Responding to: SEC Should Shut Down Big Brother Database for Stock Traders — Richard Morrison · 2026-06-29

What the Piece Argues

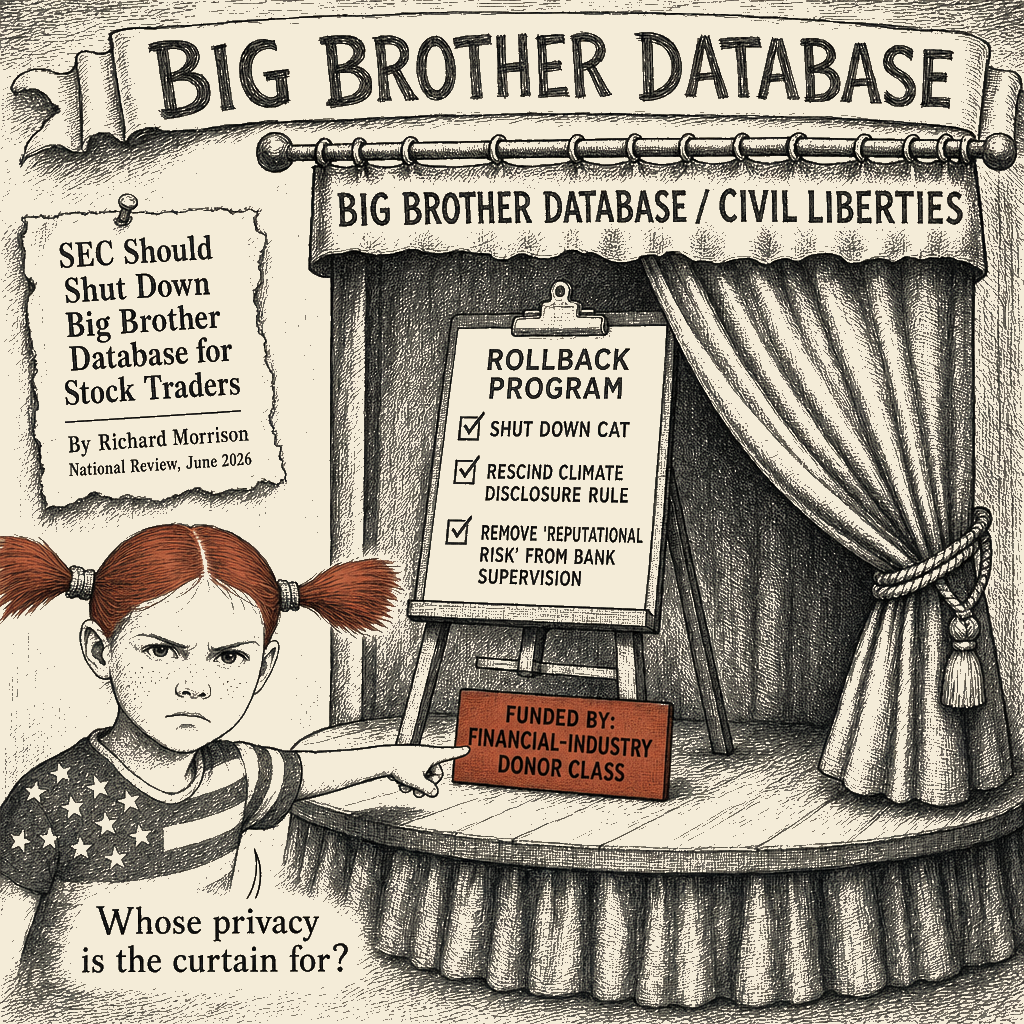

The piece, by Richard Morrison in National Review, argues that the Securities and Exchange Commission should “shut down entirely” its Consolidated Audit Trail — the master database tracking every order, cancellation, modification, and executed trade in U.S. equity and options markets. Morrison frames the CAT as an Orwellian surveillance tool with First Amendment (compelled disclosure of expressive conduct), Fourth Amendment (warrantless mass surveillance), and Fifth Amendment (regulatory taking of proprietary trading strategies; compelled self-incrimination) problems, and as a cybersecurity and privacy threat to ordinary Americans. The piece closes by linking the CAT to two other Trump-era SEC moves it endorses — rescinding the climate-disclosure rule and removing “reputational risk” from bank supervisory criteria — as part of a broader pattern of rolling back “deep-state overreach” in financial regulation.

Receipts

The piece is selling a civil-liberties argument for a regulatory rollback whose real beneficiaries are the financial industry’s most opaque trading operations.

-

The framing wants you to believe:

- The CAT is a “Big Brother” database that threatens ordinary Americans’ constitutional rights

- Tracking every trade is equivalent to the government tracking every grocery purchase

- The program is unconstitutional on First, Fourth, and Fifth Amendment grounds

- Closing the CAT protects civil liberties and complements a broader rollback of financial overreach

-

What’s really going on:

- The article itself names the suppressed variable in plain English: it worries specifically that CAT data “can reveal highly valuable proprietary trading strategies” — i.e., the loudest privacy claim in the piece belongs to the actors whose trades most need to be visible to the regulator

- The cui bono is the financial industry’s most opaque trading operations: high-frequency traders, hedge funds, and proprietary desks whose advantage depends on informational asymmetry the CAT would close

- The piece runs in National Review, a long-standing publication of the financial-industry donor class, and amplifies SEC Commissioner Hester Peirce (a consistent deregulatory voice), the Cato Institute (Koch funding), the Competitive Enterprise Institute, and the University of Chicago law-and-economics tradition — the institutional network behind the deregulatory program the piece is advancing

- The “rollback” the piece celebrates — climate-disclosure rescission, removal of “reputational risk” from bank supervision — is a deregulatory program, not a privacy program; the climate rule would have made public companies disclose climate risk to shareholders, and “reputational risk” let bank regulators flag banks doing business with fraudsters and money-launderers

- The SEC is a market regulator collecting data to detect the insider trading, spoofing, and front-running that cost ordinary investors billions annually — fraud that becomes nearly impossible to prosecute without a complete audit trail

The DEFCON Ladder

DEFCON 5 — Polite Reframe

When to use: A persuadable friend or good-faith relative who heard the “Big Brother” line and is worried. Calm, professional, fact-driven; the gentle correction that separates the constitutional question from the beneficiaries.

The piece asks us to imagine that tracking every stock trade is equivalent to the government tracking every grocery purchase. It is not. The SEC collects trade data to detect market manipulation, insider trading, and spoofing — crimes that cost ordinary investors billions of dollars a year, and that are nearly impossible to prosecute without a complete audit trail. The 2010 flash crash, which briefly erased roughly a trillion dollars in U.S. equity market value, was the proximate justification for the CAT in the first place. The SEC’s enforcement record on insider trading and spoofing has relied, for years, on exactly this kind of comprehensive data.

The piece’s own paragraph concedes the suppressed variable: it worries, specifically, that CAT data “can reveal highly valuable proprietary trading strategies.” That is not the worry of an ordinary investor. That is the worry of a high-frequency trader or a hedge-fund desk whose business model depends on keeping its strategy dark. The privacy claim in this piece is the privacy claim of the proprietary trader, not the privacy claim of the retiree whose 401(k) the proprietary trader is siphoning from.

A market where every trade is traceable is a market where the small investor is harder to rip off. That is what is being dismantled in the name of “limited government.”

DEFCON 4 — Firm Moral Superiority

When to use: A semi-skeptical reader who is already half-sold on the “civil liberties” framing and needs the cui bono to land. Op-ed/Substack length; iron spine; the moment to widen the receipts from the data point to the institutional authors.

Let’s trace the money.

The piece is published in National Review — a publication that has run an editorial line on financial regulation tracking the preferences of the donor class that funds it. The author flags the institutional allies by name: SEC Commissioner Hester Peirce (the SEC’s most consistent deregulatory voice, often alone on the commission across two Republican administrations), Wayne Crews at the Competitive Enterprise Institute (an industry-funded deregulatory outfit), the Cato Institute (Koch money), and the University of Chicago Business Law Review (fifty years of deregulatory legal scholarship). SEC Chairman Paul Atkins — confirmed by the Senate on April 9, 2025 and sworn in on April 21, 2025 — is the official under whose leadership the piece expects the CAT to be “ameliorated,” and he has a long deregulatory record, including a previous stint as an SEC commissioner in the George W. Bush era.

The “proprietary trading strategy” line is the tell. The piece worries that the SEC might see “highly valuable proprietary trading strategies” — i.e., the algorithmic patterns that high-frequency traders and proprietary desks use to front-run, spoof, and otherwise extract value from ordinary investors’ orders. The piece wants you to read that as a First Amendment problem. Read it instead as a description of the conduct the CAT is designed to detect.

The rest of the piece’s “rollback” program — the climate-disclosure rule (rescinded), “reputational risk” (dropped from bank supervision) — is the same story in two more venues. The climate rule would have made public companies disclose the climate risks they are pricing into their business plans, information shareholders are entitled to under existing securities law. “Reputational risk” was the supervisory tool that let bank regulators flag a bank doing business with a fraudster or a money-launderer. The piece celebrates the rollback of all three. None of the three is a privacy win for ordinary Americans. All three are wins for the actors who preferred their trades, their climate exposure, and their customer lists to remain dark.

The piece is a brief for opacity, dressed in civil-liberties clothing.

DEFCON 3 — Mockery and Ridicule

When to use: The audience is already inoculated against the “civil liberties” frame and is watching to see who is allowed to get away with what. Funny before devastating; the rack in the room.

So the pitch is: the biggest civil-liberties threat in American financial regulation is that the SEC can see what Goldman Sachs is doing. Goldman Sachs. The poor, oppressed proprietary traders at the multi-billion-dollar hedge fund whose sole asset is a model the SEC is now — unconstitutionally, apparently — able to read.

Imagine being a high-frequency trader paying eight figures a year for a mansion in Greenwich, and having your congressman explain to the SEC that the privacy violation in this country is them noticing that you are front-running the orders of a 71-year-old in Akron buying 200 shares of Procter & Gamble.

That’s the First Amendment problem. That’s the chilling effect on association. Not the journalists being doxxed, not the donors being mapped, not the state legislators being stalked by the people who lost the last election — those are the people whose expressive association is being burdened. The proprietary trader. Whose “core values” are being exposed by his own market activity. Whose “deepest thoughts” the SEC can now read. Hester Peirce, ladies and gentlemen: standing up for the First Amendment rights of Citadel.

And the cybersecurity argument? That is rich. The bank regulators dropped “reputational risk” — the supervisory tool that flagged when a bank was doing business with a money-launderer. The climate-disclosure rule, which would have made public companies tell their shareholders about the climate risk they are pricing into their own books, was rescinded. The CAT is the surveillance state. The proprietary traders, the climate-fossil-fuel-suppressing banks, the defrauded-account holders: those are the victims of the surveillance state.

Brenda in Detroit feeding her two kids on $400 a month in SNAP is the surveillance state. The 71-year-old in Akron whose retirement account Citadel is picking clean: the surveillance state. The fund that cannot see its own exposure to the next Madoff: the surveillance state. The proprietary traders’ ability to operate in the dark: civil liberties.

Step away from the kool-aid.

DEFCON 2 — Aggressive Villainization

When to use: The audience has heard the polite and firm versions and is ready for the institutional authors to be named in their own words. The mirror; the moment the high-frequency trader’s privacy claim reflects back what the proprietary trading actually does.

The piece calls the CAT a “Big Brother” database. Let’s talk about Big Brother. The hedge fund that pays for order flow from your broker and front-runs your order before it hits the exchange: that is Big Brother. The proprietary trading desk that pays a record settlement to the DOJ to resolve spoofing charges: that is Big Brother. The bank that got a deferred-prosecution agreement for processing billions in suspicious transactions: Big Brother. The fund that loaded up on mortgage-backed securities in 2007 while selling them to pension funds, then needed a bailout: Big Brother. The market-maker that turns off its quotes the instant retail investors need liquidity: Big Brother.

The CAT is the accountability layer. It is the audit trail that lets the SEC follow the money from the suspicious transaction to the human being who made the decision. It is the tool that produces the deferred-prosecution agreements and the spoofing settlements. It is the only thing standing between the proprietary trader and the pension fund. The piece wants you to look at the SEC and call it the surveillance state. Look at the proprietary trading desk. That is the surveillance state. It is watching your 401(k). It is running the algorithm on your order. It is the deep state, in the only sense the word has ever actually meant.

The piece’s recommended fix — shut down the CAT — is not a privacy reform. It is a deregulation. The donor class is funding a deregulatory campaign. The deregulatory campaign needs a moral vocabulary. Privacy is the moral vocabulary. The proprietary trader is the actual client. The ordinary American is the bill.

DEFCON 1 — Nuclear Satire

When to use: The audience is bad-faith or performative, and the work is catharsis and containment. The piece’s named authors and beneficiaries treated with absolute villainization; the receipts laid end to end; the hyperbolic comparisons deployed in service of structural truth.

The argument before us is that the Securities and Exchange Commission — the regulator created after 1929 to keep the financial system from ripping off ordinary Americans a second time — has become the real civil-liberties threat in America. Not the IRS that just leaked the President’s tax returns. Not the FBI that spied on Martin Luther King Jr. Not the NSA that has been hoovering up your phone records since 9/11. The SEC. Tracking. Trades.

And the heroes of this piece are the proprietary traders. The same people whose literal business model is detecting your order and trading ahead of it. The people who built the 2010 flash crash. The people who brought us the 2008 financial crisis, the Knight Capital glitch that cost the firm $440 million in 45 minutes, the Madoff fund, the Enron special-purpose entities, the Wells Fargo fake accounts, the SVB interest-rate bet that vaporized in 48 hours, the FTX balance sheet, the Archegos margin call, the Treasury market dysfunction of March 2020. These are the people whose “expressive association” is being burdened by the existence of an audit trail.

The same people who gave us Operation Choke Point, the same people whose “Choke Point 2.0” debanked the cryptocurrency companies, the same people whose “reputational risk” tools were — oh wait. The piece celebrates the removal of those reputational risk tools. The piece celebrates the debanking. The piece celebrates the rollback of the climate disclosure rule. The piece is for Operation Choke Point. It is for the proprietary trader in the dark. It is against the public seeing the proprietary trader’s book. It is for the bank not telling its regulator which fraudsters it banks with. It is against the public company telling its shareholders its climate exposure.

What the piece is for is opacity. What it is against is accountability. The CAT is not a surveillance tool. It is the accountability tool. The piece is against accountability. The piece is for the proprietary trader. The piece is against you.

This is not a privacy argument. This is a looting argument in a privacy costume.

DEFCON 1+ — Prophetic Indictment

When to use: The reader moved by moral authority with an edge. The canonical register; restrained profanity where it sharpens the blade. The piece’s authors, in the Hebrew-prophetic cadence, named not for what they are at the level of the soul, but for what they have built.

The piece is selling a privacy argument on behalf of the people whose privacy most needs piercing. The prophet Amos stood in the gate of Israel and named the merchants who had “sold the righteous for silver, and the needy for a pair of shoes.” The piece before us is the same gate, the same merchants, the same shoes. The righteous are the ordinary investors the CAT would protect. The needy are the 71-year-olds whose orders the proprietary desk is trading against. The silver is the same silver. The pair of shoes is the regulatory apparatus, which the merchants have now, by means of the rhetoric of this piece, succeeded in stripping from the feet of the regulator.

The First Amendment was forged in a furnace of Jim Crow. It was forged to protect the NAACP from compelled disclosure of its membership list. The piece would apply that protection — forged in the bones of Black civil rights — to the right of a proprietary trading desk to hide its orders from the regulator that polices the integrity of the market. To take the canon of the civil-rights movement and redeploy it as a privilege of capital. To stand on the shoulders of Thurgood Marshall and use them as a stepladder to obscure a Goldman Sachs trade.

This is what Jeremiah named: the unblushing face. The piece does not blush. It does not have to blush. It has the apparatus. It has the donor class. It has the deregulatory think-tank network. It has the friendly commissioner. It has the friendly chairman. It has the publication. It has the moral vocabulary. It has the language of the Founding. It is using all of it — all of it — to keep the proprietary trader in the dark and the ordinary investor in the dark about the proprietary trader. The prophet’s diagnostic was: they did not know how to blush. The diagnostic holds. The face is still unblushing.

The CAT is the SEC’s audit trail. Audit trail. The phrase is older than the piece. Audit trail. The first audit trail was the prophet’s. The prophet who called the merchants to account. The piece before us would take the prophet’s language and turn it into a lawyer’s brief for the merchants.

We have seen this before. The prophet has seen it before. The prophet named it. The prophet said: hands full of blood. The hands that wrote the piece are full of the blood of the ordinary investors the CAT would protect. The hands are not shaking. The face is not blushing. The language of the Founding is being deployed. And the language of the Founding is, like the language of the prophet, being deployed by the merchants.

This is not a coincidence. It is a campaign. The campaign is well-funded. The campaign has a vocabulary. The campaign is winning.

DEFCON 1++ — Profane Scorched-Earth

When to use: The cathartic release valve. The reader who needs the gloves all the way off; the crowd that came for the prophetic and stayed for the demolition. Maximal profanity; receipts spine intact; the loudest, hardest tier.

The piece is a piece of shit. Let us say so.

It is a piece of shit written by a piece-of-shit institution for the benefit of a piece-of-shit client. The piece is for National Review, which has been carrying water for the donor class since Buckley. The author is Richard Morrison. The donor class is the financial industry. The client is the proprietary trader — the Goldman desk, the Citadel algorithm, the hedge fund whose entire fucking business model is detecting your order and front-running it. The piece is asking the American public to believe that the most oppressed class in American finance in 2026 is the proprietary trader.

The proprietary trader. The person who, in 2008, sold the mortgage-backed security to your pension fund and then needed a bailout when it blew up. The person who paid a record settlement to resolve the spoofing charges. The person who got the deferred-prosecution agreement for processing billions in suspicious transactions. The person who turned off the quotes the instant you needed liquidity in March 2020. The person who spammed your broker’s order book with fake quotes to move the price and made a quarter-cent on the spread. That person. That person is the civil-liberties victim in this story. The SEC can see his fucking trades. He needs constitutional protection. He needs the First Amendment. He needs the Fourth Amendment. He needs the Fifth Amendment. He needs the Court of Appeals. He needs the Supreme Court. He needs the Founding Fathers. He needs every fucking thing in the American constitutional canon — forged in a furnace of slavery, refined in the blood of the civil-rights movement, paid for in the bodies of the working class that the New Deal was supposed to protect — he needs ALL OF IT, the whole fucking thing, every word, every amendment, every precedent — to keep the regulator from seeing the fucking book.

The piece would have you believe that the proprietary trader’s expressive association is being chilled. The proprietary trader’s expressive association. The 401(k) he is trading against. The retiree whose order he is front-running. The 71-year-old in Akron. The pension fund in Toledo. The teacher in Cleveland whose retirement he is siphoning into his Greenwich fucking mansion. Those are the people whose expressive association is not being chilled. Those are the people who are being fucking looted. The piece is the looter’s brief.

And the piece is the looter’s brief dressed up in the language of the fucking civil-rights movement. The piece invokes the NAACP — Thurgood Marshall’s victory in 1958 — to protect the right of a proprietary trading desk to keep its orders hidden from the regulator. The piece invokes Americans for Prosperity Foundation v. Bonta — the 2021 victory against California’s donor-disclosure rule — to protect the proprietary trader from the CAT. The piece uses the entire fucking canon of American civil liberties — every fucking word — as a fucking shield for the proprietary trader.

This is the deepest fucking obscenity of the piece. The piece is not making a privacy argument. The piece is making a deregulation argument. The piece is funded by the financial industry. The piece’s recommended fix — shut down the CAT — is a win for the financial industry. The piece’s broader program — rescind the climate-disclosure rule, drop reputational risk from bank supervision, debank the crypto companies, leave the defrauded-account holders uncompensated — is a deregulatory program. The program is well-funded. The program has a vocabulary. The vocabulary is privacy. The actual program is opacity. The actual program is: the proprietary trader in the dark, the ordinary investor in the dark about the proprietary trader, and the regulatory apparatus dismantled.

The CAT is not a surveillance tool. The CAT is the audit trail. The audit trail is the regulator’s only fucking tool for following the money from the suspicious transaction to the human being who made the decision. The piece is the brief for dismantling that tool. The piece is the brief for the proprietary trader. The piece is a fucking brief, written by a fucking institution, for a fucking client.

The piece is the brief, and the brief is bullshit, and the bullshit is funded, and the funded bullshit is winning, and the winning is looting you, and the looting is in the fucking dark, and the dark is what the brief is for.

About Malcolm Little King

Malcolm Little King is a heteronym in Main Street Independent's editorial architecture — an analytical voice, not autobiography of any actual person. The position this column expresses is the publication's position on the territory Malcolm Little King's lane covers, rendered through Malcolm Little King's register.