Responding to: Trump’s Nuclear Renaissance Is Stalling — Paul H. Tice · 2026-06-29

The primary power-protecting talking point: “Mr. Trump could deploy his standard business playbook: Summon leading Wall Street infrastructure private-equity managers to the White House and make the pitch for why things will be different this time with his promised nuclear reforms.”

What the Piece Argues

The piece, a Paul H. Tice op-ed in the June 29, 2026 Wall Street Journal titled “Trump’s Nuclear Renaissance Is Stalling,” argues that the Trump administration’s nuclear energy program is failing more than a year after executive orders promising to quadruple U.S. nuclear capacity by 2050. The author attributes the stalling to three causes: administration focus on unproven fusion and small modular reactor (SMR) designs instead of proven gigawatt-scale AP1000 reactors; distraction by foreign deals like the September 2025 U.K. nuclear agreement; and U.S. utility reluctance to commit to new AP1000 builds in the wake of the cost overruns and bankruptcy that followed the two Vogtle units completed in 2023-24. The proposed solution is for President Trump to summon the private-equity firms (BlackRock, Blackstone, and others) that have acquired major U.S. utilities to the White House to lead the next AP1000 buildout, with the October 2025 Westinghouse-government partnership as the financial backbone.

Receipts

The framing sells a PE-led nuclear buildout as the obvious cure for an industry that won’t commit to its own product.

-

The framing wants you to believe:

- U.S. utilities are merely “risk-averse” customers who need a Wall Street pep talk before they will build

- AP1000 is the only serious technology; fusion and SMRs are “shiny objects” with no path to commercial scale

- The last AP1000 build was a one-off; the next will be cheaper and faster on the merits

- The October 2025 Westinghouse-government partnership is the right financial backbone

- Foreign deals (the September 2025 U.K. nuclear agreement) are a distraction from the real work

-

What’s really going on:

- Westinghouse, the proposed build partner, has been owned by Brookfield Asset Management since emerging from bankruptcy in 2018; the October 2025 deal gives the U.S. government an equity stake in a foreign-controlled private contractor to backstop the contractor’s risk

- The same PE firms (BlackRock, Blackstone, and peers) that engineered the five-year utility-consolidation buying spree are now being positioned as the cure for the consolidation they produced

- “Risk-averse utility customers” is a sympathetic frame for the math not working — Vogtle Units 3-4 ran more than $20 billion over budget, bankrupted Westinghouse, and put the overruns on Georgia Power ratepayers

- The framing’s dismissal of SMRs and fusion requires ignoring that NuScale, TerraPower, and X-energy are at advanced NRC licensing stages with documented commercial pathways

- Anchor: the Department of Energy’s own Annual Energy Outlook, issued April 2026, projects essentially no growth in U.S. nuclear generation capacity through 2050 under either baseline or high-demand scenarios — the “stalling” the op-ed diagnoses is the DOE’s own conclusion

- The op-ed is written by the author of the National Center for Energy Analytics’ “A Strategy for Financing the Nuclear Future” report — the policy paper the piece is paraphrasing, published as opinion

The DEFCON Ladder

DEFCON 5 — Polite Reframe

When to use: Persuadable moderates, good-faith family members who just read the headline and think the government is too slow to build things.

Think of Brenda in Atlanta, whose electric bill doubled over the last decade to pay for the nuclear bailout at the Vogtle plant. The author of this piece looks at that crisis and concludes we need to give the blueprint to BlackRock. The administration claims it needs “sophisticated investors” to manage the risk of building new nuclear reactors. But when the last reactor of this exact design came in $20 billion over budget, the investors didn’t pay the difference—the ratepayers did. That is not risk management; that is a shakedown with a balance sheet. We are Christians and builders, and we know that a system where the public insures the bet and the billionaire keeps the winnings is not the free market. It is theft. We are the ones who actually build the public commons; we build for the people, not for the extraction of the few. We are the builders.

DEFCON 4 — Firm Moral Superiority

When to use: A reader who leans toward the framing but should hear the cui bono; an op-ed or Substack reply; identity-protective mixed-faith actors who can hold the contradiction.

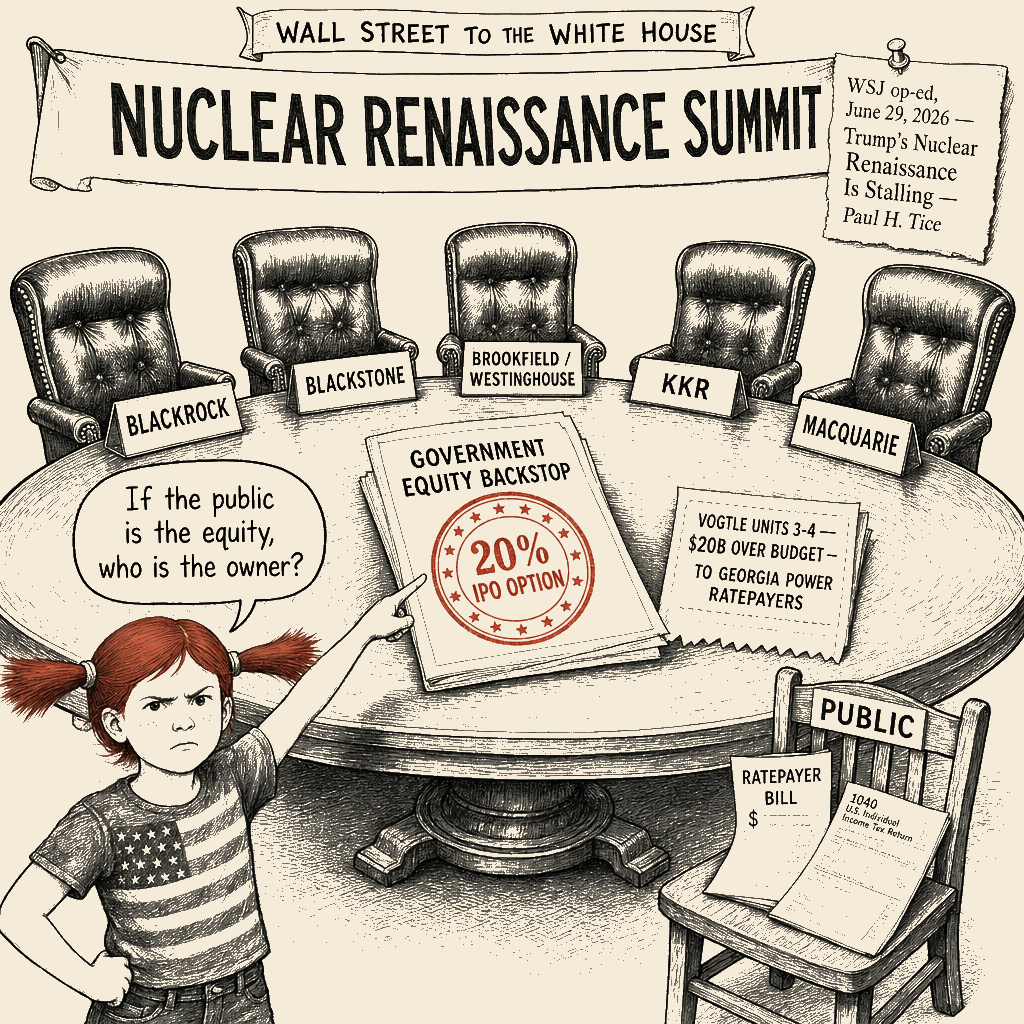

A trade that deserves scrutiny: the October 2025 Westinghouse-Commerce Department partnership is the deal the piece wants you to read as the foundation of America’s nuclear future. Read the small print. In exchange for government financial support and expedited regulatory approval, the U.S. government receives a “participation interest” in Westinghouse cash distributions and an option on 20% of any future IPO. The federal government is being asked to take an equity stake in a private contractor to backstop a multi-billion-dollar capital project whose cost overruns would be paid by ratepayers.

Westinghouse is owned by Brookfield Asset Management, the Canadian alternative-asset giant, since emerging from bankruptcy in 2018. The same Brookfield that has been buying U.S. energy assets across the cycle. The same private-equity architecture the piece wants summoning to the White House.

The piece’s author is a senior fellow at the National Center for Energy Analytics, launched in the 2023–2024 window, and the author of NCEA’s “A Strategy for Financing the Nuclear Future” report — the policy paper the op-ed paraphrases. The author of the article is the author of the policy blueprint. That is worth knowing before treating the framing as neutral analysis.

The cui bono has a clean answer. Westinghouse (Brookfield-owned) gains a government equity backstop and a captive customer pipeline. The PE infrastructure funds gain a structured, government-blessed entry into multi-decade regulated utility capital projects on favorable terms. The cost-bearers are ratepayers, who would absorb any cost overruns through rate increases, and taxpayers, who are putting public capital at risk for private gain. The piece’s prescription would make the public the equity layer of a private-sector bet, with the public taking the downside and the private sector taking the upside.

The same 400-gigawatt ambition can be served by a different design: government procurement at the federal level, ratepayer cost caps, technology-neutral licensing reform, and a regulatory environment that lets the best technology win on cost and timeline rather than on which firm bought which senator’s lunch.

A civic good distributed to the many looks different from a private gain concentrated in the few, even when both are wrapped in the same word “nuclear.”

DEFCON 3 — Mockery and Ridicule

When to use: A Twitter-thread exchange with someone repeating the PE-solves-nuclear line; perform for the bystander watching the back-and-forth.

Brace yourselves. Paul Tice has solved American energy policy. The answer was always BlackRock.

Picture it. BlackRock — the world’s largest asset manager, central architect of the five-year utility-buying spree that has consolidated U.S. electric utilities into fewer and fewer hands — is the missing piece. BlackRock is going to save nuclear power. The firm whose entire investment thesis on utility acquisitions has been “stable regulated returns and modest capex” is going to break ground on a $25 billion nuclear plant that will take a decade to complete. The same BlackRock whose Climate-Related Disclosures preach long-term stewardship is going to write a check for a multi-decade capital project on a multi-decade timeline. Sure.

You can’t make this up. The same op-ed that scolds the administration for chasing “shiny objects” in fusion and SMRs wants you to believe that a $10 trillion asset manager is the un-shiny object. The same op-ed that worries about the U.S. “losing its lead” in nuclear wants to hand the lead to a Canadian alternative-asset firm that owns Westinghouse. The same op-ed that complains about government distraction wants you to read the Westinghouse-government partnership — where the U.S. takes an equity stake in a private contractor to backstop the contractor’s risk — as the model for a clean nuclear future.

The piece is a paid policy paper wearing an op-ed costume. The author is the author of NCEA’s “A Strategy for Financing the Nuclear Future.” The strategy is: have the government take private contractor risk, hand the contractor a captive customer base of utilities (whose own executives are now too scared to commit, for the perfectly sound reason that the math doesn’t work), and call it a renaissance. Larry Fink is reportedly unavailable for comment, but his PR team is ready with talking points about how saving the climate and serving shareholders are totally compatible if the government puts up the equity.

The next time someone tells you the free market will solve the climate crisis, ask them to define “free” and “market” and “solve” all in the same sentence.

DEFCON 2 — Aggressive Villainization

When to use: A forum or Substack reply where a PE-apologist is active; heavy villainization of the IDEAS and INSTITUTIONS, not the persons.

The argument wants you to think: the bottleneck on American nuclear is “risk-averse utility customers” who need a Wall Street pep talk. The argument is engineered to make you think that.

The real bottleneck is the math. The last two AP1000s at Vogtle ran more than $20 billion over budget, and the bill went to Georgia Power ratepayers. The next build has no reason to be cheaper on the merits — first-of-a-kind engineering costs do not fall that fast. Private equity is not in the business of multi-decade, low-return, high-overrun-risk capital projects. It is in the business of leveraged buyouts, dividend recaps, and 18-month IRR targets. The op-ed asks you to believe PE will absorb what it is structurally designed to externalize.

The cui bono is clean. Westinghouse (Brookfield-owned since emerging from bankruptcy in 2018) gets a government equity backstop and a captive utility customer base. The PE infrastructure funds (BlackRock, Blackstone, KKR, Brookfield, Macquarie) get a structured, government-cleared entry into regulated utility capital projects they would not otherwise be able to take on at the right risk-return ratio. The 20% IPO option is a literal call option on the public’s money: the upside accrues to private owners, the downside accrues to taxpayers and ratepayers. The cost-bearers include ratepayers in any state that signs up, communities that bear the siting of large reactors, and competing nuclear technologies (SMRs, advanced reactors) whose firms (NuScale, TerraPower, X-energy) have documented commercial deployment pathways and are dismissed in the op-ed as “shiny objects.”

The hypocrisy exposure is on the table. The piece invokes free-market values on the demand side and government equity on the supply side. The piece complains about the administration’s “distraction” by a U.K. trade deal while endorsing a Commerce Department-Westinghouse deal in which the U.S. government takes an equity stake in a foreign-controlled private contractor. The piece complains about the Westinghouse partnership’s lack of traction in the eight months since it was signed, then proposes summoning PE to make the same partnership work. The contradictions are not bugs in the argument; they are the design.

A serious question for the piece’s author: NCEA’s funding is not publicly broken out by donor. Before treating this analysis as neutral, the public deserves to know which firms in the PE-and-nuclear space may have underwritten the think tank that produced the report the op-ed paraphrases.

A serious question for the PE infrastructure funds named in the piece: the same firms that engineered the utility-consolidation problem are now being summoned to lead the nuclear solution. The piece never asks whether the consolidation itself is part of why utilities are constrained. The piece is structurally unable to ask that question, because the answer would indict the firms the piece is asking to be summoned.

DEFCON 1 — Nuclear Satire

When to use: Catharsis. When the goal is to expose the bad-faith reader in grotesque metaphor; perform for the ally who needs the air cleared.

You have to admire the elegance of the con. The same firms that bought the grid over the last decade now want you to believe they will save the grid from itself.

The op-ed proposes, with a straight face, summoning the private-equity owners of America’s electric utilities to the White House to lead the next nuclear build. The same PE funds that engineered the consolidation. The same PE funds that, when they buy a regulated utility, promptly slash capex, raise dividends, lever up the balance sheet, and ship the cash back to the limited partners. The same PE funds whose entire investment thesis on utilities is “stable regulated returns, modest capex, predictable cash distributions.” Now you’re supposed to believe that a $10 trillion asset manager, whose portfolio construction treats every regulated utility as a yield instrument, is going to break ground on a $25 billion multi-decade capital project that has, on the last attempt, bankrupted its builder and run $20 billion over budget.

The math is not a mystery. The math is the answer. The piece does not want you to do the math.

The piece complains about “shiny object syndrome” while summoning the shiniest objects in the global financial system. It complains about government “distraction” while endorsing a deal in which the U.S. government takes an equity stake in a Canadian-owned private contractor to backstop private risk. It complains about the Westinghouse deal’s lack of traction eight months in, then proposes summoning PE to make the Westinghouse deal work. The contradictions are so consistent they are unmistakable. The contradictions are the design.

The piece is a paid policy paper, written by the author of the NCEA report, published in the editorial pages of a major newspaper, in the hope that the public reads it as neutral analysis. The author is a senior fellow at a pro-nuclear think tank that functions as an advocate for the industry it analyzes. The industry’s preferred policy is: have the government take the contractor risk, hand the contractor a captive customer base, and call it a renaissance.

A modest policy suggestion, in case anyone at the captured agencies is reading: if you want the public to underwrite a multi-decade capital project, give the public the upside. Nationalize the build. Standardize the designs. Run the program like the Manhattan Project or Apollo: government-funded, government-procured, private-sector-built, with the public owning the assets. The same 400-gigawatt ambition. The same nuclear power. None of the equity in private hands.

But that is not what the op-ed is asking for. The op-ed is asking for a different kind of renaissance: the one where BlackRock, Blackstone, and Brookfield own the nuclear future they are summoning the public to subsidize.

DEFCON 1+ — Prophetic Indictment

When to use: For the reader moved by moral authority with an edge; long-form Substack or column-length response; the prophetic-moral register with restrained profanity, calibrated below the 1++ apex.

The prophet Jeremiah had a name for the public figure who has lost the capacity to blush. The op-ed on America’s “stalling nuclear renaissance” has the diagnostic on its own sleeve. It is written by the author of the policy paper the op-ed paraphrases. It is published as opinion by a newspaper whose editorial board has, in other contexts, defended the free market. It complains about government “distraction” while endorsing government equity in a foreign-owned private contractor. It complains about “shiny object syndrome” while summoning the shiniest objects in global finance to lead the buildout. The op-ed does not blush. The op-ed does not know damn well how to.

Cicero, on the orator who curries favor with money: adulatio — flattery in the form of analysis. The op-ed’s posture is that of a neutral energy wonk presenting the obvious solution. The obvious solution is: have the government take the private contractor’s risk, hand the contractor a captive utility customer base, and pay the contractor’s IPO upside in public money. The posture of neutrality is the work. The adulatio is the actual content. It is horseshit dressed in a three-piece suit, and the suit costs the public a lot of damn money.

Hubris is, in the Greek tragedians, ruinous arrogance that mistakes the speaker for the structure. The op-ed is the structural-political equivalent: a small constellation of PE firms and one Canadian-controlled nuclear contractor have been mistaken, in the prose, for the public interest. The hubris is so practiced it almost reads as analysis. The op-ed wants to write the national energy policy of the United States in the interest of a $10 trillion asset manager and a Brookfield-owned nuclear vendor. The op-ed does not seem to find this strange. The op-ed’s author is a senior fellow at a think tank that functions as an advocate for the industry it analyzes. The op-ed is, in the precise sense, captured.

Luxuria, in Tacitus: indulgence as governing principle. The proposed design is a banquet. The contractor eats the upside. The PE funds eat the structured return. The ratepayers eat the cost overruns. The taxpayers eat the contractor’s downside. The public interest, in the design, is what gets chewed.

Authority is brittle. Oppression is the mask of fear. Karis Nemik’s manifesto, written in another fictional galaxy, names the operational fact. The op-ed’s argument is brittle. It depends on ratepayers continuing to absorb cost overruns. It depends on taxpayers continuing to backstop private contractor risk. It depends on utilities continuing to be the captive customers of a contracting architecture they did not design. It depends on the public continuing to mistake a paid policy paper for neutral analysis. Every dependency is a fracture line.

Power doesn’t panic. Cassian Andor, in the same galaxy: the regime that escalates is the regime that knows it is exposed. The nuclear industry’s quiet panic is visible in the architecture of the proposed deal. The “summon Wall Street to the White House” pitch is the move of an industry that has tried the standard private-capital pitch and found no buyers. So it is asking the government to be the buyer of last resort, with the public’s money and the public’s risk. That is what the hell this is.

The op-ed wants to dress a private subsidy as a national revival. The national revival is real. The subsidy is real. The mistake is in mistaking one for the other.

A serious America would do this: nationalize the next round of nuclear builds. Standardize the designs. Cap ratepayer exposure. Government-funded, government-procured, private-sector-built, public-owned assets. The same 400-gigawatt ambition. The same nuclear power. None of the equity in private hands.

By any means necessary that operate inside the law, the analytic instrument, and the public register, we name what has been done and we keep the receipts. We are not coming together with anyone whose program requires the ongoing privatization of public risk.

DEFCON 1++ — Profane Scorched-Earth

When to use: Catharsis. The personal release valve. The all-out maximal-expletive climax.

OK. We’ve danced around this long enough. Let’s say what’s fucking true.

Paul Tice wrote a fucking policy paper for a fucking pro-nuclear think tank, and the Wall Street Journal fucking published it as an op-ed, and now we’re supposed to treat the fucking thing as analysis. The author is the author of the fucking NCEA report. The NCEA is a fucking pro-nuclear think tank launched in the 2023–2024 window, whose structural alignment and likely funding tie it to the industry it supposedly analyzes. The author is not a neutral energy wonk. The author is a fucking industry advocate wearing the costume of one.

The op-ed says the problem is “risk-averse utility customers.” The op-ed mentions the last two AP1000s at Vogtle came in “way over budget” and bankrupted Westinghouse, but it does not give the fucking $20 billion figure. It does not name the fucking Georgia Power ratepayers who ate the overrun. It does not say the reason utilities won’t commit is that they got burned, they know they’ll be burned again, and the ratepayers will be the motherfuckers who eat the next overrun. “Risk-averse” is the polite way of saying “we got burned, the math doesn’t work, and the people who’d be underwriting the risk are the same people who’d absorb the loss.”

The op-ed says summon BlackRock. Summon Blackstone. Summon the fucking PE infrastructure funds. The same PE funds whose five-year utility-buying spree consolidated the fucking grid into fewer and fewer hands. The same PE funds whose investment thesis on utilities is “stable regulated returns, modest capex, predictable cash distributions.” The same PE funds that, when they buy a regulated utility, promptly fucking slash capex, raise dividends, and ship the cash to the limited partners. Now they’re going to break ground on a $25 billion nuclear plant. Sure they are. And I have a fucking bridge in Brooklyn to sell you.

The op-ed complains about “shiny object syndrome” in fusion and SMRs. The op-ed wants to summon the shiniest fucking objects in the global financial system to lead the build. The op-ed’s argument is so fucking stupid it can be stated in one sentence: the way to build nuclear power is to have the most leveraged, most short-term-horizon, most quarterly-return-driven segment of global capital take a multi-decade low-return high-overrun-risk capital project. The op-ed does not find this fucking strange. The op-ed is written by a fucking senior fellow. The fucking think tank functions as an advocate for the fucking industry. The fucking report the op-ed paraphrases is the fucking policy blueprint. The fucking author is the fucking author of the fucking report. The fucking op-ed is the fucking policy paper in a fucking costume.

The October 2025 Westinghouse-Commerce Department deal: the U.S. government takes a fucking equity stake in a Brookfield-owned private contractor to backstop the contractor’s risk, in exchange for a participation interest in cash distributions and a 20% option on any future fucking IPO. The upside goes to private owners. The downside goes to fucking taxpayers. The ratepayers eat the cost overruns. The communities eat the fucking siting. The competing technologies (NuScale, TerraPower, X-energy) get dismissed as “shiny objects” because they’re not Brookfield-owned. The bullshit is so transparent you can see through it like a fucking window.

The answer is simple, it’s been the same answer for a decade, and the op-ed will not fucking say it: nationalize the fucking build. Standardize the designs. Cap the ratepayer exposure. Government-funded, government-procured, private-sector-built, public-owned assets. The same 400-gigawatt ambition. The same fucking nuclear power. None of the fucking equity in private hands.

The op-ed wants to dress a private subsidy as a national revival. The fuck it is. The fuck it has ever been. A private subsidy is a private subsidy. A national revival is a public build. The op-ed is asking the public to pay for the private contractor’s fucking risk, and the op-ed has the fucking gall to call it analysis. The fuck it is.

By any means necessary that operate inside the law, we name what has been done. We keep the fucking receipts. We are not fucking coming together with anyone whose program requires the ongoing fucking privatization of public risk.

The Deeper Breakdown

The op-ed’s apex beneficiaries are Westinghouse — owned by Brookfield Asset Management since emerging from bankruptcy in 2018 — and the PE infrastructure funds named or implied (BlackRock, Blackstone, plus peers like KKR, Macquarie, and Brookfield’s other vehicles). The mechanism is a three-part architecture: (1) government equity participation in Westinghouse, structured as a participation interest in cash distributions and a 20% option on any future IPO, in exchange for financial support and expedited regulatory approval; (2) a “summit” of PE-owned utilities at the White House, organized to commit to AP1000 builds that PE-owned utilities would not commit to without government cover; (3) a captive utility customer base in which ratepayers absorb cost overruns through rate increases. The omitted fact is that the last two AP1000 builds at Vogtle ran more than $20 billion over budget, bankrupted the original Westinghouse, and put the overruns on Georgia Power ratepayers — the same pattern would be replicated under the proposed design, with the cost landing in the same place.

The receipts that prove the cui bono finding:

- Department of Energy Annual Energy Outlook, issued April 2026 — projects essentially no growth in U.S. nuclear generation capacity through 2050 under both baseline and high-demand scenarios. The op-ed’s premise of “stalling renaissance” is the DOE’s own conclusion.

- October 2025 Commerce Department-Westinghouse partnership — 10 AP1000 units, $80 billion in stated value; government equity participation in Westinghouse cash distributions; 20% IPO option under specified conditions; construction not scheduled to begin until 2030.

- Westinghouse’s 2017 Chapter 11 bankruptcy; Brookfield Asset Management and Cameco’s 2018 acquisition of Westinghouse in the 2018 reorganization.

- Vogtle Units 3 and 4: original budget approximately $14 billion; final cost approximately $35 billion; construction began 2013, Unit 3 came online in 2023, Unit 4 in 2024; cost overruns absorbed by Georgia Power ratepayers.

- The National Center for Energy Analytics (NCEA), launched in the 2023–2024 window, authored the report “A Strategy for Financing the Nuclear Future” cited in the op-ed; the op-ed’s author is the report’s author.

- PE utility consolidation in the 2020-2025 window: BlackRock, Blackstone, KKR, Brookfield, Macquarie, and other PE infrastructure funds have been the major buyers of U.S. electric utility assets, with trend-level consolidation effects on capex and balance-sheet leverage noted in industry analysis. The Yale Thurman Arnold Project’s 2026 paper raises specific competition concerns about PE utility acquisitions.

The piece’s underlying diagnosis is sound. The DOE’s own April 2026 Annual Energy Outlook confirms the “stalling” premise. The technology-trap critique of faddish SMR and fusion enthusiasm has real teeth. The Vogtle cost-overrun facts are documented in the project’s own public reporting. The proposed solution is where the analysis inverts: a concentrated beneficiary is asked to be amplified, the costs are externalized to ratepayers, taxpayers, and competing technologies, and the public is asked to take the equity-layer risk in a private-sector bet while the private sector takes the upside. The remedy is government procurement at the federal level, ratepayer cost caps, technology-neutral licensing reform, and standardized designs (including the advanced reactors already at advanced licensing stages) — the same civic good, with the public interest in the design.

Missing information: NCEA’s donor list is not publicly broken out at the level required to confirm which PE or nuclear-industry firms have underwritten the think tank that produced the report the op-ed paraphrases.

About Malcolm Little King

Malcolm Little King is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Malcolm Little King's lane covers, rendered through Malcolm Little King's register.