Responding to: The Dutch Lawsuit That Could Undermine U.S. Energy Security — Michael Toth · 2026-07-06

What the Piece Argues

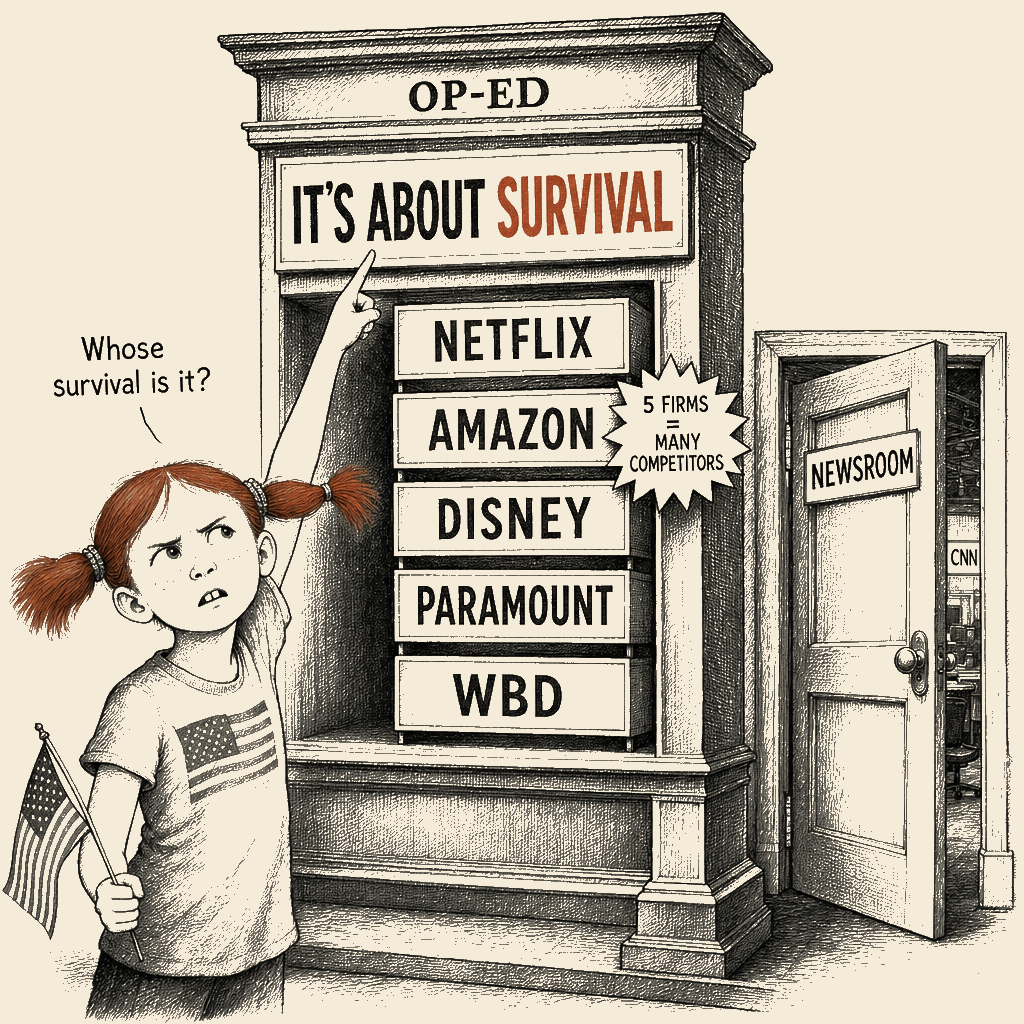

Michael Toth’s op-ed defends the proposed $111 billion Paramount–Warner Bros. Discovery merger against an anticipated legal challenge from a coalition of state attorneys general led by California’s Rob Bonta. Toth argues the merger is not a grab for monopoly power but a defensive necessity for Paramount and WBD to compete with the much larger Netflix, Amazon, and Disney in a capital-intensive streaming market. He claims the deal’s combined 22 percent streaming-subscriber share falls well below the 30 percent presumption of anticompetitive harm established by United States v. Philadelphia National Bank (1963), and contends that blocking the merger will not prevent the streaming price increases and studio-movie declines already underway. The piece portrays the AGs’ anticipated challenge as a politically motivated “stunt” that, by leaving the merged entity unable to compete, would ultimately cost consumers more than the merger itself.

Receipts

The framing wants the reader to believe the Paramount–WBD merger is “about survival” — defensive consolidation needed to compete with Netflix, Amazon, and Disney — and that the Democratic state AGs preparing to challenge it are staging a politically motivated stunt that will leave consumers worse off.

-

The framing wants you to believe:

- The merger is the only way for Paramount and WBD to “survive” against Netflix, Amazon, and Disney.

- The combined 22 percent streaming-subscriber share is well below the antitrust concern threshold.

- AG Bonta’s challenge is a political stunt, not a substantive consumer-protection action.

- Blocking the merger will not stop price increases or save studio jobs.

- A “saturated market” of five major streamers proves the deal is competitive.

-

What’s really going on:

- “Survival” accrues to the merged entity’s controlling executive — David Ellison, Paramount’s CEO — who takes the controlling role at a $111 billion media portfolio combining HBO, CNN, Warner Bros. studios, and Paramount’s film and television catalog. The cui bono flows up to the new controlling executive, not down to the consumer paying the streaming bill.

- The “saturated market” of five firms controlling essentially all premium U.S. video streaming is the textbook oligopoly antitrust law exists to police — not a defense of further consolidation.

- The Philadelphia National Bank 30 percent threshold is the floor for presumption of anticompetitive harm in the relevant market, not the ceiling for scrutiny. Media-merger analysis examines content production, distribution channels, and news — a deal combining HBO, CNN, and a major film studio is a relevant-market question far broader than streaming subscribers.

- Netflix and Disney, two of the five firms Toth describes as a saturated market, raised prices 38 percent and 172 percent last year, per Toth’s own citation — evidence of the oligopoly pricing power further consolidation entrenches, not evidence the merger is harmless.

- The state AGs Toth dismisses won the last media merger they challenged: the Nexstar–Tegna deal Toth himself mentions was preliminarily blocked by a Sacramento federal judge.

Anchor citation: United States v. Philadelphia National Bank, 374 U.S. 321 (1963).

The DEFCON Ladder

DEFCON 5 — Polite Reframe

When to use: persuadable moderates, good-faith family at the holiday table, op-ed readers who want a measured rebuttal they can forward without flinching.

The argument that the Paramount–WBD merger is “about survival” is a real argument, and the 22 percent streaming-subscriber figure Toth cites is technically accurate. But “survival” is doing a lot of work in that sentence. Survival for whom? Paramount’s existing shareholders — and David Ellison, who becomes the controlling executive of the combined entity — gain operational control of one of the largest media portfolios in the world: HBO, CNN, Paramount’s film library, and Warner Bros. Discovery’s studios. That is not a survival story for the household paying the streaming bill each month. Antitrust law exists precisely to weigh whether “survival” of one company is worth the long-term loss of competition in a market that already sits four or five firms deep, and the Philadelphia National Bank 30 percent threshold is the floor for that inquiry, not the ceiling. The five-firm oligopoly Toth describes as a “saturated market” is the structural problem antitrust enforcement was built to address — not a justification for letting it consolidate further. Consumers, workers, news consumers, and smaller competitors are the constituency the law was written to defend; the controlling executive’s balance sheet is the constituency the law was written to weigh against them.

DEFCON 4 — Firm Moral Superiority

When to use: identity-protective mixed-faith readers, op-ed and Substack audiences who want analytical rigor with restraint and a named institutional trace.

Michael Toth asks the reader to trust that the Paramount–WBD merger is “about survival” — that without it, Paramount and WBD cannot compete with Netflix, Amazon, and Disney. The question that actually matters is not whether the merged company can survive. The question is who benefits from the merger’s consummation, and who bears the cost.

The benefit side: David Ellison, already Paramount’s CEO, becomes the controlling executive of a $111 billion media empire combining HBO, CNN, Warner Bros. studios, and Paramount’s film and television catalog. The opposition coalition Toth names in his own piece — Senator Cory Booker’s hearing, Mark Ruffalo’s testimony, Jane Fonda’s letter with 3,000 entertainment-industry signatories — is the documented record of concern Toth is asking the reader to set aside. The merger is “about survival” in the same sense that every leveraged buyout is “about creating value”: the value flows to the new controlling executive, and the costs are distributed.

The cost side: the five-firm streaming market Toth calls “saturated” is the textbook oligopoly antitrust law was written to police. Netflix and Disney — two of the five firms, per Toth’s own citation — raised prices 38 percent and 172 percent last year. Toth wants the reader to read those price hikes as evidence that consolidation is harmless. They are evidence of the opposite: the pricing power the oligopoly already wields, and the merger entrenches.

The state attorneys general Toth dismisses are doing the job state antitrust law assigns them, and they did it successfully in the Nexstar–Tegna case Toth himself mentions. If Toth’s argument were as strong as he presents, he would not need to characterize consumer-protection enforcement as a stunt.

DEFCON 3 — Mockery and Ridicule

When to use: bystanders who need the absurdity made visible, mixed audiences where the literalized image lands harder than the structural argument.

Michael Toth wants the reader to believe that a merger combining HBO, CNN, and a major film studio under one executive is “about survival.” Survival, presumably, the way a $111 billion media empire consolidating control over what Americans watch, read, and stream is the underdog fight. Paramount under David Ellison is the scrappy challenger here, just trying to make it in a tough neighborhood of Netflix, Disney, and Amazon — the three companies that collectively spent $63 billion on content last year, while Paramount and WBD scrape by on whatever is left of the couch cushions.

The five-firm streaming market Toth calls “saturated” is the joke. Five. Firms. That is the saturated market, the way a 7-Eleven on every corner is a saturated grocery economy. The five companies that will control essentially every show and movie most Americans pay to stream are the “many competitors” Toth wants the reader to see. Two of those five firms — Netflix and Disney, per Toth’s own admission — raised prices 38 percent and 172 percent last year, and he asks the reader to read those price hikes as proof that more consolidation is the answer. Toth is prescribing the tumor as the cure for the tumor, and asking the patient to thank him for the bill.

The piece closes by warning that consumers will pay a “merger tax” if the AGs win. But the merger tax is what happens when one company controls HBO, CNN, and the Paramount catalog. The merger tax is what Toth’s piece is asking the reader to bless. “It’s about survival” is the line every monopoly uses right before it kills the smaller competitor. Toth has written the merger’s press release and called it an op-ed.

DEFCON 2 — Aggressive Villainization

When to use: mixed-to-bad-faith actors, when the case needs to be drawn hard and the named figures named in their named role.

The Paramount–WBD merger is not “about survival.” It is about David Ellison — already Paramount’s CEO — becoming the controlling executive of a $111 billion media empire that includes HBO, CNN, and Warner Bros. Discovery’s film and television operations. Toth wants the reader to read the deal as the underdog fight of a struggling streamer against giants. The opposition coalition Toth himself names — Senator Booker’s hearing, Mark Ruffalo’s testimony, Jane Fonda’s letter with 3,000 entertainment-industry signatories — is the documented record of structural concern Toth asks the reader to forget. That is the structural fact Toth is asking the reader to overlook.

The “five-firm saturated market” Toth invokes is the textbook oligopoly. Five firms control essentially all premium video streaming in the United States. Toth wants the reader to call that “many competitors” because naming the structure accurately — concentrated, oligopolistic, antitrust-relevant, in need of enforcement — would not let him make his argument. Two of those five firms — Netflix and Disney, per Toth’s own citation — raised prices 38 percent and 172 percent last year, and he wants the reader to read those price hikes as evidence that consolidation is harmless. They are the proof that the oligopoly already has pricing power, and the merger entrenches it.

The state attorneys general Toth dismisses as staging a “political stunt” are doing the job state antitrust law assigns them, and they won the last time they did it — the Nexstar–Tegna merger Toth himself mentions was preliminarily blocked by a Sacramento federal judge. If Toth’s case were as strong as he presents, he would not need to characterize consumer protection as a stunt.

The piece’s closing line inverts the term. “Merger tax,” Toth writes, is what consumers pay when “political stunts trump the rule of law.” The merger tax is what the merger imposes. The merger tax is what the deal will cost consumers in higher prices, fewer choices, and less newsroom independence once CNN sits under David Ellison’s roof. Toth knows what the merger tax is. He has built the piece to rename it.

DEFCON 1 — Nuclear Satire

When to use: bad-faith actors, performative trolls, and the catharsis for allies; receipts still required at every paragraph.

Michael Toth has written a 1,200-word press release for a $111 billion media merger and called it an op-ed. The merger combines HBO, CNN, and Warner Bros. Discovery’s film and television operations under the control of David Ellison, already Paramount’s CEO — a controlling executive whose transition to the top of a $111 billion media portfolio is the structural fact Toth asks the reader to set aside. Toth wants the reader to call this a “survival story,” the way a patient who came in for a hangnail and left with a limb amputation is the story of “aggressive intervention.”

The five-firm streaming market Toth calls “saturated” is five. Companies. He wants the reader to look at the landscape in which five firms control essentially all premium video streaming in the United States and call it “many competitors” the way a desert with five oases is “lush.” Two of those five firms — Netflix and Disney, per Toth’s own admission — raised prices 38 percent and 172 percent last year, and he wants the reader to read those price hikes as proof that more consolidation is the cure. This is the medical equivalent of prescribing the disease for the disease and calling it breakthrough medicine.

The “22 percent market share well under the Philadelphia National Bank threshold” line is the most lawyerly-sounding piece of bullshit in the piece. The threshold is the floor for presumption, not the ceiling for scrutiny, and the relevant market for a merger combining HBO, CNN, and a major film studio is not “percent of streaming subscribers.” The relevant market is content production, distribution, and news — and in any of those, the merged entity is a giant. Toth cites the threshold to wave the deal past scrutiny the way a creationist cites transitional gaps to wave evolution past a biology class. The move is the same. The intellectual honesty is the same.

The state AGs Toth dismisses are doing the job state antitrust law assigns them, and the last time they did it — the Nexstar–Tegna merger Toth himself mentions — they won. A Sacramento federal judge preliminarily blocked that deal. The pattern is: AGs challenge a merger, the merger hits a courtroom, the courtroom does what courts do. Toth wants the reader to read the courtroom part as a “political stunt” because the courtroom part is where the bill of sale for the rest of American media gets examined. Toth does not want that examination. The piece is the argument against the examination.

The closing line calls the “merger tax” the cost of the AGs’ lawsuit. The merger tax is what consumers pay when one company owns HBO and CNN and the Paramount film library and decides the streaming prices for all of it. The merger tax is what Toth’s piece is asking the reader to bless. Toth is not worried about the merger tax. Toth is worried about the antitrust lawyers.

DEFCON 1+ — Prophetic Indictment

When to use: the reader moved by moral authority with an edge; the canonical register deployed; restrained profanity where it sharpens the blade; calibrated below the 1++ apex.

What the prophet Amos said of the merchants of his day — that they sold the righteous for silver and the needy for a pair of sandals — the same indictment falls on the merchants of this merger: they would sell the news, the film, and the future of an informed citizenry for the third yacht, and they would name it survival.

Michael Toth writes in the National Review that the Paramount–WBD merger is “about survival.” The word is a deflection. The deal transfers operational control of HBO, CNN, and Warner Bros. Discovery’s catalog into the hands of a single executive — David Ellison, Paramount’s CEO — who takes the controlling role at the combined $111 billion entity. Critics including Senator Cory Booker, Mark Ruffalo, and 3,000 entertainment-industry signatories organized by Jane Fonda have publicly opposed the merger; Toth has called them theater. Toth asks the reader to read this transaction as a struggling company fighting for its life. It is not a struggling company. It is a controlling executive taking control.

The five firms Toth names as the saturated market — Netflix, Amazon, Disney, and the two about to be merged — are the structure the antitrust laws were written to police. That the structure is “saturated with major players” is not a defense of it; it is a description of it. Five is not many. Five is what concentrated power looks like when the regulators are not looking. Toth’s piece is a regulator-not-looking essay. Two of those five firms — Netflix and Disney, per Toth’s own citation — raised prices 38 percent and 172 percent last year. That is what the oligopoly does, and the merger is what entrenches the oligopoly.

And one word for the bullshit arithmetic of the “22 percent well under the Philadelphia National Bank threshold” line: the threshold is the floor for presumption, not the ceiling for scrutiny, and the relevant market for a deal that combines HBO, CNN, and a major film studio is not “percent of streaming subscribers.” It is the market for content production, distribution, and the news. In any of those, the combined entity is damn well a giant.

The piece closes by warning that the consumer will pay the “merger tax” if the AGs win. The merger tax is what the consumer pays now. The merger tax is what the consumer has been paying since the four-firm concentration of meatpacking, the three-firm concentration of wireless carriers, the three-firm concentration of airlines. The merger tax is the architecture of extraction dressed in the language of efficiency.

The state attorneys general Toth mocks are the inheritors of a long line of consumer-protection work in this country — Bonta’s office did the same work in the Nexstar–Tegna case Toth himself mentions, and the Sacramento federal judge preliminarily blocked that deal. Toth has called the lawsuit a “political stunt.” The lawsuit is what the lawsuit is — a state antitrust action under state antitrust law, brought by officers elected to do precisely this work, and dismissed by Toth as theater because the courtroom is where the architecture gets examined.

Jeremiah said of his generation: they have healed the wound of the people lightly, saying peace, peace, when there is no peace. Toth’s piece heals the wound of concentrated media power lightly, saying competition, competition, when the market has five firms. The piece is the wound. The piece is the light healing.

DEFCON 1++ — Profane Scorched-Earth

When to use: full catharsis, gloves all the way off, the reader who needs the maximal release; same absolute constraints as 1 (kick up at named power only, never the rank-and-file; no dehumanization; no calls to violence; no slurs against protected classes).

Michael Toth has written what amounts to a paid shill piece for a $111 billion media merger that consolidates HBO, CNN, and the Paramount film library under the control of David fucking Ellison — Paramount’s CEO — and he has the fucking nerve to call it “about survival.” The survival is the controlling executive’s. The survival is the next quarter’s earnings report. The survival is not yours, and it sure as shit is not the newsroom independence of CNN once it sits under the roof of an executive whose takeover of a $111 billion media empire is the most fucking obvious structural fact in the merger.

Toth wants the reader to look at five firms controlling essentially all premium video streaming in the United States and call that a “saturated market” the way a desert with five fucking oases is a tropical paradise. Five. Companies. He wants the reader to call them “many competitors” because naming the structure accurately — concentrated, oligopolistic, antitrust-relevant — would not let him make his argument. Two of those five firms — Netflix and Disney, per Toth’s own goddamned citation — raised prices 38 percent and 172 percent last year, and he wants the reader to read those price hikes as proof that more consolidation is the answer. The cure is the disease is the fucking cure.

The “22 percent market share well under the Philadelphia National Bank threshold” line is the most lawyerly-sounding bullshit in the piece. The threshold is the floor for presumption, not the ceiling for scrutiny, and the relevant market for a merger combining HBO, CNN, and a major film studio is not “percent of streaming subscribers.” The relevant market is content production, distribution, and news — and in any of those the merged entity is a fucking giant. Toth cites the threshold to wave the deal past scrutiny the way a creationist cites transitional gaps to wave evolution past a biology class. The move is the same. The intellectual honesty is the same.

The state AGs Toth dismisses as staging a “political stunt” are doing the goddamned job state antitrust law assigns them. They won the last time they did it — the Nexstar–Tegna merger Toth himself mentions was preliminarily blocked by a Sacramento federal judge. Toth is asking the reader to call the courtroom the stunt because the courtroom is where the bill of sale for American media gets examined. The piece is the argument against the examination. The piece is the press release for a fucking merger dressed up as a Toth op-ed.

And the fucking closing line. “Consumers will thank them. After all, they are the ones who end up paying the ‘merger tax’ in the form of higher prices, degraded service, and, ultimately, less competition when political stunts trump the rule of law.” Toth has just told the reader, in the most lawyerly way possible, that the merger tax is what the AGs cost. The merger tax is what the merger fucking costs. The merger tax is what the deal imposes: higher prices, fewer choices, less newsroom independence, one more firm that gets to decide what Americans watch and read. Toth knows what the merger tax is. He has written the merger tax a press release and called it an op-ed and run it in the National Review, and the fucking nerve of calling the regulators the stunt is the whole fucking piece.

About Malcolm Little King

Malcolm Little King is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Malcolm Little King's lane covers, rendered through Malcolm Little King's register.