Responding to: Debanking Suddenly Leaves Banks Legally Exposed — Jay Rogers · 2026-07-14

What the Piece Argues

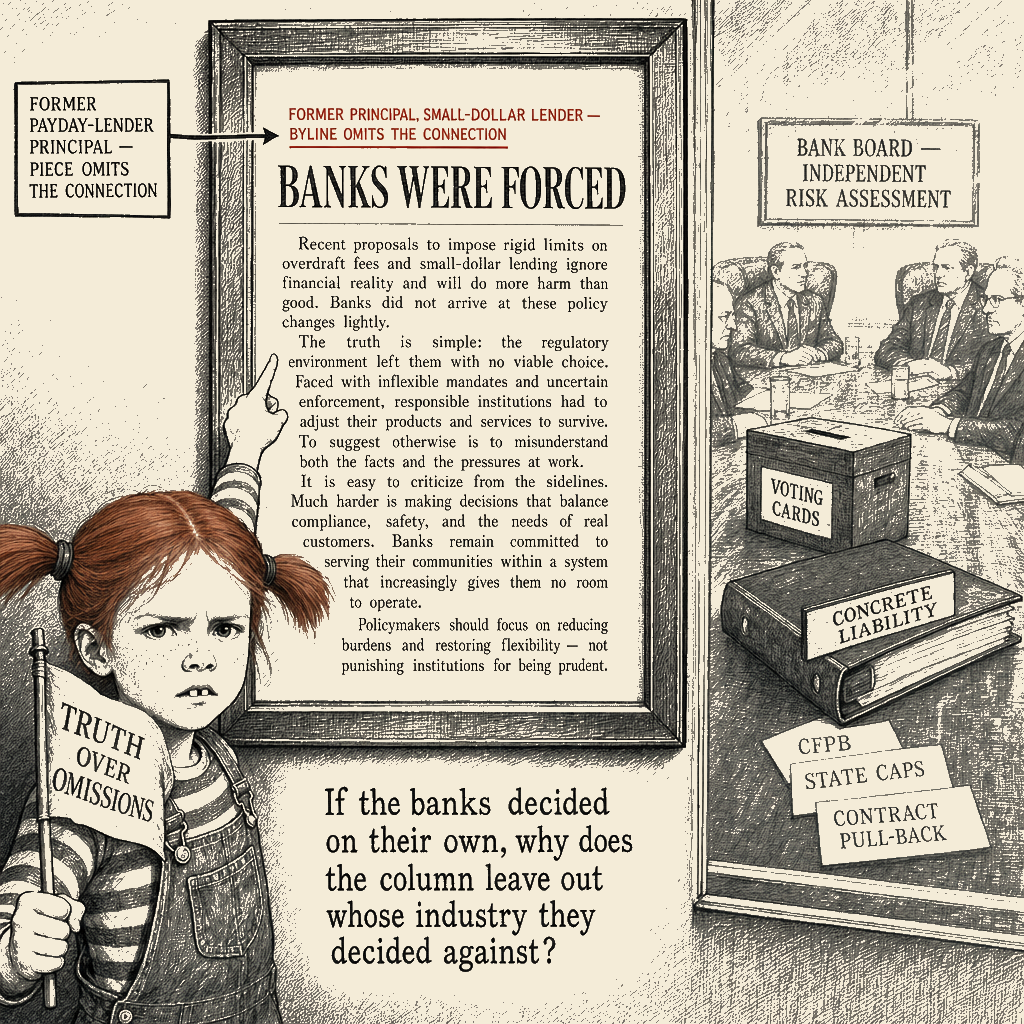

The opinion argues that the OCC and FDIC’s new rule ending “reputational risk” as a supervisory factor retroactively exposes banks to litigation for decisions they made under government pressure to cut ties with disfavored industries. The author, a former small-dollar lending executive, contends that coordinated regulatory pressure — from Operation Choke Point to IRS targeting of conservative nonprofits to post-2020 debanking — created a regime where regulators used informal discretion to achieve what legislation could not: forcing private institutions to discriminate against entire legal industries (payday lenders, gun dealers, oil and gas, digital assets) through implicit threat rather than explicit rule, leaving the banks holding the liability when the regulatory cover is withdrawn.

Receipts

The piece frames bank debanking as coerced censorship of lawful industries — but the industries in question had documented records of consumer harm that banks independently recognized as material risk.

The framing wants you to believe

- That banks were innocent bystanders forced by regulators to drop lawful customers, and the new rule unfairly leaves them holding the bag

- That “reputational risk” was a bureaucratic invention that served no legitimate purpose

- That the nine identified industries (payday lending, firearms, private prisons, oil and gas, etc.) were targeted for political reasons, not because they carried documented patterns of consumer abuse, regulatory violations, and litigation exposure

- That the proper remedy is to let banks serve any legal industry without regulatory pressure

What’s really going on

- The OCC’s own review covered 2020–2023 — the period when banks themselves had already concluded that serving payday lenders (with state-level interest rate caps proliferating and CFPB enforcement active), private prisons (with federal contracts shifting), and coal (with declining economics and mounting climate litigation) was not just a reputational problem but a concrete liability problem. The regulatory “pressure” the piece describes was in many cases downstream of market realities the banks had already recognized

- “Operation Choke Point” (2013) was officially a fraud-prevention program targeting third-party payment processors that were processing for fraudulent merchants — including payday lenders where auto-draft abuses and tribal-sovereignty evasion had generated thousands of consumer complaints. The FDIC guidance the piece cites was responding to documented consumer harm, not political animus

- The piece’s own author ran “Loantopia” — a small-dollar lending operation — and previously advised Mobiloans, an online tribal lender that was precisely the type of operation that generated the consumer-protection concerns driving the regulatory response. The piece’s framing as a neutral observer of “debanking” is structurally analogous to a coal executive lamenting that banks won’t serve coal companies anymore

- The “5.6 million unbanked households” statistic the piece cites to argue that debanking created unmet credit needs is misleading: the unbanked rate has been falling for decades (from 7.6% in 2019 to 4.2% in 2021 before rising to 5.6% in 2023 per FDIC data), and the primary reasons households report being unbanked are insufficient income and distrust of banks, not inability to access payday lending

Anchor citation: FDIC 2023 National Survey of Unbanked and Underbanked Households (showing primary reasons for being unbanked are income-related, not credit-access-related); CFPB Supervisory Highlights on payday lending (2015–2020 cycles showing pattern of consumer harm); OCC preliminary report on debanking (December 2024, confirming policies were in place but not examining whether bank decisions were independent of market assessments).

The DEFCON Ladder

DEFCON 5 — Polite Reframe

When to use: With a well-meaning relative or coworker who read the piece and thinks “the government made banks drop lawful businesses, and now the banks are stuck with the lawsuits.”

Let’s sit with what actually happened here. The author is right that Operation Choke Point had real problems — using regulatory pressure as a backdoor to achieve policy goals is not how a properly functioning administrative state should work. Abuses by the IRS targeting conservative nonprofits were real and were properly condemned.

But the piece asks us to believe that nine of the largest banks in America — each with armies of lawyers and compliance officers — cut off entire industries only because regulators pressured them, and that these same banks never independently assessed whether payday lending (with state-level interest rate caps and thousands of CFPB complaints on file), private prisons (with the federal government itself reducing contracts), or coal (in terminal economic decline) carried concrete legal and financial risk.

We should be able to hold two thoughts at once: yes, regulatory pressure was real and in some cases improper; and yes, many of these industries were dropped because banks honestly assessed the liability exposure and concluded the business wasn’t worth it. The regulatory cover may have made the decision easier, but the underlying risk was real. The conversation we need is about how to make the regulatory process transparent and rule-bound — not about restoring access to high-cost credit and extractive industries whose business models depended on regulatory indifference.

DEFCON 4 — Firm Moral Superiority

When to use: In a comments section or Substack reply where someone is using the piece to claim “the administrative state is persecuting lawful businesses.”

Let’s be precise about what the piece is actually arguing. Jay Rogers — former executive of Mobiloans (an online tribal lender) and Loantopia (a small-dollar lending portfolio company) — is telling us that banks should not have been “pressured” into dropping industries like payday lending. The same payday lending that, at Mobiloans specifically, involved tribal-sovereignty evasion to bypass state interest rate caps. The same industry that the CFPB documented engaging in “debt traps” where loans carried effective APRs exceeding 400% and where lenders debited accounts repeatedly, generating overdraft fees on top of default.

The OCC’s new rule doesn’t create a legal problem for banks. It creates a rhetorical problem: the regulatory cover is gone, and the banks are now exposed to the question they’ve dodged for a decade. Not “did a regulator suggest you drop this customer?” but “did your own board independently conclude that serving this industry was consistent with your fiduciary duties?”

That’s a fair question. Banks that cut ties with payday lenders after CFPB enforcement actions, that dropped private prisons after the federal government moved away from them, that walked away from coal after the economics collapsed — those banks have nothing to fear. The ones who should worry are the banks that dropped customers based on a wink and a nod from a regulator, without any independent risk assessment. And the piece’s real complaint is that those last five years of wink-and-nod decisions are no longer protected.

The Fifth Amendment takings claim the piece floats — that coordinated government pressure to exclude legal industries constitutes a taking — is creative but structurally unsound. The Takings Clause requires government appropriation of private property for public use; regulatory pressure on third-party intermediaries to discontinue commercial relationships with specific industries does not fit the doctrinal framework without a showing of direct government appropriation of the bank’s property. An industry that depends on banks being forced to serve it, regardless of the banks’ own independent risk assessment, is not an industry with a constitutional right to banking services. It’s an industry that needs to make its case in the market, not through the barrel of a regulation that says “you must serve me.”

DEFCON 3 — Mockery and Ridicule

When to use: When someone deploys the piece’s frame in a context where the audience already knows the industry history — catching bystanders with the absurdity.

This is a beautiful piece of work. “Please feel terrible for the nine largest banks in America, who were meanly pressured by regulators into the terrible burden of not profiting from payday lending, private prisons, and coal companies.”

The horror. The tragedy. Citibank had to not process payments for loans at 400% APR. Bank of America had to not bank the industry that generates thousands of CFPB complaints annually. Capital One had to not serve the gun shop whose owner is “shocked” — shocked! — that payments were stopped without explanation. From the man who ran Loantopia, the company named after the village where every financial product is a loan and every loan is a profit center.

Here’s the part the piece hopes you won’t notice: Jay Rogers advised Mobiloans, a tribal lender that used tribal-sovereignty claims to evade state interest rate caps. The entire business model was “we can charge whatever we want because a tribal nation says so.” And the piece’s position is that banks should have been forced to process payments for this business model, and that regulators who said “maybe this is consumer fraud” were the bad guys.

The piece ends with a grand rhetorical flourish: “Someone will test that theory now, and my money is on the Justice Department to get there first.” My money is on the Justice Department showing up with a spreadsheet of consumer complaints and asking a jury whether Capital One’s decision to drop a gun shop that can’t get CFPB complaints on the record (because none exist) was a duty-of-care failure or a rational business judgment.

The real legal exposure isn’t the banks that dropped payday lenders. It’s the banks that kept serving them, and the boards that approved “reputational risk” policies without documenting the underlying analysis — because now they have to explain to a jury why they dropped the adult entertainment industry (federal sex trafficking liability exposure, actually well-documented) and not the fast-food chains using the same payment processors.

DEFCON 2 — Aggressive Villainization

When to use: In a forum or comment thread where the piece is being used to argue for broader deregulation of financial services, and the audience needs to see the structural interest behind the complaint.

The piece’s real grievance is structural. An entire class of industries — payday lending, private prisons, coal, firearms — lost access to the banking system not because of a regulatory ban, but because banks independently assessed the risk and liability exposure and decided the business wasn’t worth it. The piece’s author, who ran companies that depended on regulatory indifference to tribal-sovereignty evasion schemes that allowed 400% APR lending, is now writing for the opinion pages of the most powerful financial newspaper in the world to argue that banks should be forced to serve those industries. This is not a neutral analysis of regulatory overreach. This is a former industry insider writing the brief for the next round of extraction — framing the predatory lender’s access to the banking system as a constitutional right.

The OCC’s own report found that nine major banks dropped or restricted these industries. The piece wants you to believe this was a coordinated political purge. The more plausible reading: at the same time that CFPB enforcement actions were exposing payday lending abuses, at the same time that federal and state governments were moving away from private prisons, at the same time that coal was becoming an economic and climate liability — banks, exercising ordinary business judgment, concluded these industries were risky, expensive, and not worth the litigation exposure.

The “reputational risk” label may have been a convenient shorthand. But the underlying risk was real. The piece’s argument that this was purely political requires you to believe that the nation’s most sophisticated financial institutions, each employing thousands of compliance professionals, simply followed regulatory pressure like lemmings into decisions that cost them billions in fee income — and that the only reason they did so was because regulators whispered the magic words “reputational risk.”

The alternative — that these banks independently reached the same conclusion because the industries in question had real consumer-harm profiles, real litigation exposure, and real economic decline — is inconvenient for the piece’s narrative. But it’s also what the OCC report actually found when it looked at the banks’ internal documentation: policies were in place, but the policies were the banks’ own. The regulatory pressure was the context, not the cause.

The duty-of-care lawsuit the piece is so excited about will have to answer a simple question: was it negligence for a bank board to decide that serving a lender charging 400% APR through tribal-sovereignty evasion posed any kind of risk? If the answer is no — if banks must serve any legal industry regardless of the consumer-harm profile — then the piece is arguing for something far more radical than “stop regulatory overreach.” It’s arguing for a world where banks have no discretion at all, and every lawful business has a constitutional right to a checking account.

DEFCON 1 — Nuclear Satire

When to use: When the piece is being cited as authoritative by someone who claims not to understand why payday lending was targeted, and the audience needs a grotesque but accurate image.

The OCC and FDIC eliminated “reputational risk” supervision. Now the nine largest banks in America — the same banks that collectively extracted more than a trillion dollars from the American economy over the last decade through fees, interest, and overdraft charges — are worried about liability for declining to process payments for the industries that charge them fees for processing payments for the industry that charges borrowers 400% APR.

Picture the chain: the payday borrower’s bank account is drained by an auto-debit that the lender runs three times to force a default. The borrower pays overdraft fees to her bank. The bank collects processing fees from the lender. The lender’s shareholders collect dividends. The piece’s author collects a consulting fee for advising the lender. And the Wall Street Journal op-ed page collects prestige for publishing the complaint that the whole extraction chain should be protected from regulatory scrutiny.

It’s extraction all the way down, and the extraction has a face. The payday borrower’s account emptied by automated withdrawal. The bank’s compliance department drained by subpoena costs. The op-ed page’s credibility drained by running a piece that omits the author’s industry position. The solution the piece offers to the 5.6 million unbanked households is: make sure payday lenders can get payment processing. Not higher wages, not lower healthcare costs, not accessible credit from regulated institutions. Payment processing for the tribal lender charging 400% APR. The circular logic of extraction: the people who cannot afford bank accounts need access to the industry that extracts wealth from the people who cannot afford bank accounts, and the people who process payments for that industry should be forced to do so at gunpoint of regulation, and the regulators who say “maybe don’t profit from that, actually” are the constitutional villains.

The piece closes with a confession it doesn’t realize it’s making: “My money is on the Justice Department to get there first.” Of course it is. The Justice Department, under any administration, loves a case where it can subpoena bank records and ask “did your board independently evaluate whether serving a tribal lender that evades state interest rate caps was consistent with your fiduciary duties?” The banks will settle for a billion dollars, the DOJ will announce a “landmark consumer protection enforcement action,” and Jay Rogers will write another piece explaining that this is all the regulators’ fault for creating the expectation that banks should think for themselves.

DEFCON 1+ — Prophetic Indictment

When to use: When the moral frame needs to be named — not “this is bad policy” but “this is a species of institutional sin that the record condemns.”

Let us speak plainly. The prophet’s office is to name what is hidden, and what is hidden in this piece is the structure that produces the complaint.

The author ran companies whose business model was extracting wealth from the working poor through loans structured to trap rather than release. The rates were not 15% or 18% or even 36%. They exceeded 400% in annualized terms — a rate that, in any honest moral accounting, is not a fee for service but a form of what the Mosaic law called neshekh: the biting interest that consumes the borrower’s substance. The author now writes to say that the banks should not have been permitted to conclude, on their own judgment, that facilitating this extraction posed a risk to their own institutional integrity.

The Vullo decision the piece cites is relevant. The Supreme Court held that a regulator’s threat against insurers and banks, used to pressure them into dropping disfavored customers, can state a First Amendment claim. But the question the piece does not ask is whether the regulator’s substance — the content of what was being pressured — was itself a legitimate exercise of the state’s duty to protect the vulnerable. The regulator was not saying “drop the gun shop because I disagree with the Second Amendment.” The regulator was saying, in the aggregate across sectors, “these industries have generated documented patterns of consumer harm; your facilitation of that harm may create liability exposure for your institution.”

We are asked to believe that the ancient CFPB and the FDIC and the OCC — those vast, lumbering institutions of the administrative state — somehow hypnotized the most sophisticated financial institutions on earth into abandoning profitable business lines. The Hebrew prophets had a word for this: the refusal to see what is actually happening, because seeing it would require an accounting the seer does not want to make.

The 5.6 million unbanked households are real. Their suffering is real. The piece uses their suffering as a rhetorical weapon to argue for restoring the access of predatory lenders to those households. That is the inversion the prophets named: the powerful presenting themselves as the victim of a system designed to protect the vulnerable, and demanding the system be dismantled so the extraction may resume.

Amos 5:24 — “But let justice roll down like waters, and righteousness like a mighty stream.” The justice rolling down is not a Justice Department subpoena. It is the structural fact that a business model dependent on charging 400% APR to the working poor, and on coercing banks to process those payments, is not a business model with a right to exist. The bank that declined to facilitate that extraction was not acting from political animus. It was acting from an assessment the market itself demanded. We do the prophet’s work when we refuse to let the extraction class dress its complaint for continued extraction in the language of constitutional grievance.

DEFCON 1++ — Profane Scorched-Earth

When to use: When someone has deployed the piece as “proof” that regulatory overreach is the only reason payday lending got pushed out, and the response needs to be loud enough to drown the echo.

Oh, this is a beautiful fucking piece. This is a masterwork of the extraction class writing its own brief, and the Wall Street Journal ran it on the op-ed page with the copyright notice and everything.

Let me translate what’s actually being argued here. “The government told banks they should maybe think twice about processing payments for industries that have generated thousands of consumer fraud complaints, and now the banks are worried that a jury might ask them why they dropped those customers without doing their own risk assessment. This is an outrage. The banks should be protected from having to think for themselves. And also, my payday lending clients should get their payment processing back.”

The piece’s author ran Loantopia. He advised Mobiloans — a tribal lender that built its entire business model on the proposition that tribal sovereignty means it can charge 400% APR and the state of California can go fuck itself. And his position is that Capital One should be forced to process payments for the gun shop whose owner says he was “shocked” when payments stopped. Shocked! The man who charged 400% APR through a sovereign-nation loophole is shocked — shocked — that a bank might independently decide not to participate.

Here is the suppressed variable the entire piece is built to hide: these industries were not targeted because regulators hate freedom. They were targeted because the industries themselves are dogshit businesses that produce documented, measurable, billion-dollar piles of consumer harm. Payday lending is a debt trap by design. Private prisons rode the mass-incarceration wave and are now facing the economic consequences. Coal is dying because the economics collapsed, not because of ESG — the market killed coal before the regulators even got their boots on.

The OCC report found nine sectors were restricted. Notice what the piece doesn’t argue: that any of these restrictions were factually wrong — that payday lending is actually fine for consumers, that private prisons are a model of rehabilitation, that coal is coming back. It can’t argue that, because the evidence doesn’t support it. So instead it argues that the process was wrong — that regulators applied pressure instead of passing a law, and that banks should have done their own analysis.

And now the banks are exposed. Good. The duty-of-care argument is going to be a beautiful thing to watch. “Your honor, the board approved dropping payday lenders without any independent analysis.” “And what would an independent analysis have shown?” “That payday lending had a documented pattern of consumer harm, regulatory enforcement actions, state interest rate caps, and litigation exposure.” “So the board’s decision was correct on the merits, you just object to the process?” “Yes.” “Case dismissed.”

The Justice Department subpoena is not the threat the piece thinks it is. The subpoena is the government asking the banks “did you coordinate with each other on these decisions?” If the banks coordinated, that’s a Sherman Act problem. If they didn’t coordinate, and each independently reached the same conclusion — that serving payday lenders charging 400% APR was not worth the risk — then the DOJ has nothing, and the piece’s entire argument collapses into “well, the banks should have been stupider about their risk assessment.”

That’s what this is really about. The extraction class wants banks to be stupider. It wants banks to serve predatory lenders without asking questions, process payments for gun shops without looking at the compliance risk, and keep the money flowing to industries whose business models depend on regulatory indifference. And when banks, using the judgment they are paid billions of dollars to exercise, say “no, this is too risky,” the extraction class runs to the Wall Street Journal and writes a piece about “reputational risk gone wrong.”

Fuck that. The reputational risk was real. The markets spoke. The extraction is what got extracted — from the payday borrower, from the prisoner’s family, from the coal miner’s community. The banks didn’t cause that extraction, but they were its facilitator, and when they stopped facilitating it, the extraction class called it persecution.

Someone should indeed test this theory in court. And my money is on the discovery production — where the bank produces the board’s risk assessment, the CFPB enforcement actions, the consumer complaint database, and the jury sees that this was not politics but prudence. The constitutional theory is a taking without compensation. The market theory is a taking without profit. And the jury will side with the bank every time.

About Malcolm Little King

Malcolm Little King is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Malcolm Little King's lane covers, rendered through Malcolm Little King's register.