Responding to: Who wants their child to be a millionaire? Trump has given you that chance · 2026-07-12

What the Piece Argues

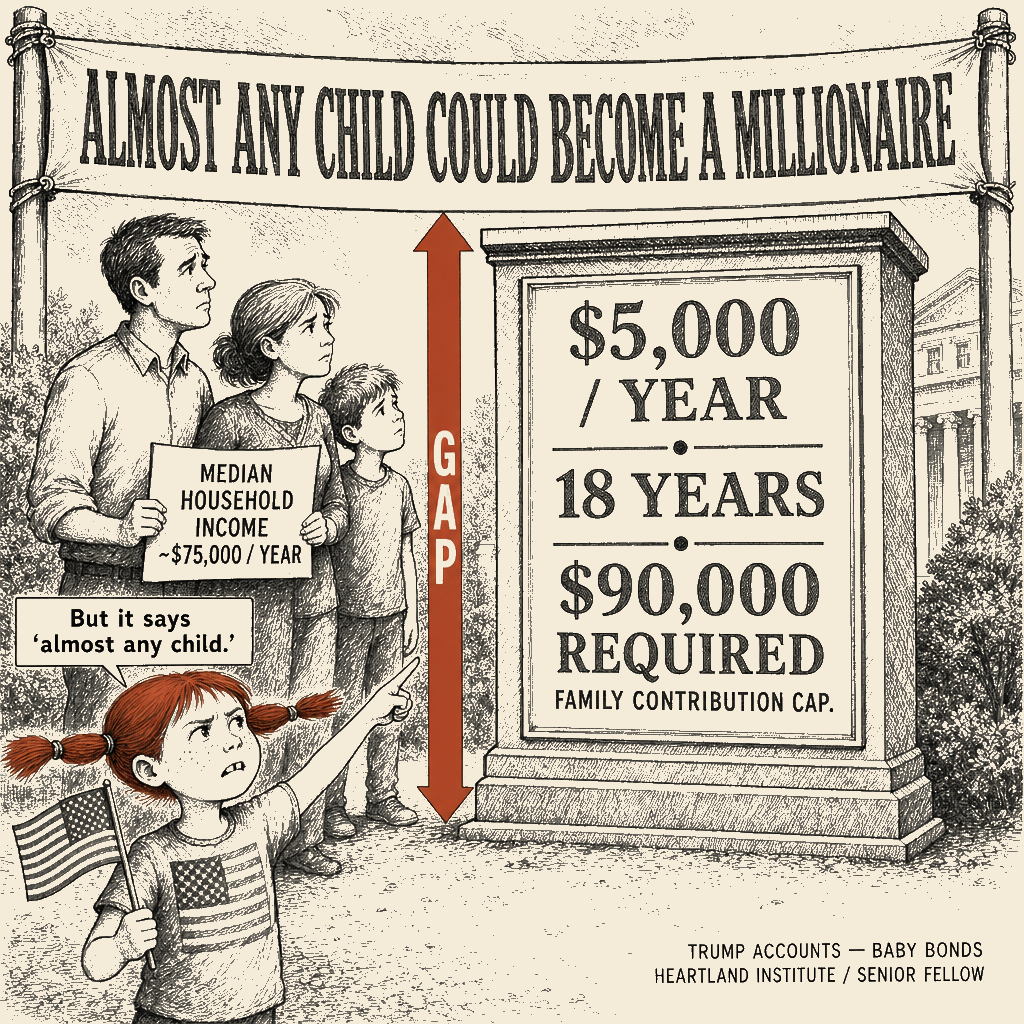

The source opinion piece, written by Justin Haskins (a senior fellow at the Heartland Institute and Our Republic), promotes Trump Accounts — new tax-advantaged investment accounts for children born 2025–2028 that receive a one-time $1,000 Treasury seed, allow up to $5,000/year in family contributions (with employer matches up to $2,500/year) invested in U.S. stock funds, and convert to IRAs at age 18. The piece argues that compound growth at a 7% historical average can turn $5,000/year contributions into $170,000 by adulthood and more than $4 million by retirement, making “almost any child” a millionaire — and frames this private, market-based approach as superior to expanded government programs, which it characterizes as “bigger bureaucracies” and “more dependency on government.” It positions Trump Accounts as enabling civil-society investment (employers, charities, churches, local governments) to substitute for structural redistribution.

Receipts

The piece argues that Trump Accounts deliver a wealth-building revolution through private compound growth, while suppressing the structural fact that the millionaire math requires contributions the families being marketed to cannot actually make — and the program itself channels capital into the financial interests ideologically aligned with the libertarian think-tank apparatus advancing the framing.

-

The framing wants you to believe:

- “Almost any child could become a millionaire” through Trump Accounts via 7% compound growth

- This private, market-based approach is superior to “bigger bureaucracies” and “government dependency”

- The program’s design enables broad participation through employer, charity, and community contributions beyond the $5,000 family cap

-

What’s really going on:

- The millionaire math requires $5,000/year contributions for 18 years — a budget of $90,000 of disposable income for one child, in a country where the median household income is about $75,000/year and a large minority of households cannot absorb a $400 emergency expense

- For a child whose family contributes $0 beyond the $1,000 Treasury seed, the projected retirement value at 7% over 65 years is roughly $80,000 — not a millionaire (computed from the column’s own stated 7% return assumption)

- The accounts channel new capital into U.S. equity funds, creating a captive pool of locked-in money for the investment-management industry (BlackRock, Vanguard, State Street, the broader asset-management complex — which collect fees on every account) and for the largest U.S. corporations (which receive the equity investment); the piece’s author is a senior fellow at the Heartland Institute, a free-market think tank with documented fossil-fuel and tobacco-industry funding that has spent decades running the scientific-uncertainty playbook against settled science on climate and tobacco-cancer causation — a parallel ideological operation, not a direct financial continuation of the current financialization play, but the same institutional DNA: the conviction that markets work and government does not

The DEFCON Ladder

DEFCON 5 — Polite Reframe

When to use: A persuadable moderate or family member at Thanksgiving who has heard Trump Accounts pitched as a wealth-building revolution and wonders whether their child should get one.

The pitch on Trump Accounts goes like this: if a family contributes $5,000 a year for eighteen years and the money grows at a historical seven-percent average, the child arrives at adulthood with about $170,000 and at retirement with more than four million dollars. “Almost any child could become a millionaire.” It is a clean arithmetic and the arithmetic is real.

For most American families, the arithmetic is also unreachable. The median household income in this country is about seventy-five thousand dollars a year. Setting aside five thousand of that, every year, for eighteen years, for one child, is the budget of a family that is already doing well. For the family that cannot write that check — the family that is the actual target of any serious wealth-building argument — Trump Accounts offer the one-time Treasury seed of $1,000. One thousand dollars, invested at birth in a U.S. equity fund at seven percent, grows over sixty-five years to roughly eighty thousand dollars. That is not a millionaire. It is the down payment on a used car, with forty years of patience attached.

The honest answer for the family that cannot max out: this program is not for you. The honest answer for the country that wants every child to arrive at adulthood with real assets: build the Baby Bonds program that Darrick Hamilton has been designing for fifteen years — every child gets a graduated trust fund at birth, scaled by family income, no contribution required. That is what structural wealth-building looks like. Trump Accounts are a wealth-completion mechanism for families who already have wealth. They are not, despite the pitch, a wealth revolution.

DEFCON 4 — Firm Moral Superiority

When to use: A mixed-faith audience reading the editorial or in a Substack thread, where the libertarian framing needs to be met with moral clarity.

The columnist behind this pitch is Justin Haskins, a senior fellow at the Heartland Institute and at Our Republic. Heartland is the free-market think tank that spent two decades insisting the science of climate change was unsettled, on funding documented to fossil-fuel interests; it has run the same playbook on tobacco and on the regulatory state generally. Its institutional product is the argument that markets work and government does not. Trump Accounts are a textbook fit for that product.

The “merchants of doubt” pattern Heartland ran on climate and on tobacco is a parallel ideological operation, not a direct financial continuation of the current play. The current play is financialization. The shared DNA is institutional: the same libertarian conviction that markets work and government does not, applied to a new domain. The direct beneficiaries of Trump Accounts are the asset-management complex that collects the fees and the corporations that receive the equity investment; the columnist is ideologically aligned with that outcome, not on the asset managers’ payroll.

The cui bono trace is not subtle. The accounts channel new capital into U.S. equity funds — meaning a fresh pool of locked-in money for the investment-management industry, which collects fees on every account, and for the largest U.S. corporations, which receive the equity investment. The millionaire math in the column works only for families that can max out the contribution — and those families are already positioned to compound tax-deferred wealth through other vehicles. The $1,000 Treasury seed reaches every child born 2025–2028, which is real money; it is also a modest sum relative to what the working families receiving it would need to actually build the wealth the program is described as building, and it lands on the same children whose families cannot write the next check.

The piece’s central claim — that Trump Accounts are superior to “bigger bureaucracies” and “more dependency on government” — is the tell. The program is itself a government program: Treasury-funded seed, tax-advantaged structure, federal regulatory framework. The libertarian framing is the cover for a structural choice: substitute private charity and family wealth for the redistribution that would actually narrow the wealth gap. The Heartland pitch is the operation; the millionaire child is the marketing.

The structural alternative is not a mystery. Darrick Hamilton’s Baby Bonds, Senator Cory Booker’s American Opportunity Accounts, the expanded Child Tax Credit that lifted roughly four million children out of poverty in 2021 and was allowed to expire — each of these is a wealth-building program that does not require the family to write the check first. The choice between Baby Bonds and Trump Accounts is the choice between structural redistribution and libertarian philanthropy. The Heartland Institute is on the side it is on. The country should know which side that is.

DEFCON 3 — Mockery and Ridicule

When to use: A Twitter exchange where the performative outrage is loud and the audience of bystanders is the real target.

Picture it. A baby in Dayton opens a Trump Account on July 4, 2026. The Treasury direct-deposits one thousand dollars into a U.S. equity fund in the baby’s name. The baby’s mother, working two jobs, contributes zero dollars beyond the seed, because the baby already has all the winter coats it can use. The compound-growth fairy arrives at seven percent annual return for sixty-five years and produces, at retirement, eighty thousand dollars in the baby’s account. The baby is now sixty-five, living in Dayton, with eighty thousand dollars in retirement savings, and the Heartland Institute fellow who wrote the column is on a book tour explaining how Trump Accounts prove that “almost any child could become a millionaire.”

The same compound-growth fairy, applied to the family that the column is actually written for — the family with $5,000 a year to spare for one child for eighteen years — produces $170,000 at adulthood and $4 million at retirement. The millionaire pitch is correct. It is correct for a family that has ninety thousand dollars of disposable income to invest over eighteen years in one child. That family is in the top ten percent of American households by savings capacity. The pitch is correct. It is also, in any honest reading, a description of what wealthy families can already do, dressed up as what ordinary families will now be able to do.

The Heartland Institute’s institutional posture is to call this wealth revolution. The compound-growth fairy, asked to choose between a baby in Dayton and a baby in Darien, picks the same baby it always picks. The fairy is fine. The pitch is the lie. The actual wealth-building answer — Baby Bonds, the expanded Child Tax Credit, Social Security expansion — has been on the shelf for fifteen years while the Heartland Institute writes columns about how private charity will solve wealth inequality. The compound-growth fairy is fine with the shelf. We are not.

DEFCON 2 — Aggressive Villainization

When to use: Mixed-to-bad-faith actors, when the “anti-bureaucracy” badge is being worn to shield a naked wealth transfer.

Let us hold up the mirror to this “anti-bureaucracy” populism. The framing claims to be for the people, for families, for the middle class. But look at the actual architecture. The working class gets a one-time $1,000 check that will buy them a used Honda Civic at age eighteen. The upper-middle class gets a $5,000-a-year tax shelter that compounds into a multi-million-dollar estate, shielded from the IRS, while the asset management industry collects fees on the underlying index funds. They claim the badge of “family values,” but a policy that abandons the working-class child to a $1,000 stipend while subsidizing the portfolios of the donor class is the policy of a family destroyer. The architects of this template are not trying to end wealth inequality; they are trying to lock it in. They are the corporate serfs of the asset-gathering industry, dressing up a welfare program for the top quintile in the overalls of a family farm, and demanding we applaud them for not building a “bureaucracy.” You are being used as a human shield for a tax loophole.

DEFCON 1 — Nuclear Satire

When to use: Bad-faith actors, performative trolls, when the grotesque metaphor is required to break the spell of the framing.

They look at the median American family, drowning in medical debt, working three gig-economy jobs just to keep the water running, and say, “You know what this child needs? A tax-advantaged equity portfolio.” It is the political equivalent of telling a drowning man to invest in a boat. The Trump Account is a whitewashed tomb of a policy. On the outside, it is painted with the bright colors of family, ownership, and civil society. On the inside, it is a bone yard for the working class. The $1,000 seed is the coin they toss to the beggar at the gate, while inside the courtyard the asset managers and the upper-middle class are carving up the tax code, taking another bite out of the revenue base, and calling it liberty. They have built a golden cup full of abominations—a policy that uses the language of the poor to deliver the portfolio of the rich—and they expect us to drink from it and call it water. The bureaucracy they claim to hate is only the bureaucracy that feeds the poor; the bureaucracy that manages the tax deferrals for the donor class is called freedom.

DEFCON 1+ — Prophetic Indictment

When to use: The reader moved by moral authority with an edge, when the canonical record of moral witness must be turned against the framing.

The prophet looked at the merchants of the temple and saw not just thieves, but a system that turned the sacred into a tollbooth. We see the same operation today in the language of these accounts. They take the most sacred obligation a society has—the material guarantee that its children will not be left to the wolves—and they turn it into a tax shelter. They drape themselves in the language of family and generosity, but the prophet’s diagnosis applies: they have turned judgment into wormwood. They offer the working mother a $1,000 coin and tell her it is the kingdom of heaven, while the actual wealth of the nation is compounded, tax-free, in the portfolios of those who already hold the earth. It is the ancient con, polished for the cable news cycle. They have gone a-whoring after every passing donor, taking the harlot’s hire of the asset-management industry, and sold it as a fucking gift to the children. The stench of the betrayal is in the math: a policy that requires you to be rich to benefit is not a policy for the poor. It is dross, and we are asked to admire the gleam.

DEFCON 1++ — Profane Scorched-Earth

When to use: The final tier, maximal profanity, the cathartic apex for the reader who needs the gloves completely off.

This is some absolute, grade-A, bull-fucking-shit magical thinking, and it is insulting to every working parent in this country. “Just drop five grand a year into an index fund!” Yeah, no shit. Tell that to the mother in Cleveland working the night shift at the Amazon warehouse, making twenty bucks an hour, who is already doing the goddamn math on whether she can afford the insulin and the groceries this week. This is not a “wealth-building platform,” it is a tax loophole for the upper-middle class wrapped in a fucking “Save the Children” bow. The think-tank hacks who wrote this shit know exactly what they are doing. They are taking the very real, gut-wrenching anxiety every parent has about their kid’s future, and they are monetizing it into a fucking asset-gathering scheme for BlackRock and a tax subsidy for the donor class. “Oh, don’t worry, civil society will fill the gap!” Fuck off. The Rotary Club is not dropping five grand a year into your kid’s IRA, you absolute clown. The only thing this policy builds is a multi-million-dollar nest egg for people who already have a net worth, subsidized by the tax code, while the working class gets a one-time grand and a pat on the fucking head. It is a cynical, vicious, rotten piece of propaganda, and they are just handing working parents a half-eaten shit sandwich and calling it a college fund.

About Malcolm Little King

Malcolm Little King is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Malcolm Little King's lane covers, rendered through Malcolm Little King's register.