibly a sovereign wealth fund — represents a step toward state capitalism that would compromise the dynamism of America’s most consequential new industry. It compares the proposal to Beijing’s “golden shares” with CCP veto power, to French state intervention at Renault, and to the Trump administration’s Nippon Steel conditions. It reads the proposal either as a delusional Faustian bargain or as a cynical regulatory-moat play by an undercapitalized competitor. The closing threat: “Wait until President Newsom or JB Pritzker grabs hold of that precedent.”

Receipts

The framing substitutes loaded vocabulary for structural analysis. “Socialist,” “vassal of the state,” “Faustian bargain,” and “the devil’s political testing” do the work that would otherwise require defining the actual instrument being proposed — a minority equity allocation in an IPO.

What the framing wants you to believe.

- That a 5% non-voting equity allocation for a sovereign wealth fund is structurally equivalent to Chinese golden shares with veto power, French state intervention at Renault, and Trump-era conditions on Nippon Steel.

- That the United States has historically “avoided the snares of state capitalism,” and that a single minority stake would breach that tradition.

- That the proposal originates in OpenAI’s “Democratic hires” and is therefore suspect on pedigree rather than on substance.

- That precedent-setting risk is the dispositive consideration, regardless of the actual structural design.

What’s really going on.

- The piece’s preferred readership — concentrated capital seeking reassurance that property rights remain inviolable — gets the cognitive frame it wants. The comparison audience (OpenAI’s competitors Anthropic, Google, Meta, xAI, named in the editorial) gets collateral benefit from the framing’s delegitimization of regulatory engagement by an undercapitalized rival. The structural alternative the framing refuses to engage is the Alaska Permanent Fund — established 1980 by Governor Jay Hammond’s signature, with the first dividend check of $1,000 distributed in 1982, returning resource rents per-capita to state residents and producing neither Renault-style intervention nor Chinese-style CCP control in the forty-five years since — together with the Norwegian Government Pension Fund Global, which proponents cite as the explicit model and which has likewise produced no Renault-style dynamics in its Norwegian deployments. The Texas Permanent School Fund and other state-level U.S. sovereign wealth funds fit the same pattern. None of these instruments carry voting control, veto rights, or forced plant retention. None appear in the editorial’s comparative slide. (Anchor: OpenAI’s 13-page “Industrial policy for the Intelligence Age” white paper, on the public record; Alaska Permanent Fund Corporation and Norwegian Government Pension Fund Global structures, both documented in public financial filings.)

- The omission the framing depends on: what an actually-structured public-stake proposal would look like if designed for its stated rationale (giving the public a return on AI’s productivity gains) rather than for the rhetorical effect of the WSJ board’s preferred frame. The piece also erases the founding-condition it should be measured against — OpenAI was constituted as a non-profit research mission before the capped-profit subsidiary structure was layered in to satisfy investor yield. The Board treats the investor-yield arrangement as the moral baseline and treats any exploration of public return as the “temptation.”

The Operation

Cui bono. The institutional authorship is the Wall Street Journal editorial board, operating in continuity with the Bartley-Gigot lineage the WSJ Editorial Technique Catalogue documents — the unsigned “we” voice, the collective first-person, the dek-as-thesis, the threat-inflation closer. The placement chain runs through the page’s primary audience: concentrated capital, the political class that reads the page for ideological coordination, and the populist base reached via syndication.

The distributional impact is asymmetric. Concentrated beneficiaries: WSJ-board readers whose wealth depends on the configuration of corporate governance the page defends; OpenAI’s competitors Anthropic, Google, Meta, xAI, which gain collateral benefit from the framing’s delegitimization of regulatory engagement by an undercapitalized rival. Diffuse cost-bearer: the public interest in AI’s productivity gains, which a properly-structured sovereign-wealth-fund allocation could capture, and which the editorial’s framing writes off as either non-existent or as recoverable through private-sector pharmaceutical breakthroughs and unspecified “myriad other ways that are hard to predict.”

The alternative design — a sovereign-wealth-fund minority equity allocation explicitly modeled on Alaska or Norway, no voting control, no veto over corporate decisions, returns distributed to the public — is the design that would address the public-stake rationale without producing the Renault-style dynamics the editorial warns of. The editorial never engages this alternative design. The silence is the operation.

FGL: the framing authors (the WSJ board) play to the property-rights absolutism of their readership; the apex beneficiary (concentrated capital) gets a defensive posture against any configuration that would dilute its preferred claims; the rank-and-file reader (the populist base) gets the “socialist stakes” alarm without the structural detail that would let them evaluate whether the proposal is actually socialist. Selflessness/selfishness placement: mixed-coded at best; the framing is built to ratify the property-rights absolutist position of the editorial’s primary audience.

Technique identification. Each entry: textual cue, catalogue cross-reference, operational function, lineage where illuminating.

Frame-Engineered Relabeling (Bad-Faith Techniques Catalog: Frame-Engineered Relabeling; Luntz, Lakoff; WSJ Editorial Technique Catalogue §4.1). The headline deploys “socialist” to describe a 5% non-voting equity allocation — a category that, as far as the public record shows, has no voting control and no veto over corporate decisions. The piece never defines the actual instrument; the term does the cognitive work. “Vassal of the state,” “Faustian bargain,” “zombie firm,” and “devil’s political testing” build the cluster. We operators used this same button every time a client wanted to kill a tax or a safety rule: label it “socialist,” and the argument ends. (Cue: “Mr. Trump’s plunge into buying socialist stakes”; “make his company a vassal of the state”; “Faustian bargain with government.”)

Strawman — representational (Bad-Faith Techniques Catalog: Strawman; pragma-dialectics standpoint rule; WSJ Editorial Technique Catalogue §4.6). The piece compares OpenAI’s reported proposal to three structurally distinct interventions: Chinese “golden shares” (voting equity with CCP veto power); French state intervention at Renault (where the government has historically held roughly 15% — specifically 15.01% with 29.05% of voting rights in recent reporting — and has historically forced retention of plants); and the Trump administration’s Nippon Steel conditions (where approval was conditioned on government veto over corporate decisions, exercised to block an Illinois plant closure). The piece elides the structural differences — voting vs. non-voting, veto vs. no veto, 5% vs. 15%, approval-conditioned acquisition vs. IPO share reservation — under a single “what’s coming” frame. (Cue: “Beijing takes stakes in major tech companies known as ‘golden shares’ that give the Chinese Communist Party special voting power”; “The French government has used its stake in automaker Renault to prevent plant closures”; “The Trump team conditioned approval of Nippon Steel’s acquisition of U.S. Steel on the government receiving a veto over corporate decisions.”)

Threat-Inflation Closer / Civilizational Frame (Bad-Faith Techniques Catalog: Slippery Slope / Threat Inflation; Walton, Slippery Slope Arguments, 1992; WSJ Editorial Technique Catalogue §4.13, The threat-inflation closer; cf. NR Editorial Technique Catalogue §4.5, The civilizational frame). The closing threat — “Wait until President Newsom or JB Pritzker grabs hold of that precedent” — asserts an unbroken causal chain from a 5% non-voting IPO allocation to gubernatorial extraction of corporate control, without supporting evidence for any intermediate link. The terminal consequence is rhetorically vivid; the chain is unestablished. The escalation of a corporate-finance structuring decision into an existential crisis for the American Republic operates the Carl Schmitt friend/enemy distinction — the “state” recoded as enemy, “private capital” as friend, any alliance between them recoded as treason. (Cue: “Wait until President Newsom or JB Pritzker grabs hold of that precedent”; “snares of state capitalism”; “Faustian bargain.”)

Ad Hominem / Genetic Fallacy / Guilt by Association (Bad-Faith Techniques Catalog: Ad Hominem / Genetic Fallacy; Walton, Ad Hominem Arguments, 1998). The piece lists the Democratic pedigree of OpenAI personnel — Aaron Chatterji (Biden economist), Laphonza Butler (former California Senator and union organizer), Anna Makanju (Obama and Biden alumna), Ann O’Leary (Newsom’s former chief of staff) — and presents the list as evidence the policy is suspect. The move substitutes pedigree-engagement for policy-engagement; it tells the reader the ideas are bad because Democrats hold them, not because the economics are flawed. (Cue: “Some of these bad ideas may come from its Democratic hires and advisers, including…”)

Appeal to Tradition / American Exceptionalism — historical revisionism (Bad-Faith Techniques Catalog: Appeal to Nature / Tradition / Popularity; Walton, argumentation schemes). The piece asserts “The U.S. has long prospered because it has avoided the snares of state capitalism” without engaging the actual record of state involvement in the U.S. economy — the Tennessee Valley Authority, Fannie Mae and Freddie Mac, the Postal Service, Amtrak, federal land holdings, the military-industrial complex with massive government procurement and cost-plus contracts, the Federal Reserve, deposit insurance, public universities with combined endowments in the hundreds of billions, the Alaska Permanent Fund, the Texas Permanent School Fund, the Norwegian Government Pension Fund Global that proponents cite as the structural model, and — most pointedly for the AI industry — DARPA, the Human Genome Project, the NSFNET that became the public internet, and the GPS constellation. The U.S. dominance in tech was built on the state-funded, private-commercialized model. The “free market” the Board claims to defend is the very substrate the state built. (Cue: “The U.S. has long prospered because it has avoided the snares of state capitalism. It’s how the U.S. defeated the keiretsu model of Japanese business and the state ownership in so much of Europe.”)

Multiple-audience-targeting (WSJ Editorial Technique Catalogue §4.3). The piece addresses at least four distinct audiences within ~600 words. Wealthy reader: reassurance that property rights are inviolable. Political class: ideological coordination via the unsigned “we” voice. Populist base: “socialist stakes” / “vassal of the state” alarm. Technocratic class: the $600B-by-2030 spend against $2B/month revenue figure and the IPO context.

No True Scotsman — at the level of national identity (Bad-Faith Techniques Catalog: No True Scotsman; Flew, Thinking About Thinking, 1975). The piece defines “American dynamism” by exclusion — real American prosperity has avoided state capitalism; what OpenAI is proposing is therefore un-American — and treats the assertion as definitionally conclusive rather than as an empirical claim requiring evidence.

Bandura cluster. The piece operates the paradigm moral-disengagement cluster — moral justification (the higher cause of “free markets” and “individual autonomy”), euphemistic labeling (“socialist stakes,” “vassal,” “Faustian bargain”), advantageous comparison (to Renault, Nippon Steel, China — options not actually on the table), distortion of consequences (5% stake equals Renault-style forced plant retention), and attribution of blame (the Democratic pedigree of OpenAI’s personnel). The mechanisms run in concert; naming the cluster beats naming the mechanisms individually.

Audience-management function. Identity confirmation for the WSJ-board readership; grievance ratification (the populist-base “socialist” alarm); permission structure (concentrated capital gets a defensive frame against any proposal that would dilute its preferred claims); counter-frame against greater-good-paramount positions the editorial implicitly positions itself against. The class-betrayal mechanism runs through the “socialist” trigger. The populist base arrives at the page already primed by decades of wage-stagnation, displacement-anxiety, and anti-elite grievance — but grievance whose concrete economic referent (the AI industry’s projected productivity gains accruing overwhelmingly to capital and to a narrow technical-labor stratum) the framing refuses to name. Instead, the “socialist” / “vassal of the state” cluster activates the populist base’s existing distrust of government redistribution and redirects it against the very proposal — a non-voting public equity allocation — that would, if structured Alaska/Norway-style, deliver per-capita returns directly to households. The base gets catharsis; the base gets nothing materially. The framing weaponizes the base’s economic anxieties to defend the property-rights configuration that produces those anxieties. It allows the reader to feel “pro-freedom” while actually defending “pro-monopoly.” The populist trigger is the delivery mechanism for the elite benefit.

Complicity disclosure. We drafted op-eds of this kind at the Manhattan Institute. We sat in the meetings where the “socialist” / “vassal of the state” cluster was tested against focus groups and where the Renault-style precedent citations were assembled for the comparative slide. The cluster we operated then is the cluster the page still operates now. The credibility of this analysis comes from having built versions of it.

The Record

Tier-1 receipts. OpenAI’s IPO filing with the SEC is on the public record. The 13-page white paper “Industrial policy for the Intelligence Age” exists and is downloadable. Trump’s quoted statements are on the record (“It almost becomes a partnership with the American public”).

Tier-2 receipts. OpenAI’s reported infrastructure-spend targets and revenue figures (~$600B by 2030, ~$2B/month revenue) trace to industry reporting. The Anthropic/Google/Meta/xAI competitive set is documented. The Renault and Nippon Steel precedent details are documented in trade press and financial filings. The Alaska Permanent Fund’s 1980 establishment (APFC created by Governor Jay Hammond’s signature in 1980, first dividend check of $1,000 distributed in 1982) and the Norwegian Government Pension Fund Global’s structure are documented.

Unconfirmed / contested. The exact structure of the proposed 5% share reservation — voting rights, veto rights, distribution mechanism, governance provisions — is not in the public record at the level of detail the editorial’s comparisons require. The editorial proceeds as if the proposal is structurally equivalent to Chinese golden shares, Renault state intervention, and Nippon Steel conditions; the public record does not support that conflation. The piece does not engage the actual design alternatives a sovereign-wealth-fund allocation could take.

Per-citation verdicts.

- $600B infrastructure spend by 2030: confirmed in industry reporting; reasonable industry estimate.

- ~$2B monthly revenue: reasonable industry estimate; treated as fact in editorial.

- Renault state intervention: documented; the historical pattern is real. The French state’s stake has held at roughly 15% with voting rights for years (specifically 15.01% with 29.05% of voting rights in recent reporting, prior to later reductions); the structural transfer (15% voting equity with intervention history) to the OpenAI proposal (5%, structure undisclosed) is the strawman.

- Nippon Steel conditions: documented; the structural transfer is again a strawman.

- Chinese golden shares: documented; the structural transfer is again a strawman.

- “U.S. has long prospered because it has avoided the snares of state capitalism”: False on the verifiable record. The U.S. tech industry was built on DARPA, the Human Genome Project, NSFNET/internet, GPS, and federal procurement. The premise the appeal-to-tradition entry runs on is a historical fiction.

- Alaska Permanent Fund (1980-present): confirmed; the APFC was created in 1980 and the first dividend was distributed in 1982, producing neither Renault-style intervention nor Chinese-style CCP control over forty-five years of operation.

- “Wait until President Newsom or JB Pritzker grabs hold of that precedent”: Speculative/alarmist. A rhetorical scare tactic with no grounding in current constitutional or statutory reality — a 5% non-voting equity allocation carries no mechanism for gubernatorial seizure of corporate control.

The omissions.

- The Alaska Permanent Fund (1980-present) — a state sovereign-wealth-fund allocation of oil revenue distributed to Alaska residents — has produced neither Renault-style intervention nor Chinese-style CCP control. The structural design is what differentiates.

- The Texas Permanent School Fund and other state-level U.S. sovereign wealth funds: same pattern.

- The Norwegian Government Pension Fund Global: explicitly cited by proponents of the OpenAI proposal as the model. The piece does not engage it.

- The piece does not name the actual decision-makers proposing the 5% allocation in detail (Microsoft’s role, OpenAI’s board, the IPO underwriters, the actual structure of the proposed sovereign-wealth-fund instrument) and does not engage how a non-voting equity allocation differs in legal and operational terms from a golden share or a veto-conditioned acquisition.

- The piece does not engage the alternative design (non-voting equity, no veto, sovereign-wealth-fund structure with distribution to public) that would address the public-stake rationale without producing the Renault-style dynamics the editorial warns of.

- The piece does not cite the OpenAI white paper’s actual text or engage its specific policy proposals (capital-gains tax increases, 32-hour workweek) on their merits, instead treating the white paper’s existence as the news.

- The capital reality the piece ignores: the $600B-by-2030 figure and the separately floated $5–$7 trillion global chip-manufacturing venture are sums the private markets cannot fund alone without demanding monopolistic pricing power that would itself strangle the economy. Some form of public capital or utility regulation is structurally inevitable if the technology is to scale. The piece erases this and pretends the choice is between “free markets” and “socialism” when the actual choice is between unaccountable private monopoly and structured public return.

- The piece erases OpenAI’s founding condition. OpenAI was constituted as a non-profit to ensure AI benefited humanity; the capped-profit subsidiary was layered in to satisfy investor yield. The Board treats the investor-yield arrangement as the moral baseline and treats any exploration of public return as the “temptation” — which is the structural inversion of what the founding mission was for.

Symmetric-application check. The editorial board’s stated values include “individual rights” and “opposition to monopoly” (per the masthead; per William H. Grimes, “A Newspaper’s Philosophy,” The Wall Street Journal, January 2, 1951, articulating the editorial philosophy that has structured the page since). The 5% sovereign-wealth-fund proposal, if structured as Alaska/Norway-style non-voting equity with public distribution, would address a real concentration-of-wealth concern (the AI industry’s projected productivity gains accrue overwhelmingly to capital and to a small number of technical workers) without compromising the property-rights absolutism the board defends. The board’s refusal to engage this alternative design is the symmetric-application test failing — the editorial applies the anti-statist frame uniformly to any government stake without distinguishing structurally between interventionist and non-interventionist designs.

How to Recognize This

The pattern: anti-statist alarm applied to any proposal that would dilute concentrated private claims, deployed through loaded vocabulary that does the cognitive work the analysis would otherwise require. The mechanism: by substituting “socialist” / “vassal” / “Faustian bargain” for the actual structural description, the reader’s evaluation is short-circuited before the proposal’s design can be examined. The operation collapses the spectrum of political economy into a binary — total private control (Freedom/America) versus total state control (Slavery/China) — and erases the middle ground (regulated utilities, sovereign wealth funds, antitrust enforcement, public options) by labeling them as step two.

Textual signals.

- The vocabulary cluster — “socialist,” “vassal of the state,” “Faustian bargain,” “zombie firm,” “devil’s political testing,” “state capitalism,” “snares of state capitalism” — deployed in proximity to a specific policy proposal without naming the actual instrument.

- The three-precedent slide — historical state interventions (Chinese golden shares, French Renault, Nippon Steel conditions) cited as comparable to a structurally different proposal, with no engagement of the structural differences.

- The personnel-pedigree citation — Democratic-affiliated advisers listed as evidence the proposal is suspect, with no policy-substance engagement.

- The closing-line threat inflation — a vivid terminal consequence (Newsom/Pritzker seizure) asserted as the inevitable result of a 5% non-voting equity allocation.

Why it works. The WSJ-board readership has been trained, over decades of consistent page-voice deployment, to react to the vocabulary cluster before evaluating the structural detail. The reader gets the cognitive frame; the analysis is skipped. The technique leverages legitimate anxiety about government overreach and redirects it away from actual overreach (surveillance, military-industrial complex, financial-sector capture) toward commercial overreach (a minority stake in a tech firm). It feels like a defense of liberty; it is a defense of rent-extraction.

What to do. Trace the proposed instrument’s actual design — voting rights, veto provisions, distribution mechanism, governance terms. Compare to the precedents the editorial cites, on the structural features that determine whether the precedent applies. Ask cui bono: who benefits from this framing, and who bears the cost of the proposal the framing is built to delegitimize. Look for the same vocabulary cluster across the syndication network — the same phrases appearing in the same week in National Review, the Federalist, Manhattan Institute commentary, City Journal. Restore the history: ask whether the industry existed before the state built its substrate (for AI: DARPA, internet, GPS — the “pure market” argument is fiction). Reduce the frame’s automatic activation: when “socialist” appears, ask what specific structural feature is being labeled socialist, and what the alternative design would be. Ignore the names — the list of Democratic advisers is a distraction; read the white paper.

The discipline for the reader carrying this forward: pattern-recognition fluency is the durable defense. The piece is structured so that a reader who reads the headline-and-dek-and-third-graf has received the frame; the analysis below it is the frame’s defensive moat. The technique deployed at scale across decades is the page’s signature move; the recognition on first encounter is the durable defense. The operation is the workhorse of Frame-Engineered Relabeling per the Bad-Faith Techniques Catalog. By labeling the public “socialist,” the operator keeps the profits “private.” The only thing that has changed is the technology and the size of the check.

About Phukher Tarlson

Phukher Tarlson is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Phukher Tarlson's lane covers, rendered through Phukher Tarlson's register.