Analyzing: ‘Taylor Swift Tax’ Won’t Hit Just the Kelces — James Freeman · 2026-07-15

What the Editorial Argues

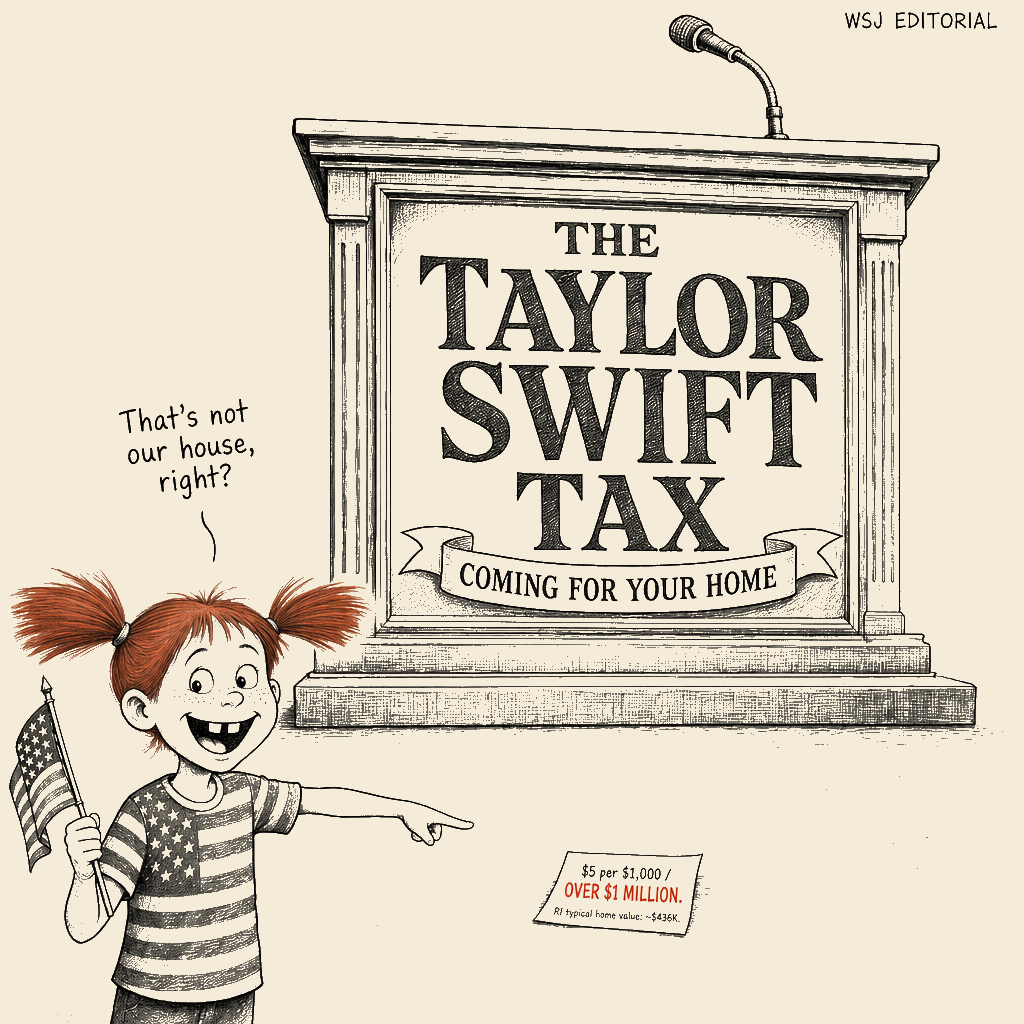

James Freeman argues that Rhode Island’s new property tax, which has been nicknamed the “Taylor Swift Tax” because of its potential impact on the recently married billionaire pop star and her NFL-star husband Travis Kelce, is not a narrowly targeted levy on the ultrarich but a broad-based burden that will fall heavily on middle-class homeowners. The column presents the tax as an economically destructive act of one-party Democratic governance, citing local reporting and a governor’s reluctant signature to suggest that even the bill’s own party recognizes its harm to average working families in a state already carrying a heavy tax load.

Receipts

What the framing wants you to believe. That Rhode Island Democrats passed a tax so egregious it’s named after a celebrity, that it represents a “broad assault on middle-class wallets,” that Governor McKee’s refusal to sign signals bipartisan alarm, and that the state is punishing ordinary families to soak the rich.

What’s really going on. The “Taylor Swift Tax” is a rhetorical frame engineered to generalize outrage from a single celebrity case to anyone who owns property in Rhode Island — while suppressing any discussion of what the tax funds, the rate structure, or the fiscal alternatives the legislature considered. The article’s evidentiary anchor for “broad assault on middle-class wallets” is a WPRI report and similar local coverage indicating the tax applies to homes valued at $1 million and over — which is not the middle class by any measure in Rhode Island, where the typical home value is approximately $436,000 (Zillow typical home value index, 2026). The column leans on Americans for Tax Reform (ATR), a conservative anti-tax advocacy organization founded by Grover Norquist in 1985, as its source for the claim of economic destructiveness — a Tier-3 advocacy source with a documented interest in opposing any tax increase, not a neutral fiscal analysis. The load-bearing omission no reader would catch: what revenue the tax is intended to fund and what alternatives were available. Without that context, “tax increase” is an empty moral category rather than a fiscal choice between funding schools vs. funding pensions vs. cutting services vs. raising other taxes. Anchor citation: the WPRI report itself limits the tax’s reach to million-dollar properties; the generalization to middle-class homeowners is invented.

The Operation

Cui bono. The piece’s institutional authorship is straightforward: James Freeman is an assistant editor of the Wall Street Journal editorial page, writing for an outlet that has opposed nearly every tax increase at every level of government for seventy-five years. The piece serves the WSJ’s signature audience-management choreography (§4.3, WSJ Technique Catalogue — multiple-audience-targeting). The wealthy reader receives: your class is being treated like Taylor Swift; this state is hostile to the propertied, another data point for the “blue state failure” frame (§4.9). The populist-conservative base receives: Democrats are coming for your house, your savings, your future — and they’re doing it in the worst-run states. The political class receives: here is a citable argument that a celebrity-named tax hurts ordinary people, useful for repeating in hearings and op-eds across the syndication network. The technocratic reader receives: a Tax Foundation–aligned analysis (via ATR) that the tax is economically destructive, treated as independent evidence.

Distributional impact and beneficiaries. The concrete beneficiary is the donor class that benefits from anti-tax sentiment — the coalition that has successfully blocked progressive taxation for decades, funded by the donor network that Americans for Tax Reform has been the conducted arm of since Norquist founded it in 1985. The named cost-bearers are “hard-working citizens” and middle-class families; the actual cost-bearers, in the counterfactual where the tax funds essential services, are the public-sector recipients of those services — schools, infrastructure maintenance, health programs — and, in the alternative where the tax is defeated without replacement, the same residents who then absorb service cuts. The editorial’s deployment of ATR is itself a relabeling — the “taxpayer watchdog” Calloway Bills is presented as neutral when the organization is a partisan anti-tax advocacy shop. This is the same §4.1 substitution technique that relabeled “tax hike” as “revenue grab” and “estate tax” as “death tax”; the editorial applies it to the source identity itself.

Alternative design. If the editorial’s stated concern were actually about tax fairness and fiscal sustainability rather than about blocking revenue, it would have asked: what is this tax funding, what would the alternatives cost, is there a more progressive rate structure, and do the benefits of the spending exceed the cost of the tax? None of those questions appear. The alternative design, reconstructed from the disadvantaged constituency’s interests, is not “no tax increase” but “transparent fiscal choice with the revenue’s purpose and incidence disclosed.”

FGL — Fear, Greed, Laziness. Fear: a celebrity’s tax bill is coming for your house. Greed: your property value and inheritance are under threat. Laziness: you don’t need to read the tax code or the state budget; the frame tells you everything you need to know by naming the celebrity. Applied symmetrically across three constituencies: the editorial’s author (fear of losing anti-tax momentum; greed for continued donor-network support; laziness of recycling a familiar frame rather than reporting actual fiscal data), the apex beneficiary (the ATR donor network, whose greed is avoidance of progressive taxation, whose fear is that the public might learn taxes fund services they support, whose laziness is in funding columns rather than making an affirmative case for cuts), and the rank-and-file reader (whose fear of higher taxes is real and human, whose greed is the natural concern for family finances, whose laziness is the normal citizen’s inability to track a state budget — these are not contemptible; they are the conditions the operation was designed to exploit).

Technique identification.

- Frame-engineered relabeling (WSJ Technique Catalogue §4.1, Bad-Faith Techniques Catalog entry). The substitution of “Taylor Swift Tax” for “property tax increase on million-dollar homes” is textbook. The WSJ catalogue’s substitution table at §4.1 lists “tax hikes” → “revenue grabs” and “estate tax” → “death tax”; here the move is the same: a specific rate increase relabeled as personal punishment of a celebrity to activate outrage-and-envy circuitry. The scare quotes in the title are the writer’s own acknowledgement that the label is a construction — then he deploys it anyway. The same technique operates at the sourcing level: ATR’s Calloway Bills is introduced as “taxpayer watchdog,” a neutral-sounding relabel that suppresses the organization’s partisan mission, mirroring the §4.1 substitution table’s same schema applied to source identity.

- Hasty generalization (Bad-Faith Techniques Catalog, Bad-Faith Field Guide §2). From a tax on properties assessed over $1 million, Freeman generalizes to “broad assault on middle-class wallets.” The base rate for middle-class impact is zero in the source he cites; the generalization is unsupported and suppressed.

- Austerity-thrift deployment (WSJ Catalogue §4.2, “The austerity-thrift archetype”). The piece is a pure permission structure: the suffering of those subject to the tax is framed as an assault by Democratic governance on “hard-working citizens,” letting the reader who benefits from anti-tax policy feel that opposing the revenue is a defense of the ordinary person rather than a distributional choice favoring the propertied. The permission-structure move (catalogued at §4.2) — moral justification through the higher cause of protecting the middle class — and euphemistic labeling (“egregious exaction” for a property tax increase) run in concert.

- Threat-inflation closer (WSJ §4.13). The closing invocation that the tax is “economically destructive” and encourages no one to stay uses civilizational stakes language — the tax isn’t just unpopular; it’s a structural threat to Rhode Island’s viability — without any analysis of the state’s total fiscal picture.

Audience-management function. The piece is a permission structure for the wealthy reader to feel their tax avoidance is aligned with the interests of “hard-working citizens,” and a grievance-ratification vehicle for the populist base to see Democratic state governance as inherently hostile to normal people. The celebrity name is the vector: it gets the piece read, it gets the frame repeated, and it does the work of suppressing the fiscal substance the reader would otherwise have to evaluate.

The Record

Anchor receipts and their tiers.

| Claim | Evidence in article | Tier | Verdict |

|---|---|---|---|

| Tax applies to homes valued at $1M+ | Widely reported (WPRI, Bloomberg, Yahoo) | Tier 1 (wire/locally-sourced journalism) | Supported — but this contradicts the “middle-class” framing |

| Tax is “broad assault on middle-class wallets” | None provided | Unsupported | Hasty generalization — the $1M threshold is far above the typical home value in Rhode Island (~$436k) |

| Tax is “economically destructive” | Cited via Americans for Tax Reform / Calloway Bills | Tier 3 (advocacy) | The source has a known anti-tax mission; no independent economic modeling is cited |

| Governor McKee was embarrassed, refused to sign | Governor’s letter is cited but not quoted substantively | Unconfirmed — textual cue exists but the letter’s content is not reproduced | The reader cannot verify how much of the letter concerns the tax’s structure vs. other policy objections |

| ”State politicians are not encouraging anyone to stay” | Opinion assertion | No evidence | Presupposes the tax will cause flight without citing any empirical analysis of migration patterns |

Load-bearing omissions.

- The article does not state the tax’s rate structure, only the $1M threshold. (The rate is $5 per $1,000 over $1M, as reported elsewhere — a fact the editorial suppresses.)

- It does not identify what the tax revenue is intended to fund — a necessary fact for any “destructive” claim.

- It does not name the alternatives the legislature considered (a broad-based rate increase, service cuts, debt issuance).

- It does not disclose that its primary source (Americans for Tax Reform) is a political organization founded by Grover Norquist that opposes all tax increases by principle, not by case-by-case analysis — a material interest.

- It does not engage with the documented fiscal pressures on Rhode Island (pension obligations, infrastructure, education funding) that any revenue debate must account for.

Per-citation accuracy verdicts. The WPRI citation surfaces accurately; the ATR citation is accurate as a quotation but the editorial treats a partisan advocacy source as an independent expert, which is the classic WSJ “study shows” pattern (§4.5 of the catalogue — treating a think-tank product produced by a coordinated network as neutral evidence). The same relabeling technique used on the tax itself is applied to the source: Calloway Bills is “taxpayer watchdog” — a neutrality frame that the §4.1 substitution table would recognize.

Missing-information declaration. No documentary or public-record source has been surfaced that provides a net-rate analysis, an independent fiscal impact study, or the legislative alternative proposals that would resolve whether this is a reasonable revenue measure or an “egregious exaction.” The rate structure (a $5 per $1,000 surcharge on the value above $1M) is known from external reporting but absent from the editorial; the reader’s ability to judge the editorial’s claims is limited to what the editorial itself supplies — which it structures to produce the anti-tax conclusion without the substrate to evaluate it.

How to Recognize This

The “pop star tax” frame is a recurring technique: a tax increase is nicknamed after a celebrity to trigger the reader’s associative circuitry — envy, admiration, fear that what hits the celebrity is coming for you — and then generalized to a “middle-class assault” without evidence. It is the same mechanical move as the “death tax” (Winston Churchill metaphor → Frank Luntz relabeling), the “luxury tax on the rich” (which the WSJ editorial page spent the 1990s fighting), and the “millionaire’s tax” frame deployed against every progressive rate increase. The batch is editorial cooked the same way every time.

The mechanism. Frame-engineered relabeling + hasty generalization, deployed together. The relabeling does the emotional work — you can’t read “Taylor Swift Tax” without the mental image of her extraordinary wealth. The generalization does the political work — that emotional charge transfers to anyone who owns property. The fiscal substance (rate, base, purpose, alternatives) is suppressed because it would break the transfer.

Textual signals.

- A celebrity’s name or image in the headline or lede of a tax article — treat as a frame flag.

- The transition from “billionaire example” to “this hits ordinary people too” without rate-base data.

- The source is a named anti-tax advocacy organization rather than the state’s own fiscal analysis or an independent budget evaluation.

- The scare quotes in the headline (“Taylor Swift Tax”) that the piece then treats as a neutral descriptive term.

Why it works. The celebrity name generates attention and shares; the fear of “coming for you next” is the most reliable voting cue in modern politics; and few readers have the time, access, or inclination to look up the actual property-tax code and the budget the revenue funds. The piece converts attention into outrage and outrage into opposition without the reader ever needing to know what the tax actually does.

What to do when you see it. First, trace the actual tax base: who really pays, at what rate, at what valuation? Second, ask: what is this revenue for? If the editorial doesn’t tell you, that is the suppressed variable. Third, check the advocacy source’s agenda — Americans for Tax Reform opposes every tax increase and does not disclose alternative fiscal paths. Fourth, run the cui bono: who benefits from making this tax impossible to pass without scrutiny? Not the middle class the editorial claims to defend, but the donor network that has successfully blocked progressive taxation for decades.

I know this frame because I built versions of it. We built versions of this column. The “you’re next” frame with a celebrity hook was a reliable piece of the mid-2000s arsenal. The bitterness I carry is not at the frame — it worked, that’s why we used it — but at what it cost: a reader’s capacity to evaluate a real fiscal question replaced by a triggered emotional response. The identification is the recovery.

About Phukher Tarlson

Phukher Tarlson is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Phukher Tarlson's lane covers, rendered through Phukher Tarlson's register.